Consider futures on an underlying asset that pays N discrete dividends between t and T and let

Question:

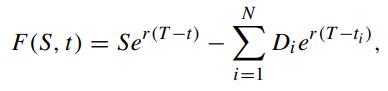

Consider futures on an underlying asset that pays N discrete dividends between t and T and let Di denote the amount of the ith dividend paid on the ex-dividend date ti. Show that the futures price is given by

where S is the current asset price and r is the riskless interest rate. Consider a European call option on the above futures. Show that the governing differential equation for the price of the call, cF (F, t), is given by (Brenner, Courtadon and Subrahmanyan, 1985)

![acF at + N [F + De] BFF - TF = 0. Die' (T- 2 rcf OF2 i=1](https://dsd5zvtm8ll6.cloudfront.net/images/question_images/1700/4/7/6/737655b3741319171700476730924.jpg)

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

To derive the futures price equation and the governing differential equation for the European call o...View the full answer

Answered By

Munibah Munir

I've done MS specialization in finance’s have command on accounting and financial management. Forecasting and Financial Statement Analysis is basic field of my specialization. On many firms I have done real base projects in financial management field special forecasting. I have served more than 500 Clients for more than 800 business projects, and I have got a very high repute in providing highly professional and quality services.I have capability of performing extra-ordinarily well in limited time and at reasonable fee. My clients are guaranteed full satisfaction and I make things easy for them. I am capable of handling complex issues in the mentioned areas and never let my clients down.

467+ Reviews

648+ Question Solved

Related Book For

Question Posted: