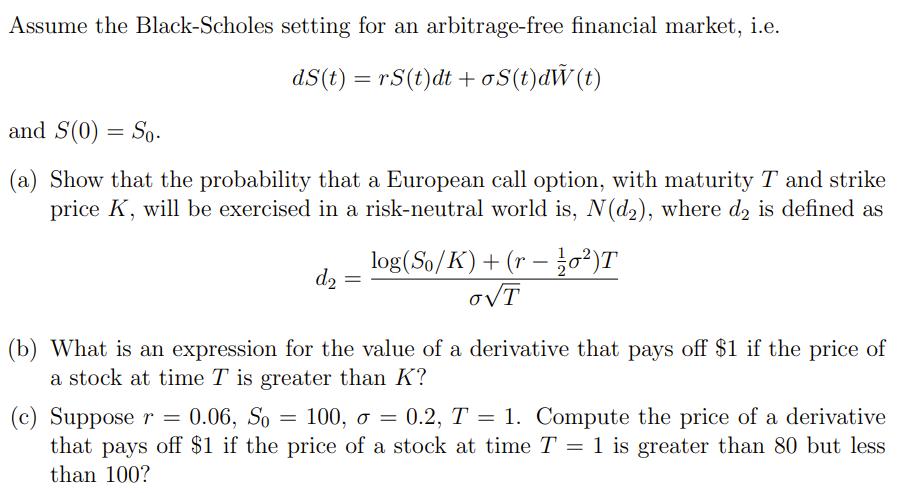

Assume the Black-Scholes setting for an arbitrage-free financial market, i.e. dS(t) = rS(t)dt + o S(t)dW(t)...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

a The probability that a European call option with maturity T and strike price K will be exercised i... View the full answer

Related Book For

Introduction to Probability and Statistics

ISBN: 978-1133103752

14th edition

Authors: William Mendenhall, Robert Beaver, Barbara Beaver

Posted Date: