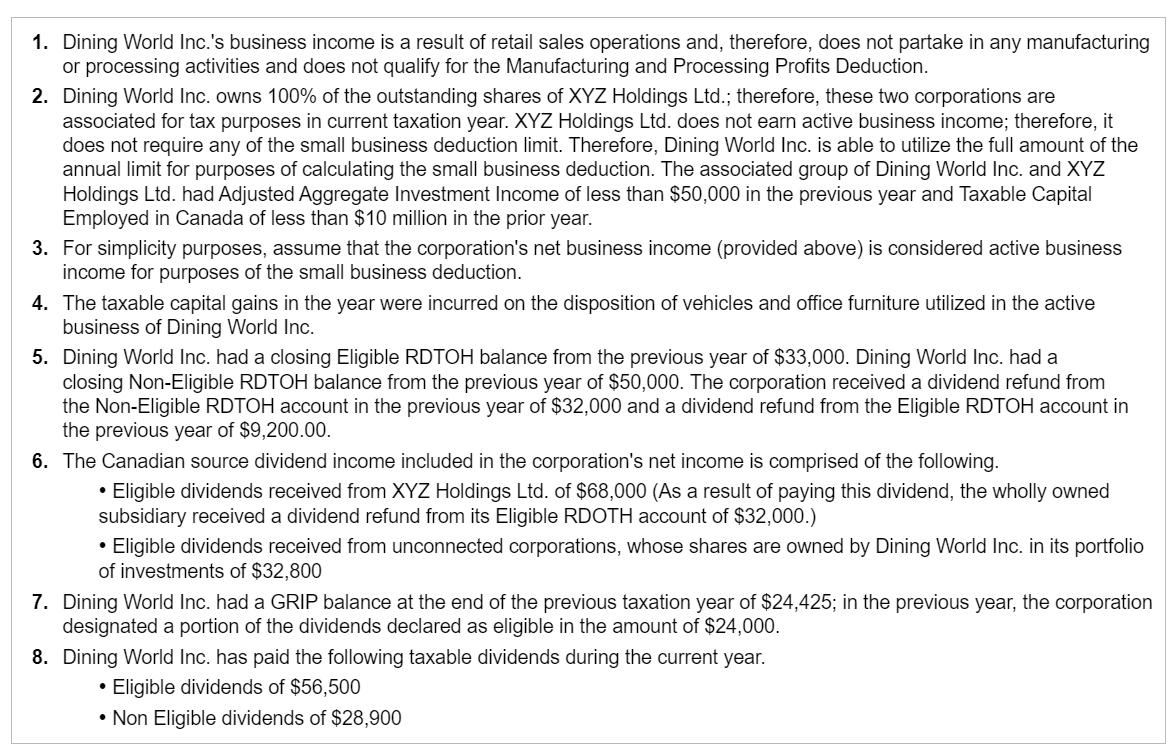

1. Dining World Inc.'s business income is a result of retail sales operations and, therefore, does...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

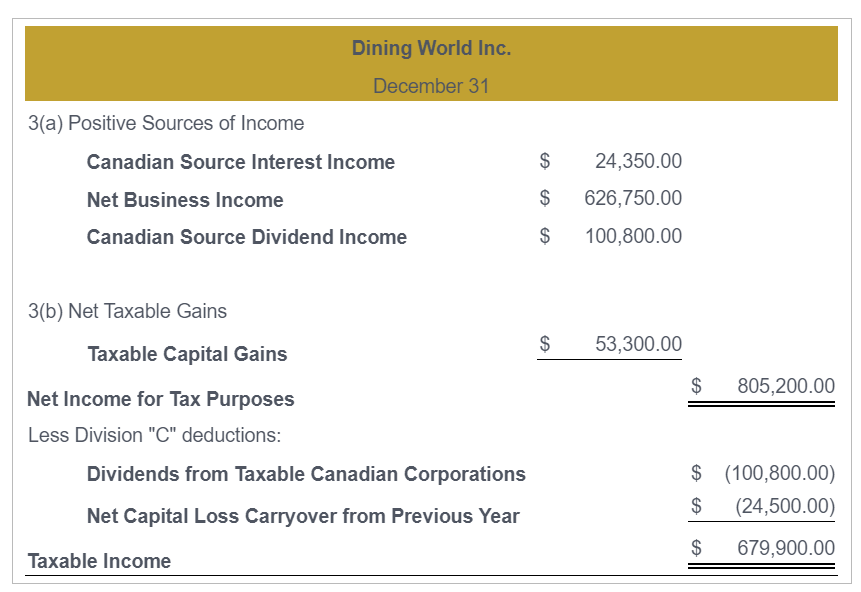

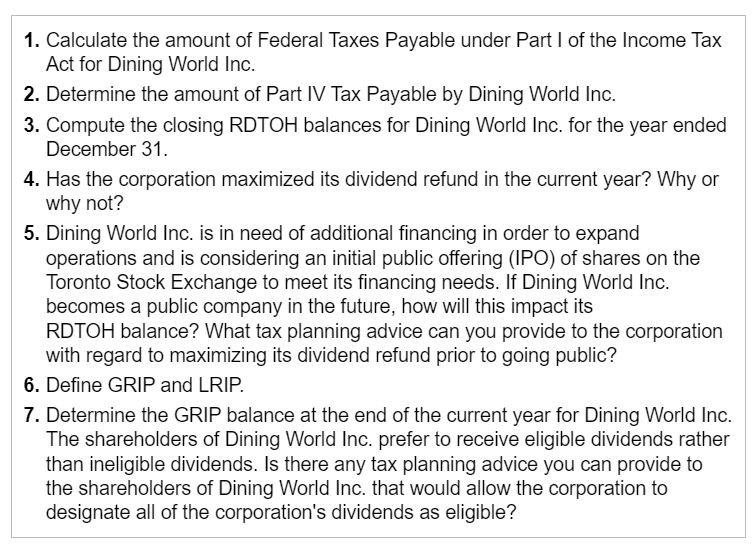

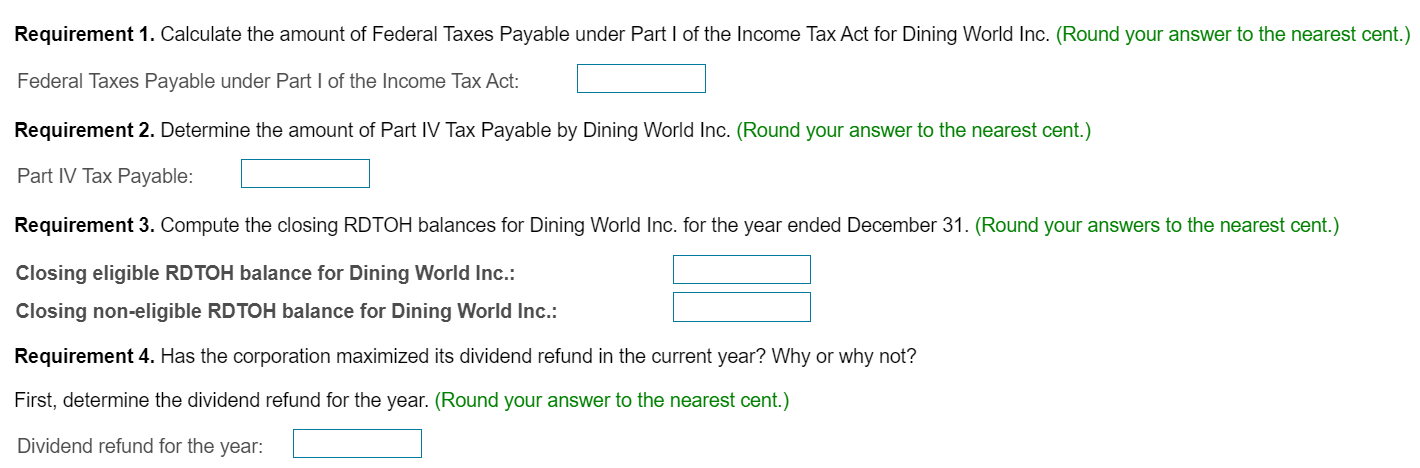

1. Dining World Inc.'s business income is a result of retail sales operations and, therefore, does not partake in any manufacturing or processing activities and does not qualify for the Manufacturing and Processing Profits Deduction. 2. Dining World Inc. owns 100% of the outstanding shares of XYZ Holdings Ltd.; therefore, these two corporations are associated for tax purposes in current taxation year. XYZ Holdings Ltd. does not earn active business income; therefore, it does not require any of the small business deduction limit. Therefore, Dining World Inc. is able to utilize the full amount of the annual limit for purposes of calculating the small business deduction. The associated group of Dining World Inc. and XYZ Holdings Ltd. had Adjusted Aggregate Investment Income of less than $50,000 in the previous year and Taxable Capital Employed in Canada of less than $10 million in the prior year. 3. For simplicity purposes, assume that the corporation's net business income (provided above) is considered active business income for purposes of the small business deduction. 4. The taxable capital gains in the year were incurred on the disposition of vehicles and office furniture utilized in the active business of Dining World Inc. 5. Dining World Inc. had a closing Eligible RDTOH balance from the previous year of $33,000. Dining World Inc. had a closing Non-Eligible RDTOH balance from the previous year of $50,000. The corporation received a dividend refund from the Non-Eligible RDTOH account in the previous year of $32,000 and a dividend refund from the Eligible RDTOH account in the previous year of $9,200.00. 6. The Canadian source dividend income included in the corporation's net income is comprised of the following. • Eligible dividends received from XYZ Holdings Ltd. of $68,000 (As a result of paying this dividend, the wholly owned subsidiary received a dividend refund from its Eligible RDOTH account of $32,000.) • Eligible dividends received from unconnected corporations, whose shares are owned by Dining World Inc. in its portfolio of investments of $32,800 7. Dining World Inc. had a GRIP balance at the end of the previous taxation year of $24,425; in the previous year, the corporation designated a portion of the dividends declared as eligible in the amount of $24,000. 8. Dining World Inc. has paid the following taxable dividends during the current year. . Eligible dividends of $56,500 • Non Eligible dividends of $28,900 Dining World Inc. December 31 3(a) Positive Sources of Income Canadian Source Interest Income Net Business Income $ 24,350.00 $ 626,750.00 Canadian Source Dividend Income $ 100,800.00 3(b) Net Taxable Gains Taxable Capital Gains Net Income for Tax Purposes $ 53,300.00 $ 805,200.00 Less Division "C" deductions: Dividends from Taxable Canadian Corporations $ (100,800.00) $ (24,500.00) Net Capital Loss Carryover from Previous Year Taxable Income $ 679,900.00 1. Calculate the amount of Federal Taxes Payable under Part I of the Income Tax Act for Dining World Inc. 2. Determine the amount of Part IV Tax Payable by Dining World Inc. 3. Compute the closing RDTOH balances for Dining World Inc. for the year ended December 31. 4. Has the corporation maximized its dividend refund in the current year? Why or why not? 5. Dining World Inc. is in need of additional financing in order to expand operations and is considering an initial public offering (IPO) of shares on the Toronto Stock Exchange to meet its financing needs. If Dining World Inc. becomes a public company in the future, how will this impact its RDTOH balance? What tax planning advice can you provide to the corporation with regard to maximizing its dividend refund prior to going public? 6. Define GRIP and LRIP. 7. Determine the GRIP balance at the end of the current year for Dining World Inc. The shareholders of Dining World Inc. prefer to receive eligible dividends rather than ineligible dividends. Is there any tax planning advice you can provide to the shareholders of Dining World Inc. that would allow the corporation to designate all of the corporation's dividends as eligible? Dining World Inc. is a Canadian controlled private corporation (CCPC) that operates a retail business selling cooking utensils, knives, and small appliances for both professional chefs and home cooks. Dining World Inc. is operated out of Ottawa, Ontario, and all of the corporation's revenue and expenses are incurred in Ontario. Requirement 1. Calculate the amount of Federal Taxes Payable under Part I of the Income Tax Act for Dining World Inc. (Round your answer to the nearest cent.) Federal Taxes Payable under Part I of the Income Tax Act: Requirement 2. Determine the amount of Part IV Tax Payable by Dining World Inc. (Round your answer to the nearest cent.) Part IV Tax Payable: Requirement 3. Compute the closing RDTOH balances for Dining World Inc. for the year ended December 31. (Round your answers to the nearest cent.) Closing eligible RDTOH balance for Dining World Inc.: Closing non-eligible RDTOH balance for Dining World Inc.: Requirement 4. Has the corporation maximized its dividend refund in the current year? Why or why not? First, determine the dividend refund for the year. (Round your answer to the nearest cent.) Dividend refund for the year: Requirement 7. Determine the GRIP balance at the end of the current year for Dining World Inc. The shareholders of Dining World Inc. prefer to receive eligible dividends rather than ineligible dividends. Is there any tax planning advice you can provide to the shareholders of Dining World Inc. that would allow the corporation to designate all of the corporation's dividends as eligible? GRIP balance at the end of the current year: 1. Dining World Inc.'s business income is a result of retail sales operations and, therefore, does not partake in any manufacturing or processing activities and does not qualify for the Manufacturing and Processing Profits Deduction. 2. Dining World Inc. owns 100% of the outstanding shares of XYZ Holdings Ltd.; therefore, these two corporations are associated for tax purposes in current taxation year. XYZ Holdings Ltd. does not earn active business income; therefore, it does not require any of the small business deduction limit. Therefore, Dining World Inc. is able to utilize the full amount of the annual limit for purposes of calculating the small business deduction. The associated group of Dining World Inc. and XYZ Holdings Ltd. had Adjusted Aggregate Investment Income of less than $50,000 in the previous year and Taxable Capital Employed in Canada of less than $10 million in the prior year. 3. For simplicity purposes, assume that the corporation's net business income (provided above) is considered active business income for purposes of the small business deduction. 4. The taxable capital gains in the year were incurred on the disposition of vehicles and office furniture utilized in the active business of Dining World Inc. 5. Dining World Inc. had a closing Eligible RDTOH balance from the previous year of $33,000. Dining World Inc. had a closing Non-Eligible RDTOH balance from the previous year of $50,000. The corporation received a dividend refund from the Non-Eligible RDTOH account in the previous year of $32,000 and a dividend refund from the Eligible RDTOH account in the previous year of $9,200.00. 6. The Canadian source dividend income included in the corporation's net income is comprised of the following. • Eligible dividends received from XYZ Holdings Ltd. of $68,000 (As a result of paying this dividend, the wholly owned subsidiary received a dividend refund from its Eligible RDOTH account of $32,000.) • Eligible dividends received from unconnected corporations, whose shares are owned by Dining World Inc. in its portfolio of investments of $32,800 7. Dining World Inc. had a GRIP balance at the end of the previous taxation year of $24,425; in the previous year, the corporation designated a portion of the dividends declared as eligible in the amount of $24,000. 8. Dining World Inc. has paid the following taxable dividends during the current year. . Eligible dividends of $56,500 • Non Eligible dividends of $28,900 Dining World Inc. December 31 3(a) Positive Sources of Income Canadian Source Interest Income Net Business Income $ 24,350.00 $ 626,750.00 Canadian Source Dividend Income $ 100,800.00 3(b) Net Taxable Gains Taxable Capital Gains Net Income for Tax Purposes $ 53,300.00 $ 805,200.00 Less Division "C" deductions: Dividends from Taxable Canadian Corporations $ (100,800.00) $ (24,500.00) Net Capital Loss Carryover from Previous Year Taxable Income $ 679,900.00 1. Calculate the amount of Federal Taxes Payable under Part I of the Income Tax Act for Dining World Inc. 2. Determine the amount of Part IV Tax Payable by Dining World Inc. 3. Compute the closing RDTOH balances for Dining World Inc. for the year ended December 31. 4. Has the corporation maximized its dividend refund in the current year? Why or why not? 5. Dining World Inc. is in need of additional financing in order to expand operations and is considering an initial public offering (IPO) of shares on the Toronto Stock Exchange to meet its financing needs. If Dining World Inc. becomes a public company in the future, how will this impact its RDTOH balance? What tax planning advice can you provide to the corporation with regard to maximizing its dividend refund prior to going public? 6. Define GRIP and LRIP. 7. Determine the GRIP balance at the end of the current year for Dining World Inc. The shareholders of Dining World Inc. prefer to receive eligible dividends rather than ineligible dividends. Is there any tax planning advice you can provide to the shareholders of Dining World Inc. that would allow the corporation to designate all of the corporation's dividends as eligible? Dining World Inc. is a Canadian controlled private corporation (CCPC) that operates a retail business selling cooking utensils, knives, and small appliances for both professional chefs and home cooks. Dining World Inc. is operated out of Ottawa, Ontario, and all of the corporation's revenue and expenses are incurred in Ontario. Requirement 1. Calculate the amount of Federal Taxes Payable under Part I of the Income Tax Act for Dining World Inc. (Round your answer to the nearest cent.) Federal Taxes Payable under Part I of the Income Tax Act: Requirement 2. Determine the amount of Part IV Tax Payable by Dining World Inc. (Round your answer to the nearest cent.) Part IV Tax Payable: Requirement 3. Compute the closing RDTOH balances for Dining World Inc. for the year ended December 31. (Round your answers to the nearest cent.) Closing eligible RDTOH balance for Dining World Inc.: Closing non-eligible RDTOH balance for Dining World Inc.: Requirement 4. Has the corporation maximized its dividend refund in the current year? Why or why not? First, determine the dividend refund for the year. (Round your answer to the nearest cent.) Dividend refund for the year: Requirement 7. Determine the GRIP balance at the end of the current year for Dining World Inc. The shareholders of Dining World Inc. prefer to receive eligible dividends rather than ineligible dividends. Is there any tax planning advice you can provide to the shareholders of Dining World Inc. that would allow the corporation to designate all of the corporation's dividends as eligible? GRIP balance at the end of the current year:

