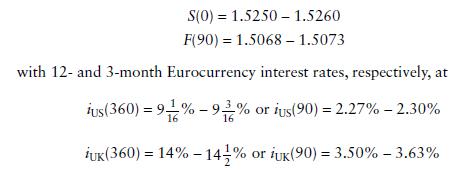

Interest rate arbitrage with bid-ask spreads (advanced). Consider the configuration of bid-ask spot and 90-day forward US$/

Question:

Interest rate arbitrage with bid-ask spreads (advanced). Consider the configuration of bid-ask spot and 90-day forward US$/£ exchange rate on June 12, 2013, keeping in mind that the lower rate is the selling/lending rate and conversely the higher rate is the buying/borrowing rate:

a. Compute the no-profit bid-ask 90-day forward rates.

b. Show how interest rate arbitrageurs can take advantage of the gap between no-profit and market bid-ask forward rates.

c. Explain how such arbitrage transactions should narrow the gap.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

Muhammad Rehan

Enjoy testing and can find bugs easily and help improve the product quality.

10+ Reviews

10+ Question Solved

Related Book For

International Corporate Finance Value Creation With Currency Derivatives In Global Capital Markets

ISBN: 9781119550464

2nd Edition

Authors: Laurent L. Jacque

Question Posted: