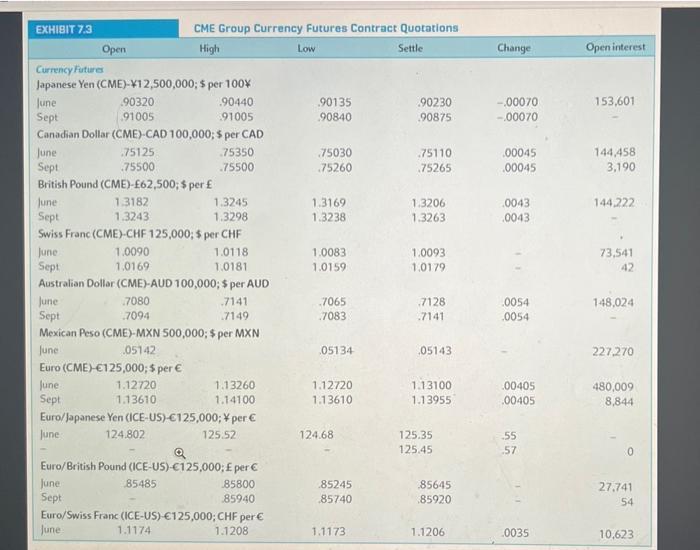

Using the quotations in Exhibit 7.3, note that the June 2019 Mexican peso futures contract has a

Question:

Using the quotations in Exhibit 7.3, note that the June 2019 Mexican peso futures contract has a price of $0.05143 per MXN. You believe the spot price in June will be $0.05795 per MXN. What speculative position would you enter into to attempt to profit from your beliefs? Calculate your anticipated profits, assuming you take a position in three contracts. What is the size of your profit (loss) if the futures price is indeed an unbiased predictor of the future spot price and this price materializes?

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

If you expect the Mexican peso to appreciate from 005143 to 0057...View the full answer

Answered By

Mugdha Sisodiya

My self Mugdha Sisodiya from Chhattisgarh India. I have completed my Bachelors degree in 2015 and My Master in Commerce degree in 2016. I am having expertise in Management, Cost and Finance Accounts. Further I have completed my Chartered Accountant and working as a Professional.

Since 2012 I am providing home tutions.

2+ Reviews

10+ Question Solved

Related Book For

Question Posted: