1. A portfolio has a total value of $160,000,000. The portfolio consists of $100,000,000 in US...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

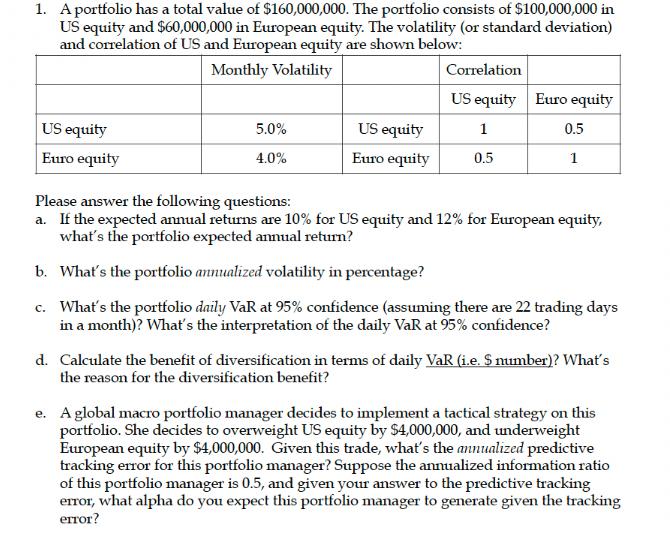

1. A portfolio has a total value of $160,000,000. The portfolio consists of $100,000,000 in US equity and $60,000,000 in European equity. The volatility (or standard deviation) and correlation of US and European equity are shown below: Monthly Volatility US equity Euro equity 5.0% 4.0% US equity Euro equity Correlation US equity 1 0.5 Euro equity 0.5 1 Please answer the following questions: a. If the expected annual returns are 10% for US equity and 12% for European equity, what's the portfolio expected annual return? b. What's the portfolio annualized volatility in percentage? c. What's the portfolio daily VaR at 95% confidence (assuming there are 22 trading days in a month)? What's the interpretation of the daily VaR at 95% confidence? d. Calculate the benefit of diversification in terms of daily VaR (i.e. S number)? What's the reason for the diversification benefit? e. A global macro portfolio manager decides to implement a tactical strategy on this portfolio. She decides to overweight US equity by $4,000,000, and underweight European equity by $4,000,000. Given this trade, what's the annualized predictive tracking error for this portfolio manager? Suppose the annualized information ratio of this portfolio manager is 0.5, and given your answer to the predictive tracking error, what alpha do you expect this portfolio manager to generate given the tracking error? 2. Suppose the geometric mean for Japanese Government Bond monthly return in a year is 1.75% and arithmetic mean is 2%. Suppose the Emerging market equity is twice as volatile as the Japanese bond in the same period. a. If the geometric mean for emerging market equity monthly return is 2% in a year, what's the arithmetic mean of the Emerging market equity monthly return in a year? 3. For the pension plan of a company XYZ, the strategic asset allocation is 60% in global equity and 35% in global fixed income and 5% in US cash. a. If the global equity market generates negative return and bond yield declines in the coming year, what will happen to the PBO funded ratio? Why? b. The pension plan sponsor of company XYZ wants to reduce the risk of the portfolio. His suggestion is to increase the cash allocation from 5% to 20% since cash is the "risk-free" asset. Considering cash as an asset and as an investment in a pension portfolio, do you agree with his suggestion? Why? c. The pension plan sponsor expects the asset return to be low and bond yield remains low in the future. Suppose the pension plan has a PBO funded ratio of 85% currently. In order to minimize the amount of corporate contribution to the pension plan and increase funded ratio, the pension plan sponsor is very interested in applying the Alpha Beta framework to his pension fund. Please provide your recommendation using Alpha/Beta investment framework. What should be the new asset allocation strategy? How much active risk should the pension plan take? Be specific and provide the rationale for your recommendation. d. In particular, the pension plan sponsor is considering investing in hedge fund. Do you think hedge fund is a good investment vehicle for the pension plan? Give a detailed discussion of hedge funds as an investment in pension plans. Be thorough in your answers. 4. An endowment Chief Investment Officer is considering investment ($100 million) with an active global equity manager. One candidate manager is a fundament driven stock picker (very similar to the China Fund manager that we have talked about in the class). The fundamental manager runs a strategy that has an alpha target of 5% and a track error target of 10%. The other candidate manager is a quantitatively driven active equity manager (very similar to GSAM case as we have discussed in the class). The quantitative manager has an alpha target of 2.5% and a tracking error target of 3.5%. The two managers' alpha streams historically have a correlation of 0.1. a. Please comment on the pros and cons of these two investment styles (fundamental vs. quantitative) for active equity management. b. How would you recommend the endowment CIO to structure her active global equity allocation ($100 million)? Specifically, should she hire one manager vs. another? Should she split her allocation between the two managers? If so, what's the split? Please provide detailed rationale for your recommendation. 1. A portfolio has a total value of $160,000,000. The portfolio consists of $100,000,000 in US equity and $60,000,000 in European equity. The volatility (or standard deviation) and correlation of US and European equity are shown below: Monthly Volatility US equity Euro equity 5.0% 4.0% US equity Euro equity Correlation US equity 1 0.5 Euro equity 0.5 1 Please answer the following questions: a. If the expected annual returns are 10% for US equity and 12% for European equity, what's the portfolio expected annual return? b. What's the portfolio annualized volatility in percentage? c. What's the portfolio daily VaR at 95% confidence (assuming there are 22 trading days in a month)? What's the interpretation of the daily VaR at 95% confidence? d. Calculate the benefit of diversification in terms of daily VaR (i.e. S number)? What's the reason for the diversification benefit? e. A global macro portfolio manager decides to implement a tactical strategy on this portfolio. She decides to overweight US equity by $4,000,000, and underweight European equity by $4,000,000. Given this trade, what's the annualized predictive tracking error for this portfolio manager? Suppose the annualized information ratio of this portfolio manager is 0.5, and given your answer to the predictive tracking error, what alpha do you expect this portfolio manager to generate given the tracking error? 2. Suppose the geometric mean for Japanese Government Bond monthly return in a year is 1.75% and arithmetic mean is 2%. Suppose the Emerging market equity is twice as volatile as the Japanese bond in the same period. a. If the geometric mean for emerging market equity monthly return is 2% in a year, what's the arithmetic mean of the Emerging market equity monthly return in a year? 3. For the pension plan of a company XYZ, the strategic asset allocation is 60% in global equity and 35% in global fixed income and 5% in US cash. a. If the global equity market generates negative return and bond yield declines in the coming year, what will happen to the PBO funded ratio? Why? b. The pension plan sponsor of company XYZ wants to reduce the risk of the portfolio. His suggestion is to increase the cash allocation from 5% to 20% since cash is the "risk-free" asset. Considering cash as an asset and as an investment in a pension portfolio, do you agree with his suggestion? Why? c. The pension plan sponsor expects the asset return to be low and bond yield remains low in the future. Suppose the pension plan has a PBO funded ratio of 85% currently. In order to minimize the amount of corporate contribution to the pension plan and increase funded ratio, the pension plan sponsor is very interested in applying the Alpha Beta framework to his pension fund. Please provide your recommendation using Alpha/Beta investment framework. What should be the new asset allocation strategy? How much active risk should the pension plan take? Be specific and provide the rationale for your recommendation. d. In particular, the pension plan sponsor is considering investing in hedge fund. Do you think hedge fund is a good investment vehicle for the pension plan? Give a detailed discussion of hedge funds as an investment in pension plans. Be thorough in your answers. 4. An endowment Chief Investment Officer is considering investment ($100 million) with an active global equity manager. One candidate manager is a fundament driven stock picker (very similar to the China Fund manager that we have talked about in the class). The fundamental manager runs a strategy that has an alpha target of 5% and a track error target of 10%. The other candidate manager is a quantitatively driven active equity manager (very similar to GSAM case as we have discussed in the class). The quantitative manager has an alpha target of 2.5% and a tracking error target of 3.5%. The two managers' alpha streams historically have a correlation of 0.1. a. Please comment on the pros and cons of these two investment styles (fundamental vs. quantitative) for active equity management. b. How would you recommend the endowment CIO to structure her active global equity allocation ($100 million)? Specifically, should she hire one manager vs. another? Should she split her allocation between the two managers? If so, what's the split? Please provide detailed rationale for your recommendation. 1. A portfolio has a total value of $160,000,000. The portfolio consists of $100,000,000 in US equity and $60,000,000 in European equity. The volatility (or standard deviation) and correlation of US and European equity are shown below: Monthly Volatility US equity Euro equity 5.0% 4.0% US equity Euro equity Correlation US equity 1 0.5 Euro equity 0.5 1 Please answer the following questions: a. If the expected annual returns are 10% for US equity and 12% for European equity, what's the portfolio expected annual return? b. What's the portfolio annualized volatility in percentage? c. What's the portfolio daily VaR at 95% confidence (assuming there are 22 trading days in a month)? What's the interpretation of the daily VaR at 95% confidence? d. Calculate the benefit of diversification in terms of daily VaR (i.e. S number)? What's the reason for the diversification benefit? e. A global macro portfolio manager decides to implement a tactical strategy on this portfolio. She decides to overweight US equity by $4,000,000, and underweight European equity by $4,000,000. Given this trade, what's the annualized predictive tracking error for this portfolio manager? Suppose the annualized information ratio of this portfolio manager is 0.5, and given your answer to the predictive tracking error, what alpha do you expect this portfolio manager to generate given the tracking error? 2. Suppose the geometric mean for Japanese Government Bond monthly return in a year is 1.75% and arithmetic mean is 2%. Suppose the Emerging market equity is twice as volatile as the Japanese bond in the same period. a. If the geometric mean for emerging market equity monthly return is 2% in a year, what's the arithmetic mean of the Emerging market equity monthly return in a year? 3. For the pension plan of a company XYZ, the strategic asset allocation is 60% in global equity and 35% in global fixed income and 5% in US cash. a. If the global equity market generates negative return and bond yield declines in the coming year, what will happen to the PBO funded ratio? Why? b. The pension plan sponsor of company XYZ wants to reduce the risk of the portfolio. His suggestion is to increase the cash allocation from 5% to 20% since cash is the "risk-free" asset. Considering cash as an asset and as an investment in a pension portfolio, do you agree with his suggestion? Why? c. The pension plan sponsor expects the asset return to be low and bond yield remains low in the future. Suppose the pension plan has a PBO funded ratio of 85% currently. In order to minimize the amount of corporate contribution to the pension plan and increase funded ratio, the pension plan sponsor is very interested in applying the Alpha Beta framework to his pension fund. Please provide your recommendation using Alpha/Beta investment framework. What should be the new asset allocation strategy? How much active risk should the pension plan take? Be specific and provide the rationale for your recommendation. d. In particular, the pension plan sponsor is considering investing in hedge fund. Do you think hedge fund is a good investment vehicle for the pension plan? Give a detailed discussion of hedge funds as an investment in pension plans. Be thorough in your answers. 4. An endowment Chief Investment Officer is considering investment ($100 million) with an active global equity manager. One candidate manager is a fundament driven stock picker (very similar to the China Fund manager that we have talked about in the class). The fundamental manager runs a strategy that has an alpha target of 5% and a track error target of 10%. The other candidate manager is a quantitatively driven active equity manager (very similar to GSAM case as we have discussed in the class). The quantitative manager has an alpha target of 2.5% and a tracking error target of 3.5%. The two managers' alpha streams historically have a correlation of 0.1. a. Please comment on the pros and cons of these two investment styles (fundamental vs. quantitative) for active equity management. b. How would you recommend the endowment CIO to structure her active global equity allocation ($100 million)? Specifically, should she hire one manager vs. another? Should she split her allocation between the two managers? If so, what's the split? Please provide detailed rationale for your recommendation. 1. A portfolio has a total value of $160,000,000. The portfolio consists of $100,000,000 in US equity and $60,000,000 in European equity. The volatility (or standard deviation) and correlation of US and European equity are shown below: Monthly Volatility US equity Euro equity 5.0% 4.0% US equity Euro equity Correlation US equity 1 0.5 Euro equity 0.5 1 Please answer the following questions: a. If the expected annual returns are 10% for US equity and 12% for European equity, what's the portfolio expected annual return? b. What's the portfolio annualized volatility in percentage? c. What's the portfolio daily VaR at 95% confidence (assuming there are 22 trading days in a month)? What's the interpretation of the daily VaR at 95% confidence? d. Calculate the benefit of diversification in terms of daily VaR (i.e. S number)? What's the reason for the diversification benefit? e. A global macro portfolio manager decides to implement a tactical strategy on this portfolio. She decides to overweight US equity by $4,000,000, and underweight European equity by $4,000,000. Given this trade, what's the annualized predictive tracking error for this portfolio manager? Suppose the annualized information ratio of this portfolio manager is 0.5, and given your answer to the predictive tracking error, what alpha do you expect this portfolio manager to generate given the tracking error? 2. Suppose the geometric mean for Japanese Government Bond monthly return in a year is 1.75% and arithmetic mean is 2%. Suppose the Emerging market equity is twice as volatile as the Japanese bond in the same period. a. If the geometric mean for emerging market equity monthly return is 2% in a year, what's the arithmetic mean of the Emerging market equity monthly return in a year? 3. For the pension plan of a company XYZ, the strategic asset allocation is 60% in global equity and 35% in global fixed income and 5% in US cash. a. If the global equity market generates negative return and bond yield declines in the coming year, what will happen to the PBO funded ratio? Why? b. The pension plan sponsor of company XYZ wants to reduce the risk of the portfolio. His suggestion is to increase the cash allocation from 5% to 20% since cash is the "risk-free" asset. Considering cash as an asset and as an investment in a pension portfolio, do you agree with his suggestion? Why? c. The pension plan sponsor expects the asset return to be low and bond yield remains low in the future. Suppose the pension plan has a PBO funded ratio of 85% currently. In order to minimize the amount of corporate contribution to the pension plan and increase funded ratio, the pension plan sponsor is very interested in applying the Alpha Beta framework to his pension fund. Please provide your recommendation using Alpha/Beta investment framework. What should be the new asset allocation strategy? How much active risk should the pension plan take? Be specific and provide the rationale for your recommendation. d. In particular, the pension plan sponsor is considering investing in hedge fund. Do you think hedge fund is a good investment vehicle for the pension plan? Give a detailed discussion of hedge funds as an investment in pension plans. Be thorough in your answers. 4. An endowment Chief Investment Officer is considering investment ($100 million) with an active global equity manager. One candidate manager is a fundament driven stock picker (very similar to the China Fund manager that we have talked about in the class). The fundamental manager runs a strategy that has an alpha target of 5% and a track error target of 10%. The other candidate manager is a quantitatively driven active equity manager (very similar to GSAM case as we have discussed in the class). The quantitative manager has an alpha target of 2.5% and a tracking error target of 3.5%. The two managers' alpha streams historically have a correlation of 0.1. a. Please comment on the pros and cons of these two investment styles (fundamental vs. quantitative) for active equity management. b. How would you recommend the endowment CIO to structure her active global equity allocation ($100 million)? Specifically, should she hire one manager vs. another? Should she split her allocation between the two managers? If so, what's the split? Please provide detailed rationale for your recommendation.

Expert Answer:

Answer rating: 100% (QA)

Lets address each question one by one Portfolio Analysis a To find the portfolios expected annual return you can use a weighted average of the expected returns for US and European equity Portfolio Exp... View the full answer

Related Book For

Fundamentals of Cost Accounting

ISBN: 978-0077398194

3rd Edition

Authors: William Lanen, Shannon Anderson, Michael Maher

Posted Date:

Students also viewed these finance questions

-

A large pipe called a penstock in hydraulic workis 1.5in diameter. The pipe thick with a maximum tensile strength of 300Mpa a. Determine the max bursting pressure (Kpa) if the max depth of water in...

-

Managing Scope Changes Case Study Scope changes on a project can occur regardless of how well the project is planned or executed. Scope changes can be the result of something that was omitted during...

-

The following additional information is available for the Dr. Ivan and Irene Incisor family from Chapters 1-5. Ivan's grandfather died and left a portfolio of municipal bonds. In 2012, they pay Ivan...

-

Jack Williams works in a very active department called purchasing. He works with store managers, marketing, and supply companies. The people in his department try to have the right product, in the...

-

Twelve million people in the United States are allergic to one or more food ingredients, and every three minutes, on average, one of these allergy sufferers ends up in a hospital emergency room.14...

-

Refer to the information in BE6-4. Calculate ending inventory and cost of goods sold for 2012, assuming the company uses specific identification. Actual sales by the company include its entire...

-

When a board member leaves the board, when is it desirable or wise to keep this person involved with the organization? How could this be accomplished?

-

Refer to the data in E24-17. Requirements 1. Calculate each divisions RI. Interpret your results. 2. Calculate each divisions EVA. Interpret your results.

-

What is the price of a $1,000 par value, 5.0% semi-annual coupon bond that matures i if investors require a 6.0% return. Round your answer to the nearest dollar. A

-

All the following case study questions are based on this book: Project management achieving competitive advantage by Jeffrey K. Pinto Question 8.1 1. Given the history of large cost overruns...

-

2. Ms. Melody decided to invest 800 dollars per month in her pension fund at the beginning of each month (6% annual rate), for thirty years, before her retirement. Ms. Melody also decided that, at...

-

Define Current Operations Intelligence . Provide an example of a current threat that our country would monitor using this intelligence strategy. Explain why this threat would meet the criteria for ...

-

Explain Robert Jervis' major scholarly contribution in his article Realism, Game Theory, and Cooperation is reducing the seemingly inscrutable caprice of political leader's decisions to a formula...

-

Read the Overview in regard to Senate Bill 158 (which is the latest Kentucky Education Accountability model). Identify two things you found most interesting in the Bill and why you found these items...

-

Walmart's Everyday Low Pricing (EDLP) strategy plays a large part in its tremendous success in the retail industry. However, setting prices low in order to limit or eliminate competition (predatory...

-

5. A 0.01kg cube slides around the inside of a vertically oriented tube at a constant rate. The tube, shown in the figure, is 0.12m in diameter. The coefficient of static friction between the tube...

-

(Apply legal principles in property law matters) On the 8 March 2018 Andrew , Bill , Charles and David buy a land. The land is bought in fee simple as " Andrew as to 1/4th share and Bill as to 1/4th...

-

On October 1, 2014, the Dow Jones Industrial Average (DJIA) opened at 17,042 points. During that day it lost 237 points. On October 2 it lost 4 points. On October 3 it gained 209 points. Deter-mine...

-

It has been said that a prior departments costs behave similarly to direct materials costs. Under what conditions are the costs similar? Why account for them separately?

-

Peninsula Candy Company makes three types of candy bars: Chewy, Chunky, and Choco-Lite (Lite). Sales volume for the annual budget is determined by estimating the total market volume for candy bars...

-

Sell Block prepares three types of simple tax returns: individual, partnerships, and (small) corporations. The tax returns have the following characteristics: The total fixed costs per year for the...

-

Minta Perry has received year-end information, including financial statements, from her accountant. Among the information is a report that the accounts receivable turnover ratio in the prior year was...

-

Tanisha Greggs, a stockholder in Mentar Corp., has just received a report of the companys ten-year financial performance that includes the following graph. In the report, management states that the...

-

Using the accrual accounting basis, when are revenues and expenses recognized?

Study smarter with the SolutionInn App