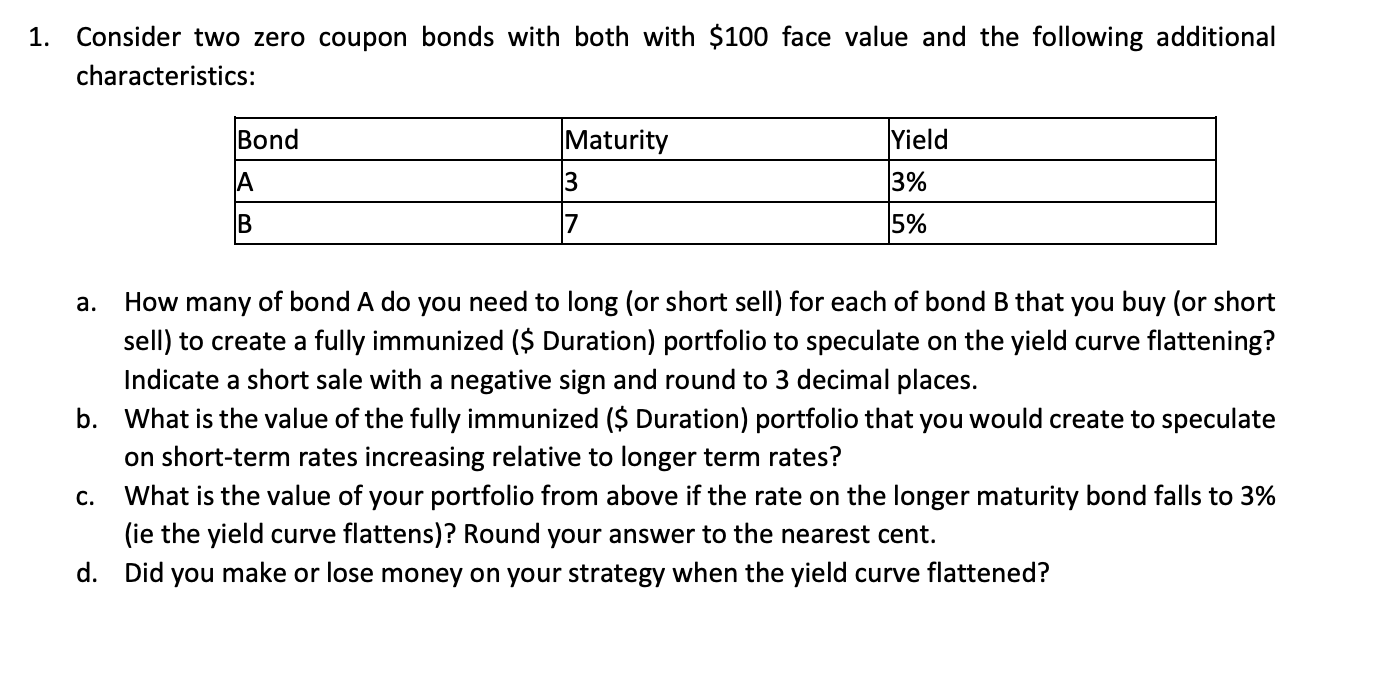

1. Consider two zero coupon bonds with both with $100 face value and the following additional...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

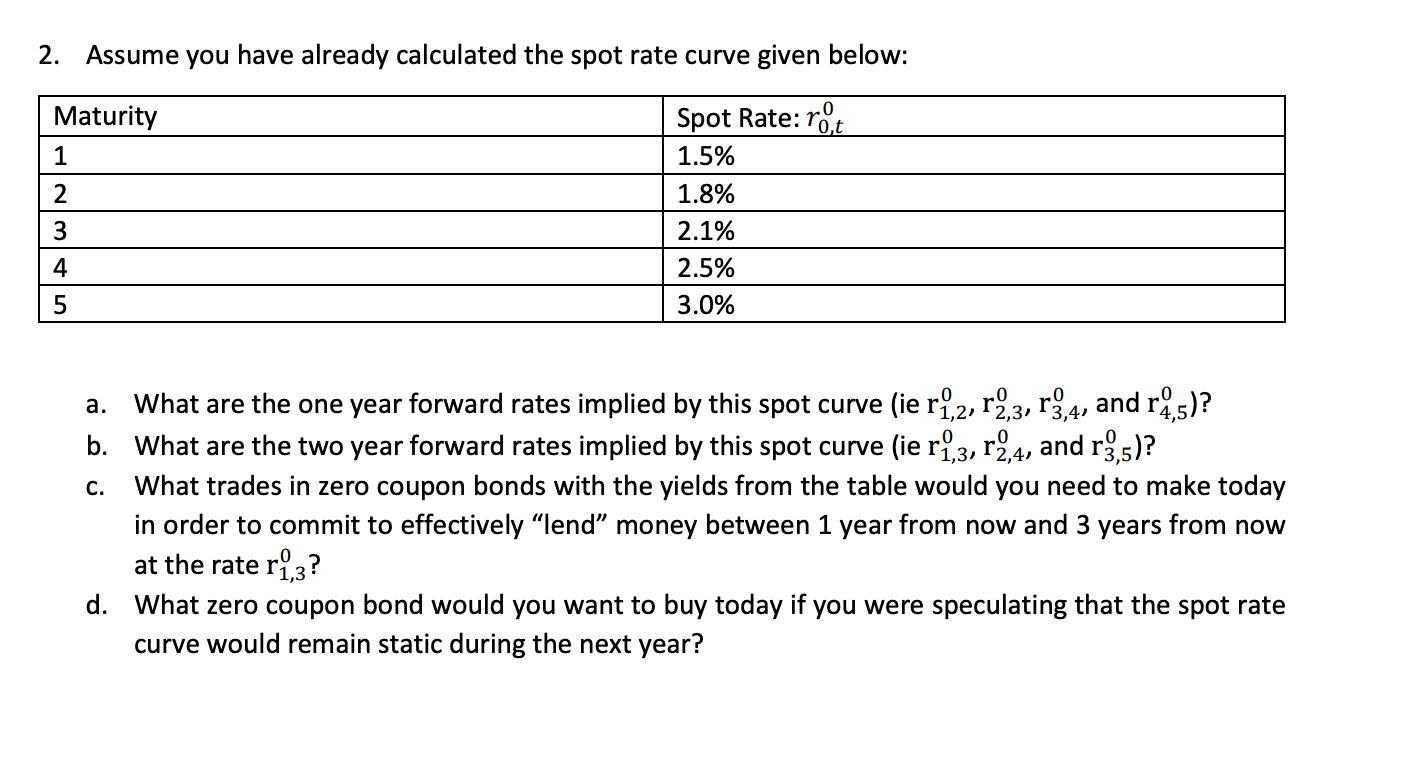

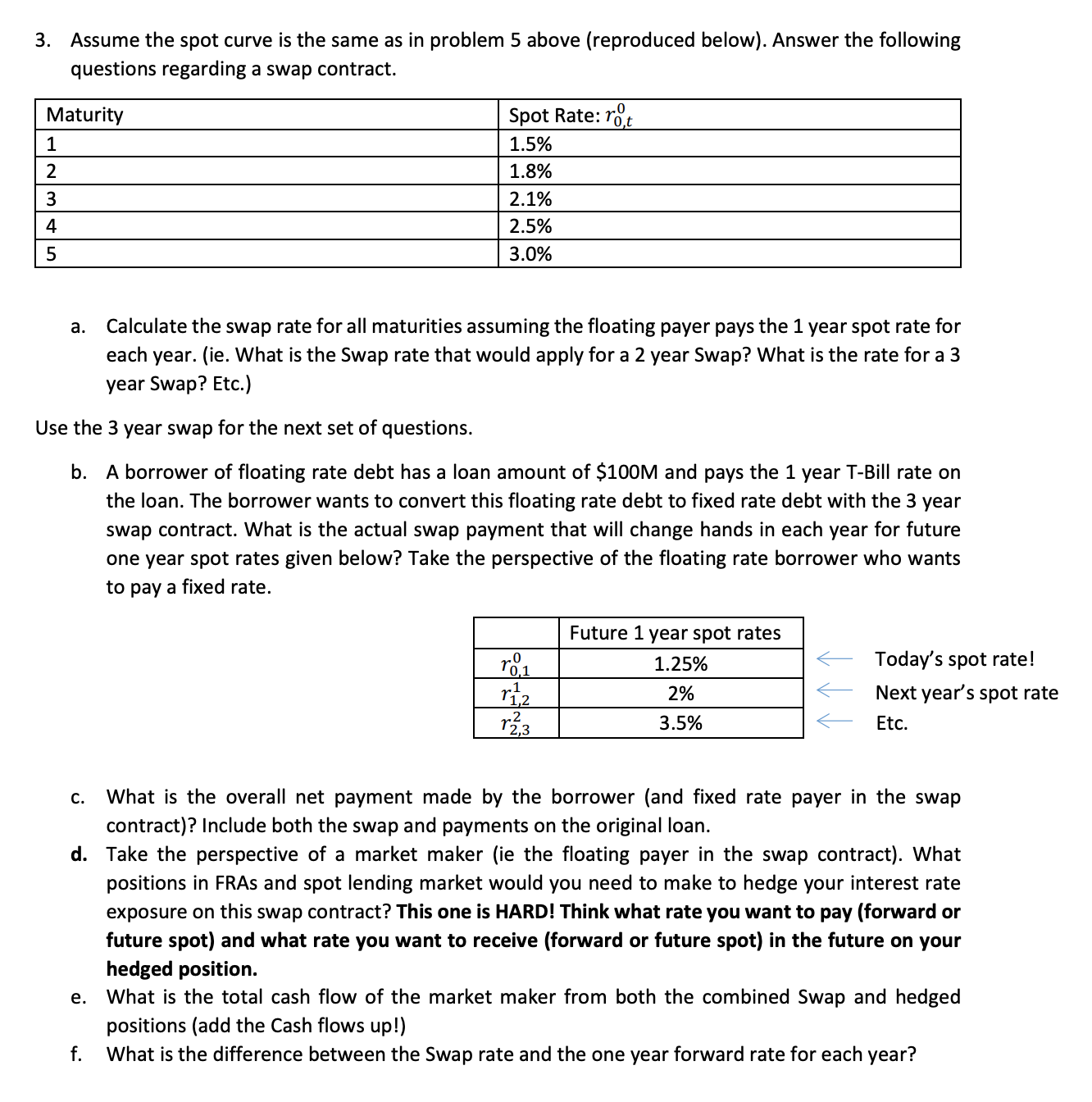

1. Consider two zero coupon bonds with both with $100 face value and the following additional characteristics: Bond A B Maturity 3 7 Yield 3% 5% a. How many of bond A do you need to long (or short sell) for each of bond B that you buy (or short sell) to create a fully immunized ($ Duration) portfolio to speculate on the yield curve flattening? Indicate a short sale with a negative sign and round to 3 decimal places. b. What is the value of the fully immunized ($ Duration) portfolio that you would create to speculate on short-term rates increasing relative to longer term rates? C. What is the value of your portfolio from above if the rate on the longer maturity bond falls to 3% (ie the yield curve flattens)? Round your answer to the nearest cent. d. Did you make or lose money on your strategy when the yield curve flattened? 2. Assume you have already calculated the spot rate curve given below: Maturity 1 2 3 45 Spot Rate: rot 1.5% 1.8% 2.1% 2.5% 3.0% a. What are the one year forward rates implied by this spot curve (ie r,2, r2,3, r3,4, and r4,5)? b. What are the two year forward rates implied by this spot curve (ie r1,3, r2,4, and r3,5)? C. What trades in zero coupon bonds with the yields from the table would you need to make today in order to commit to effectively "lend" money between 1 year from now and 3 years from now at the rate r,3? d. What zero coupon bond would you want to buy today if you were speculating that the spot rate curve would remain static during the next year? 3. Assume the spot curve is the same as in problem 5 above (reproduced below). Answer the following questions regarding a swap contract. Maturity 1 2 3 4 5 Spot Rate: rot .0 1.5% 1.8% 2.1% 2.5% 3.0% a. Calculate the swap rate for all maturities assuming the floating payer pays the 1 year spot rate for each year. (ie. What is the Swap rate that would apply for a 2 year Swap? What is the rate for a 3 year Swap? Etc.) Use the 3 year swap for the next set of questions. b. A borrower of floating rate debt has a loan amount of $100M and pays the 1 year T-Bill rate on the loan. The borrower wants to convert this floating rate debt to fixed rate debt with the 3 year swap contract. What is the actual swap payment that will change hands in each year for future one year spot rates given below? Take the perspective of the floating rate borrower who wants to pay a fixed rate. Future 1 year spot rates .0 r01 1 1,2 2 1.25% 2% 12,3 3.5% Today's spot rate! Next year's spot rate Etc. C. What is the overall net payment made by the borrower (and fixed rate payer in the swap contract)? Include both the swap and payments on the original loan. d. Take the perspective of a market maker (ie the floating payer in the swap contract). What positions in FRAS and spot lending market would you need to make to hedge your interest rate exposure on this swap contract? This one is HARD! Think what rate you want to pay (forward or future spot) and what rate you want to receive (forward or future spot) in the future on your hedged position. e. f. What is the total cash flow of the market maker from both the combined Swap and hedged positions (add the Cash flows up!) What is the difference between the Swap rate and the one year forward rate for each year? 1. Consider two zero coupon bonds with both with $100 face value and the following additional characteristics: Bond A B Maturity 3 7 Yield 3% 5% a. How many of bond A do you need to long (or short sell) for each of bond B that you buy (or short sell) to create a fully immunized ($ Duration) portfolio to speculate on the yield curve flattening? Indicate a short sale with a negative sign and round to 3 decimal places. b. What is the value of the fully immunized ($ Duration) portfolio that you would create to speculate on short-term rates increasing relative to longer term rates? C. What is the value of your portfolio from above if the rate on the longer maturity bond falls to 3% (ie the yield curve flattens)? Round your answer to the nearest cent. d. Did you make or lose money on your strategy when the yield curve flattened? 2. Assume you have already calculated the spot rate curve given below: Maturity 1 2 3 45 Spot Rate: rot 1.5% 1.8% 2.1% 2.5% 3.0% a. What are the one year forward rates implied by this spot curve (ie r,2, r2,3, r3,4, and r4,5)? b. What are the two year forward rates implied by this spot curve (ie r1,3, r2,4, and r3,5)? C. What trades in zero coupon bonds with the yields from the table would you need to make today in order to commit to effectively "lend" money between 1 year from now and 3 years from now at the rate r,3? d. What zero coupon bond would you want to buy today if you were speculating that the spot rate curve would remain static during the next year? 3. Assume the spot curve is the same as in problem 5 above (reproduced below). Answer the following questions regarding a swap contract. Maturity 1 2 3 4 5 Spot Rate: rot .0 1.5% 1.8% 2.1% 2.5% 3.0% a. Calculate the swap rate for all maturities assuming the floating payer pays the 1 year spot rate for each year. (ie. What is the Swap rate that would apply for a 2 year Swap? What is the rate for a 3 year Swap? Etc.) Use the 3 year swap for the next set of questions. b. A borrower of floating rate debt has a loan amount of $100M and pays the 1 year T-Bill rate on the loan. The borrower wants to convert this floating rate debt to fixed rate debt with the 3 year swap contract. What is the actual swap payment that will change hands in each year for future one year spot rates given below? Take the perspective of the floating rate borrower who wants to pay a fixed rate. Future 1 year spot rates .0 r01 1 1,2 2 1.25% 2% 12,3 3.5% Today's spot rate! Next year's spot rate Etc. C. What is the overall net payment made by the borrower (and fixed rate payer in the swap contract)? Include both the swap and payments on the original loan. d. Take the perspective of a market maker (ie the floating payer in the swap contract). What positions in FRAS and spot lending market would you need to make to hedge your interest rate exposure on this swap contract? This one is HARD! Think what rate you want to pay (forward or future spot) and what rate you want to receive (forward or future spot) in the future on your hedged position. e. f. What is the total cash flow of the market maker from both the combined Swap and hedged positions (add the Cash flows up!) What is the difference between the Swap rate and the one year forward rate for each year?

Expert Answer:

Posted Date:

Students also viewed these finance questions

-

Conduct online research for federal income tax brackets for the current year. Which tax bracket do you fit into for your gross household income? How close is your gross household income to the next...

-

Palomar Paper Products purchased land in 1996 for $15,000 cash. The company has held the land since that time. In 2014 Palomar purchased another tract of land for $15,000 cash. Assume that prices in...

-

Suppose you are conducting market research for your favorite soda brand. Sales have been lagging for two quarters, and you are determined to find out why. You decide to host an in-person focus group...

-

You are in charge of the audit of the United Widget Workers of America, a labor union that your firm has been auditing for several years. In performing the audit for the year ended June 30, 198X, you...

-

Included in the December 31 trial balance of Rivera Company are the following assets. Cash $ 190,000 Work in process $200,000 Equipment (net) 1,100,000 Receivables (net) 400,000 Prepaid insurance...

-

A variable is normally distributed with mean 12 and standard deviation 3. a. Determine the quartiles of the variable. b. Obtain and interpret the 90th percentile. c. Find the value that 65% of all...

-

Three-year term insurance issued for a three-year term insurance; see death guarantee, (k + 1). will be paid at the end of the year. death probabilities It is given as. Find the net annual premium of...

-

Find an Income Statement, Balance Sheet and Statement of Cash Flows for a company in which you re interested. ( All three do not have to be from the same company ) . You will need to provide me with...

-

The following is an incorrect proof of For every natural number n 1, in every group of n cars, all the cars are from the same state Proof by induction: Base case: In a group of 1 car, every car...

-

1. A note made on January 4 and due in 90 days would mature on what date? (assume February has 28 days) a. April 2 c. April 4 b. April 3 d. April 5 2. The maturity value of a $5,000, 60-day, 6...

-

Dove Corporation began its operations on September 1 of the current year. Budgeted sales for the first three months of business are $240,000, $311,000, and $410,000, respectively, for September,...

-

Julian Thomas, who is single, goes to graduate school part-time and works as a waiter at the Bay Grill in San Francisco. During 2018, his gross income was $20,700 in wages and tips. He has decided to...

-

dual has one unit of time which she splits between work and leisure. When she works, her wage rate is 1 per unit of time, and she has no other sources of income.

-

Revol Industries manufactures plastic bottles for the food industry. On average, Revol pays $76 per ton for its plastics. Revol's waste-disposal company has increased its waste-disposal charge to $57...

Study smarter with the SolutionInn App