Threatened by a declining share of the long-distance phone service market, Noy Holland, Vice President, Consumer Service,

Question:

Threatened by a declining share of the long-distance phone service market, Noy Holland, Vice President, Consumer Service, KLR Communications, suggests at a sales retreat that KLR bank on the reputation of Cheever & Yates, KLR's independent auditors, to vouch for claims made by KLR in their current advertising campaign. Holland says, "We say, You save with KLR. But who has reason to believe us? Particularly when Continental holds 70 percent of the market (even after the divestiture)! We need something, some hook, something that will give the market reason to believe us, something other than what we have now, when what we have now translates to nothing more than 'Trust us'."

Holland suggests a bold new advertising plan, what she coins "You're Ahead," a multimillion-dollar print, TV, and radio campaign that promises the unthinkable to preferred, corporate, long-distance customers: quarterly statements that: (1) compare the rates charged by KLR with the lowest rates published by Continental, and (2) extend a credit for the amount by which KLR charged more.

"What if we're not priced below Continental?" asks Sam Michel, KLR's chief financial officer.

"The question, Sam, is 'What if we are?'" Holland says.

The vice presidents for sales and for operations agree with Holland, and so in time does Michel. Gary Lutz, President and Board Chairman, asks Michel to contact Richard Yates, engagement partner for Cheever & Yates.

At a meeting among Richard Yates, Gary Lutz, Sam Michel, and Noy Holland, Michel proposes a methodology for comparing KLR's monthly bills with Continental Communication's published rates. Michel asks that Yates propose an attestation engagement to attest to the methodology.

"What, precisely, are you asking us to attest to?" asks Yates.

"Noy and our legal staff drafted what we need," says Lutz, "and what we apparently need is a statement from you that our methodology properly compares billing charges between KLR and Continental, and accurately reflects the price differences for the period July 1, 1999 through September 30, 1999, which is the first period we're offering the guarantee."

"For actual usage billed by KLR?" asks Yates.

"Yes," says Holland, "and—and Gary knows this—between alternative KLR services, since we'd like to offer a review not only against Continental, as Gary said, but also against our own alternative pricing plans, so the customer knows they're beating Continental and getting the best price we offer."

"This is risky," says Yates.

"To us?" asks Lutz.

"To us," says Yates. "What we're attesting to could be misrepresented in your written promotional materials or, for that matter, orally by your sales reps."

"What will you agree to?" asks Holland.

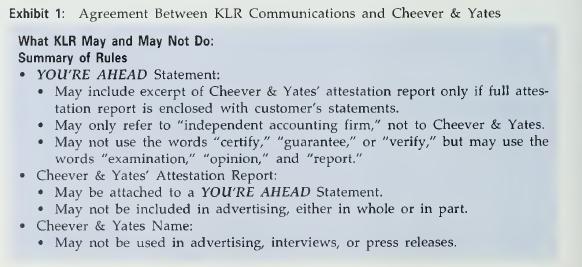

"This agreement," says Yates, referring to the contents of Exhibit 1.

Lutz, Michel, and Holland read the agreement. Michel asks, "Why are we precluded from using an excerpt of your firm's attestation unless we include a full attestation report with a customer's statement?"

"We can't risk a customer taking the excerpt out of context," says Yates.

"But including a full report will increase our billing costs/' says Michel.

"We can't take the risk," says Yates.

"And we can't use your firm's name?" asks Lutz.

"Only insofar as our name appears on the full attestation report," says Yates.

"Nowhere else."

"Why?"

"Because all I can offer you is an attestation on your methodology, not on your services," answers Yates.

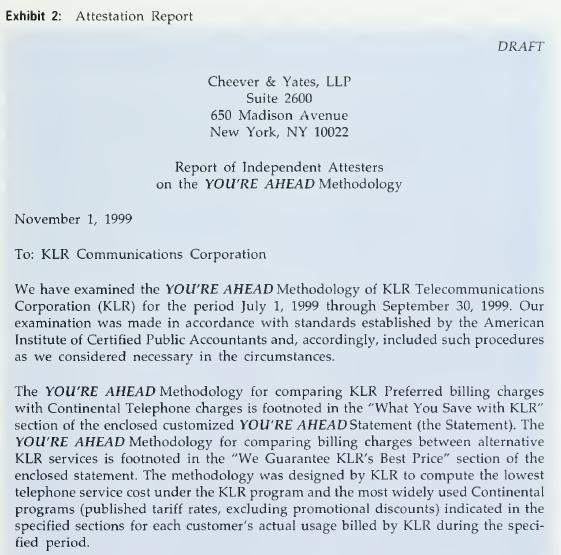

"And your report," says Michel. "What will your report look like?"

"I have a draft," says Yates, referring to Exhibit 2.

"This language," says Lutz. "We need stronger language."

"This language is the language required by our standards. We can offer no stronger statement."

Yates then explains that the attestation reporting standards (Chapter 2) are at the center of the language chosen by Cheever & Yates. Consistent with the first and second reporting standards, the draft:

1. Identifies the assertion attested to in the second paragraph (the accuracy of the "You're Ahead" Methodology for comparing KLR Preferred billing charges with Continental Telephone charges), 2. States the character of the engagement in the first paragraph (to examine the "You're Ahead" Methodology of KLR Telecommunications Corporation (KLR) for the period July 1, 1999 through September 30, 1999 in accordance with AICPA standards), and 3. States the firm's conclusion about whether the assertion is presented in conformity with the criteria against which it was measured in the third paragraph (the "You're Ahead" Methodology properly compares billing charges between KLR and Continental and between alternative KLR services and accurately reflects the price differences for the period July 1, 1999 through September 30, 1999).

Gary Lutz agrees both to the rules in Exhibit 1 and to the attestation report in Exhibit 2.

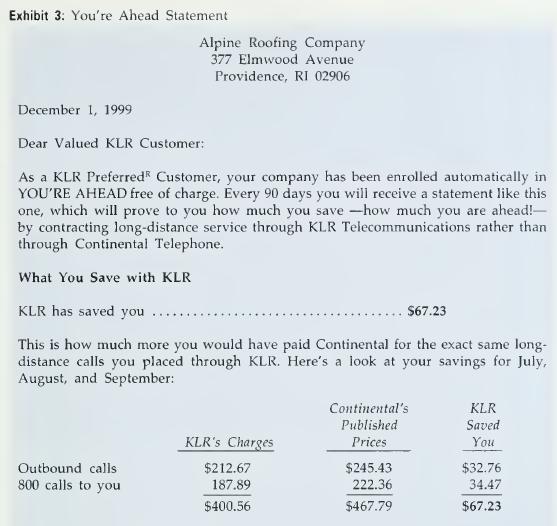

"And the 'You're Ahead' Statement," says Yates. "You have a draft?"

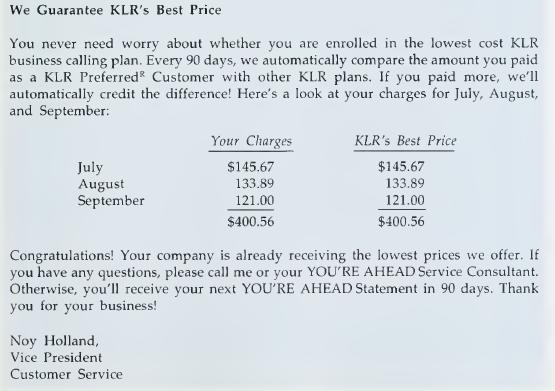

Noy Holland presents the statement in Exhibit 3, an exact duplicate for a customer, the Alpine Roofing Company.

Yates agrees to the "You're Ahead" statement, but asks what Holland proposes to excerpt from the attestation report. She types out the following:

Excerpt from independent attester's report:

"In our opinion, the 'You're Ahead' Methodology properly compares billing charges between KLR and Continental and between alternative KLR services and accurately reflects the price differences."

Turning the screen toward Yates, she says, "We'll use this below my facsimile signature on the statement."

Yates offers to deliver an engagement letter to Lutz after discussing the proposed engagement with the firm's managing partner. "But certainly by next week," Yates says.

The attestation report would be dated November 1, 1999.

Required:

As the profession ventures into new markets, the leadership in public accounting firms is confronted with questions they've not dealt with routinely in the past: For example, can we be profitable in the wake of uncertain risks and near certain liability? Why are companies like KLR approaching us if not in part to shift the risk of liability? Are we venturing into markets that we do not belong? In considering the following issues, assume that you are the managing partner of Cheever & Yates. Be mindful of the issues above as you consider the following questions. Be as critical of Richard Yates' proposed attestation service for KLR Communications as any managing partner would be of any engagement partner whose incentive compensation scheme is weighted in part on securing new business. The following questions correspond to Chapters 1-7 of the book:

Chapter 1: Is this engagement advisable? If Cheever & Yates leverages off of the KLR engagement to market similar services in other industries, do you see problems related to market permissions and market sizing?

Chapter 2: Discuss how you would comply with each of the AICPA's Attestation Standards.

Chapter 3: Discuss the deficiencies in Yates' proposed attestation report. How would you improve the report?

Chapter 4: Discuss the ethical issues you find important to the engagement.

Chapter 5: Discuss the liability issues you find important to the engagement.

Chapter 6: Discuss the risks you see accruing to Cheever & Yates from the wording of the agreement with KLR Communications and KLR's "You're Ahead"

Statement. Discuss how Cheever & Yates will gather and evaluate evidence.

Chapter 7: Discuss the information systems, technology, and internal control issues you find important to the engagement.

Step by Step Answer: