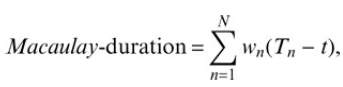

Show that Macaulay-duration is a weighted average of times to maturity where the weights w n are

Question:

Show that Macaulay-duration is a weighted average of times to maturity

where the weights wn are the fractions of the present value of the bond, represented by the n-th cashflow.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Let P be the present value of the bond Then for each cash flow the ...View the full answer

Answered By

SHINKI JALHOTRA

I have worked with other sites like Course Hero as a tutor and I have great knowledge on IT skills.

0 Reviews

10+ Question Solved

Related Book For

Question Posted: