Suppose you are researching Astra International (Indonesia Stock Exchange: ASII) and are interested in Astras price action

Question:

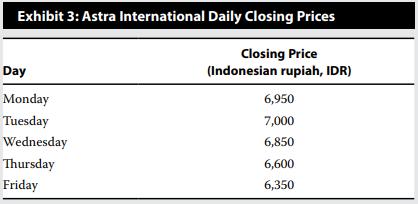

Suppose you are researching Astra International (Indonesia Stock Exchange: ASII) and are interested in Astra’s price action in a week in which international economic news had significantly affected the Indonesian stock market. You decide to use volatility as a measure of the variability of Astra shares during that week. Exhibit 3 shows closing prices during that week.

Use the data provided to do the following:

1. Estimate the volatility of Astra shares. (Annualize volatility on the basis of 250 trading days in a year.)

2. Calculate an estimate of the expected continuously compounded annual return for Astra.

3. Discuss why it may not be prudent to use the sample mean daily return to estimate the expected continuously compounded annual return for Astra.

4. Identify the probability distribution for Astra share prices if continuously compounded daily returns follow the normal distribution.

Step by Step Answer:

1 First calculate the continuously compounded daily returns then find their standard deviation in th...View the full answer