Exercise 11.11 reports ABC data for the three activity areas (cleaning, cutting and packaging) on a per

Question:

Exercise 11.11 reports ABC data for the three activity areas (cleaning, cutting and packaging) on a per output-unit basis (per kilogram of chips). This format emphasises product costing. An alternative approach that emphasises the costs of individual processes (activities) is to identify (a) the costs at each activity area, and (b) the rate per unit of the cost driver at each activity area. The following information pertains to (a) and (b):

● Cleaning activity area: McCarthy used 1.2 million kilograms of raw potatoes to yield 1 million kilograms of chips. No distinction is made as to the end-product when cleaning potatoes. The cost driver is kilograms of raw potatoes cleaned.

● Cutting activity area: McCarthy processes raw potatoes for the retail market independently of those processed for the institutional market. The production line produces (a) 250 kg of retail chips per cutting-hour, and (b) 400 kg of institutional chips per cutting-hour. The cost driver is cutting-hours on the production line.

● Packaging activity area: McCarthy packages chips for the retail market independently of those packaged for the institutional market. The packaging line packages (a) 25 kg of retail chips per packaging-hour, and (b) 100 kg of institutional chips per packaging-hour. The cost driver is packaging-hours on the production line.

Required

1. What are the total activity costs in the (a) cleaning, (b) cutting and (c) packaging activity areas?

2. What is the cost rate per unit of the cost driver in the (a) cleaning, (b) cutting and (c) packaging activity areas?

3. How might McCarthy Potatoes use information about the cost driver rates calculated in requirement 2 to better manage the Longford plant?

Data From Exercise 11.11

McCarthy Potatoes processes potatoes into chips at its highly automated Longford plant. For many years, it processed potatoes for only the retail consumer market where it had a superb reputation for quality. Recently, it started selling chips to the institutional market that includes hospitals, cafeterias and university halls of residence. Its penetration into the institutional market has been slower than predicted. McCarthy’s existing costing system has a single direct-cost category (direct materials, which are the raw potatoes) and a single indirect-cost pool (production support). Support costs are allocated on the basis of kilograms of chips processed. Support costs include packaging material. This year’s total actual costs for producing 1000,000 kg of chips (900,000 for the retail market and 100,000 for the institutional market) are:

Direct materials used ............................................ €150,000

Production support ................................................ €983,000

The existing costing system does not distinguish between chips produced for the retail or the institutional markets.

At the end of the year, McCarthy unsuccessfully bid for a large institutional contract. Its bid was reported to be 30% above the winning bid. This came as a shock as McCarthy included only a minimum profit margin on its bid. Moreover, the Longford plant was widely acknowledged as the most efficient in the industry.

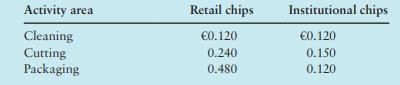

As part of its lost contract bid review process, McCarthy decided to explore several ways of refining its costing system. First, it identified that €188,000 of the €983,000 pertains to packaging materials that could be traced to individual jobs (€180,000 for retail and €8000 for institutional). These will now be classified as a direct material. The €150,000 of direct materials used were classified as €135,000 for retail and €15,000 for institutional. Second, it used activity-based costing (ABC) to examine how the two products (retail chips and institutional chips) used the support area differently. The finding was that three activity areas could be distinguished and that different usage occurred in two of these three areas. The indirect cost per kilogram of finished product at each activity area is as follows:

There was no opening or closing amount of any stock (materials, work in progress or finished goods).

Step by Step Answer:

Management And Cost Accounting

ISBN: 9781292232669

7th Edition

Authors: Alnoor Bhimani, Srikant M. Datar, Charles T. Horngren, Madhav V. Rajan