Dunstan Electric Inc. is a private company specializing in the sale of high-end home appliances and consumer

Question:

Tyler & Perry (T&P), Chartered Accountants, has audited Dunstan Electric for over 20 years. You are the audit senior on the engagement. It is now December 11, 2013, and Jack Dunstan, founder and chief executive officer (CEO), called you to say that one of the company€™s largest stores was completely destroyed in a fire on December 7. With less than a month until the year-end, this fire has happened at a bad time.

Dunstan Electric is insured for damage caused by fire. Inventory and capital assets that were destroyed in the fire are insured at their replacement cost, assuming that the replacement is of the same make and model as the asset destroyed or, if it is no longer available, the closest substitute. The insurance policy states that the insured will receive the fair value of the building that was destroyed whether or not it is rebuilt. There is no business interruption insurance policy.

The statement of claim is currently being prepared. Once the insurers receive the claim, it will be validated, approved, and then paid within 60 days of approval. The accounting staff started working on the claim but have not yet completed it.

Anne Cooper, the engagement partner, has just met with Mr. Dunstan to obtain more information about the incident and the losses sustained (Exhibit I). You also obtain the November 2013 financial statements to help you plan for this year€™s audit engagement (Exhibit II). Anne would like you to prepare a memo outlining the financial accounting considerations and any other issues resulting from the fire.

Required:

Prepare the memo to Anne Cooper.

Exhibit I

According to the records at head office, the values of the destroyed capital assets are as follows:

Preliminary estimates include the following:

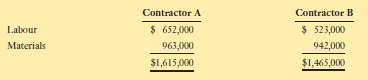

Building

Since the building was completely destroyed in the fire, a new one must now be built. As required by the insurance company, estimates from two contractors have already been received.

Jack Dunstan has never dealt with Contractor A, but the contractor has assured Jack that the building can be rebuilt similar to the newer, more modern Dunstan Electric stores. Contractor B was used for the construction of the last six Dunstan Electric stores. It is estimated to take six to eight months to rebuild the burnt store.

Jack and the insurers are currently negotiating which contractor to select. Jack has decided not to record any insurance proceeds until the negotiations are complete, and instead has booked a loss of $545,000 on the building for the year ended December 31, 2013.

Sales

No goods were sold or received after the fire. The salespeople estimated the week€™s worth of sales before the fire took place, since the weekly update to the main server was lost. Ninety percent of Dunstan€™s sales are on cash or credit card basis. For the cash and credit card sales, bank deposits are made on a daily basis by the stores. A printout of the web-based bank statement is made at head office to confirm the deposit information. The remaining 10% of sales are financed in-house. The financing application is approved at the time of the purchase by the store and the information is transferred to head office as part of the weekly update.

Inventory

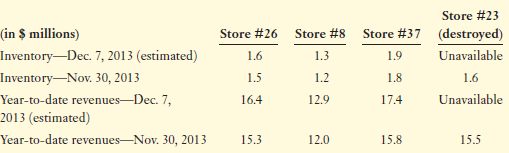

The destruction of the IT systems also created havoc in determining year-end inventory for the destroyed store. Since it is the holiday season, inventory levels of electronic goods are kept at higher levels than normal. To expedite the receipt of proceeds from the insurers, Jack went ahead and estimated the ending inventory by obtaining the inventory levels as at the date of the fire for the other three similar-sized Dunstan Electric stores:

Jack recorded insurance proceeds receivable of $1.9 million since he believes that Store #37 best approximates the destroyed store€™s activities. Jack noted, however, that some broken and older electronics items were being set aside at each of the stores in preparation for the year end inventory count. He has no idea of the value of these items in the burnt store and has not attempted to back out an amount from the other stores€™ figures.

Exhibit I

Other fire-related costs

The loss of the store has meant additional costs will be incurred:

Salaries still to be paid while employees are not able to work: ................ $110,000

Estimated site-demolition and clean-up cost: ............................................... $500,000

Municipal bylaws require a demolition of the building within 30 days. These costs will be expensed for accounting purposes.

Other

Dunstan Electric just refinanced its operating line of credit with its bank in November. As a result of this agreement, the bank now requires the audited financial statements for 2013 to be finalized no later than February 5, 2014.

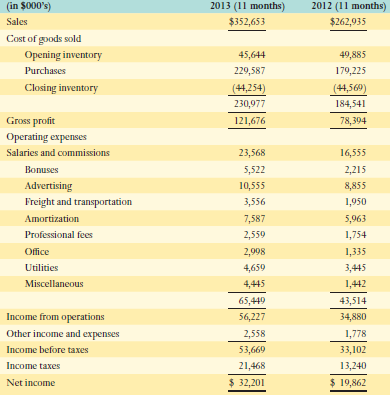

Jack and Judith were reviewing the draft financial statements and noticed the gross margin went up 6%. Jack believes that the increase is directly related to sales of electronic goods. Judith thinks otherwise. They don€™t have much management information on hand to help them analyze the reason for the increase.

Exhibit II

For the periods ended November 30

The ending inventory is the amount of inventory that a business is required to present on its balance sheet. It can be calculated using the ending inventory formula Ending Inventory Formula =... Financial Statements

Financial statements are the standardized formats to present the financial information related to a business or an organization for its users. Financial statements contain the historical information as well as current period’s financial... Line of Credit

A line of credit (LOC) is a preset borrowing limit that can be used at any time. The borrower can take money out as needed until the limit is reached, and as money is repaid, it can be borrowed again in the case of an open line of credit. A LOC is...

Step by Step Answer:

To Anne Cooper From CA Date December 12 2013 Subject Dunstan Electric Inc As requested I have considered the impact of the recent fire at Dunstan Electrics Store 23 The fire has a number of significan...View the full answer