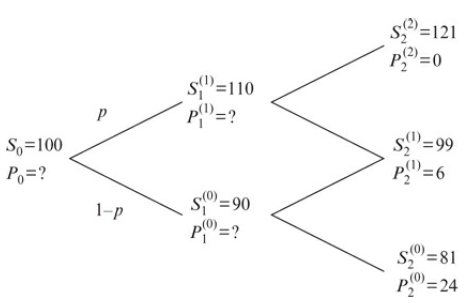

Look at the binomial tree in Figure 12.14. Assume that the risk-free interest rate vanishes, r =

Question:

Look at the binomial tree in Figure 12.14. Assume that the risk-free interest rate vanishes, r = 0%, and price the European plain vanilla put option by computing the hedge-portfolios ?(1)1, ?(1)1 and ?0.

Fig. 12.14?Binomial tree for European plain vanilla put option.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

The European plain vanilla put option is priced using the principle of no arbitrage meaning that the ...View the full answer

Answered By

FELIX NYAMBWOGI

I have been tutoring for over 5 years, both in person and online. I have experience tutoring a wide range of subjects, including math, science, English, and history. I have also worked with students of all ages, from elementary school to high school.

In addition, I have received training in effective tutoring strategies and techniques, such as active listening, questioning, and feedback. I am also proficient in using online tutoring platforms, such as Zoom and Google Classroom, to effectively deliver virtual lessons.

Overall, my hands-on experience and proficiency as a tutor has allowed me to effectively support and guide students in achieving their academic goals.

0 Reviews

10+ Question Solved

Related Book For

Question Posted: