Starr, CPA, is performing the financial statement audit of Brenda. Inc. In performing this audit, Starr has

Question:

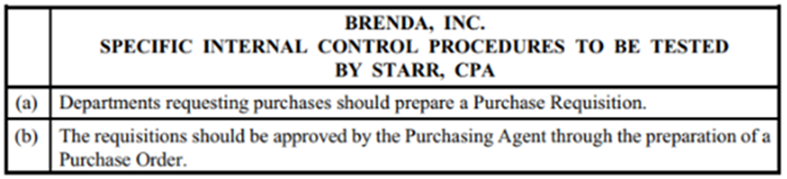

Starr, CPA, is performing the financial statement audit of Brenda. Inc. In performing this audit, Starr has determined that she needs to perform tests of controls on the procedures used by Brenda to approve purchases made on account. Specifically, Brenda's internal control includes the following control procedures.

Once items purchased by Brenda are received. they are recorded in the Voucher Register. Starr feels that any cases where either of the controls arc not functioning raise serious concerns about Brenda's internal controls.

REQUIRED:

(1) What would Starr consider to be a deviation condition in this situation?

(2) How should Starr define the population? For each item selected from the population, which procedure(s) should Starr perform?

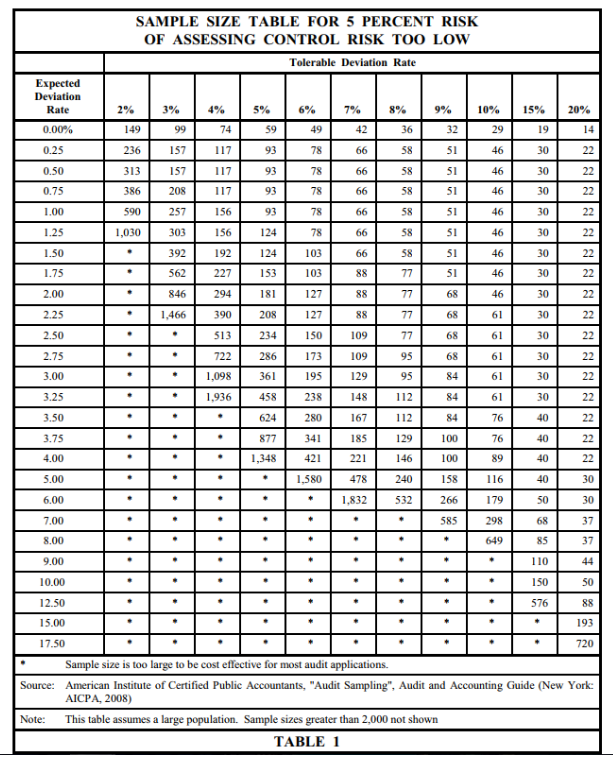

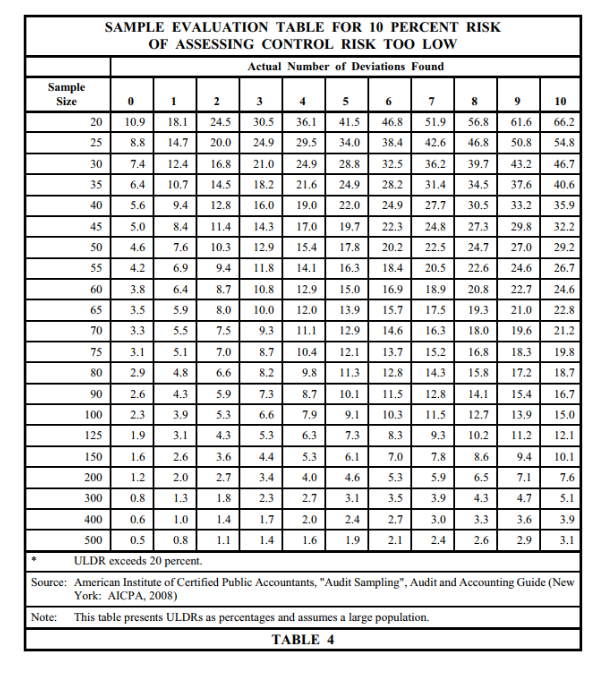

(3) Assume that Starr decided upon a risk of overreliance of 5% and a tolerable deviation rate of 4%. In addition, based on her previous experience. Starr expected a deviation rate in the population of 1.25%. What sample size should be selected by Starr?

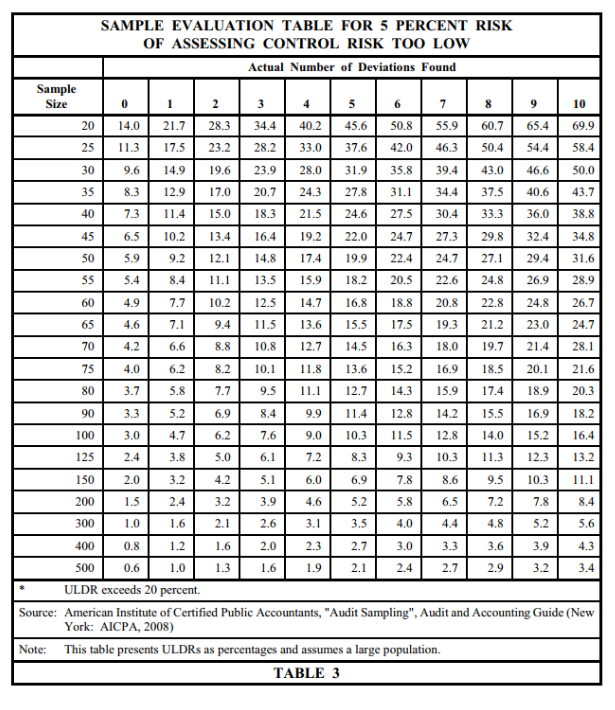

(4) Ignoring your answer to Question 3 above, assume that Starr examined 200 items and found 8 deviations.

(a) What is the sample deviation rate?

(b) What is the upper precision limit?

(c) What does the upper precision limit tell Starr?

Expert Answer:

1 A deviation would be the purchaser creating a purchase order without a requisition from any person ... View the full answer

Auditing A Practical Approach

ISBN: 978-1119566007

3rd Canadian edition

Authors: Robyn Moroney, Fiona Campbell, Jane Hamilton, Valerie Warren