Consider a European down-and-out partial barrier call option where the barrier provision is activated only between the

Question:

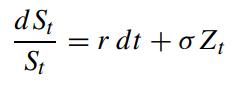

Consider a European down-and-out partial barrier call option where the barrier provision is activated only between the option’s starting date (time 0) and t1. Here, t1 is some time earlier than the expiration date T , where 0 1

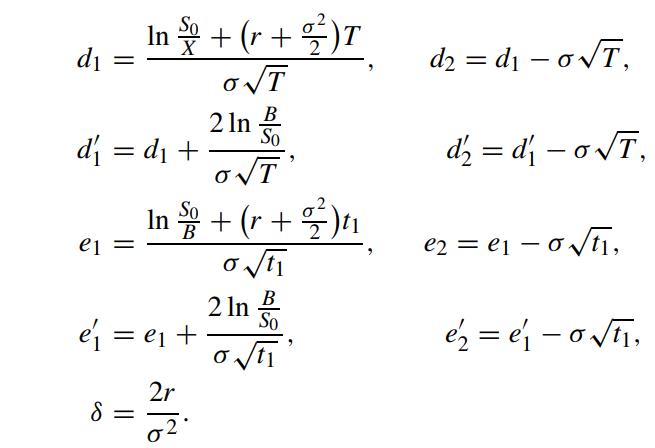

under the risk neutral measure Q. Assuming S0 > B, show that the down-andout call price is given by (Heynen and Kat, 1994a)

under the risk neutral measure Q. Assuming S0 > B, show that the down-andout call price is given by (Heynen and Kat, 1994a)

![call price e- Eq[(STX)1{St>x}1{ = {m}'>B}] 8+1 B = So [~ (d, es; 7) () ''N (d; Nd, - S - e -rT X Nd2, e2; X](https://dsd5zvtm8ll6.cloudfront.net/images/question_images/1700/4/8/2/590655b4e1e0583f1700482586128.jpg)

where

Show that the above price formula reduces to the price function defined in (4.1.12a,b) when t1 is set equal to T.

Modify the price formula in Problem 4.6 by setting ρ = √t1/T σ1 = σ and σ2 = √t1/T σ so that γ12 = 1.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

Cristine kanyaa

I possess exceptional research and essay writing skills. I have successfully completed over 5000 projects and the responses are positively overwhelming . I have experience in handling Coursework, Session Long Papers, Manuscripts, Term papers, & Presentations among others. I have access to both physical and online library. this makes me a suitable candidate to tutor clients as I have adequate materials to carry out intensive research.

1538+ Reviews

3254+ Question Solved

Related Book For

Question Posted: