Let u and d denote the state prices corresponding to the states of asset value

Question:

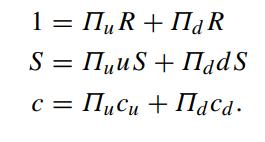

Let Πu and Πd denote the state prices corresponding to the states of asset value going up and going down, respectively. The state prices can also be interpreted as state contingent discount rates. If no arbitrage opportunities are available, then all securities (including the bond, the asset and the call option) must have returns with the same state contingent discount rates Πu and Πd. Hence, the respective relations for the money market account, asset price and call option value with Πu and Πd are given by

By solving for Πu and Πd from the first two equations and substituting the solutions into the third equation, show that the binomial call price formula over one period is given by

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Lets denote the state contingent discount rates as II and II The relations for the money market acco...View the full answer

Answered By

Ehsan Mahmood

I’ve earned Masters Degree in Business Studies and specialized in Accounts & Finance. Couple with this, I have earned BS Sociology from renowned institute of Pakistan. Moreover, I have humongous teaching experience at Graduate and Post-graduate level to Business and humanities students along with more than 7 years of teaching experience to my foreign students Online. I’m also professional writer and write for numerous academic journals pertaining to educational institutes periodically.

248+ Reviews

287+ Question Solved

Related Book For

Question Posted: