Question:

Assuming that Allied-Lyons was relying on a straddle strategy (refer to International Corporate Finance in Practice 7. 3 for background information), explain graphically and numerically under what conditions Allied-Lyons could have generated speculative gains. For illustrative purposes, assume that on January 15, 1991, Allied-Lyons had written sterling calls and puts with identical strike prices of $1.25 = £1 and respective premiums of 2. 70 cents and 3. 13 cents per pound. Was Allied-Lyons bullish or bearish on the dollar? If the dollar were to rebound to 1. 50 by March 1, how and when should Allied-Lyons hedge its otherwise speculative position? How would your answer differ if the straddle used American rather than European options?

Data from International Corporate Finance in Practice 7. 3

Transcribed Image Text:

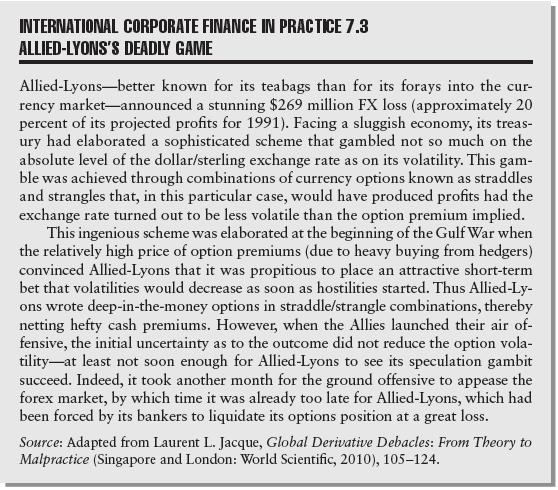

INTERNATIONAL CORPORATE FINANCE IN PRACTICE 7.3 ALLIED-LYONS'S DEADLY GAME Allied-Lyons better known for its teabags than for its forays into the cur- rency market-announced a stunning $269 million FX loss (approximately 20 percent of its projected profits for 1991). Facing a sluggish economy, its treas- ury had elaborated a sophisticated scheme that gambled not so much on the absolute level of the dollar/sterling exchange rate as on its volatility. This gam- ble was achieved through combinations of currency options known as straddles and strangles that, in this particular case, would have produced profits had the exchange rate turned out to be less volatile than the option premium implied. This ingenious scheme was elaborated at the beginning of the Gulf War when the relatively high price of option premiums (due to heavy buying from hedgers) convinced Allied-Lyons that it was propitious to place an attractive short-term bet that volatilities would decrease as soon as hostilities started. Thus Allied-Ly- ons wrote deep-in-the-money options in straddle/strangle combinations, thereby netting hefty cash premiums. However, when the Allies launched their air of- fensive, the initial uncertainty as to the outcome did not reduce the option vola- tility at least not soon enough for Allied-Lyons to see its speculation gambit succeed. Indeed, it took another month for the ground offensive to appease the forex market, by which time it was already too late for Allied-Lyons, which had been forced by its bankers to liquidate its options position at a great loss. Source: Adapted from Laurent L. Jacque, Global Derivative Debacles: From Theory to Malpractice (Singapore and London: World Scientific, 2010), 105-124.