On January 1, 2021, the general ledger of TNT Fireworks included the following account balances: During January

Question:

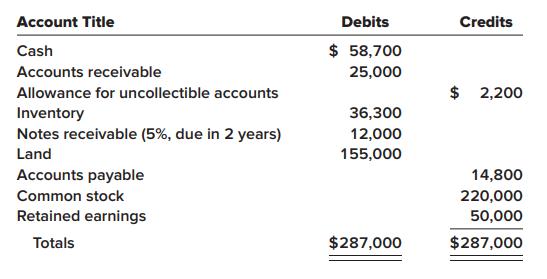

On January 1, 2021, the general ledger of TNT Fireworks included the following account balances:

During January 2021, the following transactions occurred:

Jan. 1 Purchased equipment for $19,500. The company estimates a residual value of $1,500 and a five-year service life.

4 Paid cash on accounts payable, $9,500.

8 Purchased additional inventory on account, $82,900.

15 Received cash on accounts receivable, $22,000.

19 Paid cash for salaries, $29,800.

28 Paid cash for January utilities, $16,500.

30 Firework sales for January totaled $220,000. All of these sales were on account. The cost of the units sold was $115,000.

Required:

1. Record each of the transactions listed above in the ‘General Journal’ tab (these are shown as items 1–8) assuming a perpetual FIFO inventory system. Review the ’General Ledger’ and the ’Trial Balance’ tabs to see the effect of the transactions on the account balances.

2. Record adjusting entries on January 31 in the ‘General Journal’ tab (these are shown as items 9–13):

a. Depreciation on the equipment for the month of January is calculated using the straight-line method.

b. At the end of January, $3,000 of accounts receivable are past due, and the company estimates that 50% of these accounts will not be collected. Of the remaining accounts receivable, the company estimates that 3% will not be collected. The note receivable of $12,000 is considered fully collectible and therefore is not included in the estimate of uncollectible accounts.

c. Accrued interest revenue on notes receivable for January.

d. Unpaid salaries at the end of January are $32,600.

e. Accrued income taxes at the end of January are $9,000.

3. Review the adjusted ‘Trial Balance’ as of January 31, 2021, in the ‘Trial Balance’ tab.

4. Prepare a multiple-step income statement for the period ended January 31, 2021, in the ‘Income Statement’ tab.

5. Prepare a classified balance sheet as of January 31, 2021, in the ‘Balance Sheet’ tab.

6. Record closing entries in the ‘General Journal’ tab.

7. Using the information from the requirements above, complete the ‘Analysis’ tab.

a. Calculate the return on assets ratio for the month of January. If the average return on assets for the industry in January is 2%, is the company more or less profitable than other companies in the same industry?

b. Calculate the profit margin for the month of January. If the industry average profit margin is 4%, is the company more or less efficient at converting sales to profit than other companies in the same industry?

c. Calculate the asset turnover ratio for the month of January. If the industry average asset turnover is 0.5 times per month, is the company more or less efficient at producing revenues with its assets than other companies in the same industry?

Balance SheetBalance sheet is a statement of the financial position of a business that list all the assets, liabilities, and owner’s equity and shareholder’s equity at a particular point of time. A balance sheet is also called as a “statement of financial...

Step by Step Answer:

Record each transaction in the general journal a Jan 1 Equipment purchased Debit Equipment 19500 Cre...View the full answer

Intermediate Accounting

ISBN: 978-1260481952

10th edition

Authors: J. David Spiceland, James Sepe, Mark Nelson, Wayne Thomas