Expert Answer:

Answer rating: 100% (QA)

1 Calculate the amount of Federal Taxes Payable under Part I of the Income Tax Act for Dining World Inc Round your answer to the nearest cent Part I tax calculation First 500000 of active business inc... View the full answer

Related Book For

International Marketing And Export Management

ISBN: 9781292016924

8th Edition

Authors: Gerald Albaum , Alexander Josiassen , Edwin Duerr

Posted Date:

Students also viewed these accounting questions

-

Kitchen World Inc. is a Canadian controlled private corporation (CCPC) that operates a retail business selling cooking utensils, knives and small appliances for both professional chefs and home...

-

Required a. Use professional judgment in deciding on the preliminary judgment about materiality for earnings, current assets, current liabilities, and total assets. Your conclusions should be stated...

-

An average of three small businesses go bankrupt each month. What is the probability that five small businesses will go bankrupt in a certain month?

-

The Town of Thomaston has a Solid Waste Landfill Enterprise Fund with the following trial balance as of January 1, 2017, the first day of the fiscal year. During the year, the following transactions...

-

Problem 3. A human head can be modeled as 15cm diameter sphere, with the sculp covering approximately 25%. On average adults have 100,000 scalp hairs. a) What is the density of hairs, measured as...

-

The table shows the mean heights and standard deviations for a population of men and a population of women. Compare the z-scores for a 6-foot-tall man and a 6-foot-tall woman. Assume the...

-

An investor purchased the following 5 bonds. Each bond had a par value of $1,000 and an 8% yield to maturity on the purchase day. Immediately after the investor purchased them, interest rates fell...

-

WATER SUPPLY PLANNING AND DEVELOPMENT QUESTION: EXPLAIN AND EXPOUND THE TOPICS MENTIONED BELOW. PROVIDE EXAMPLES. TOPICS: >Importance of safe drinking water on public health. >Development of water...

-

Questions specifically related to annuities: 1. What is an annuity and how does it work? 2. What are the key components of an annuity contract? 3. How do you calculate the future value of an ordinary...

-

Tio Tom's Dive Shop has 6 employees who each make $12,500 for the first quarter. Total quarterly federal income tax withheld from wages = $6,900. What should line 6 be on the first quarter Form 941...

-

Assume that you arrange a mortgage loan of $100,000 at j2 15% (i.e. 15% nominal annual rate compounded semi-annually) amortized over 25 years with monthly payments and a 5 year term. You are...

-

You are considering an acquisition of a property that, upon stabilization, will be worth an estimated $4,500,000. The costs to stabilize the property total $975,000, which would all be incurred...

-

Locate the Notes to the Financial Statements. Determine if your companies have a note providing information about the business segments in which the company operates. Often, companies label this note...

-

College friends go out for drinks to celebrate someone's 21st birthday. One woman in the group, who is not of legal age, uses a fake ID and gets arrested. What term explains the difference in what...

-

Write an Environmental Analysis (Marketing Plan) to re-position an existing offering (marketing to first time tax-payers) made by a real company. It needs to be comprehensive and written for a...

-

Using the information in P11-2B, compute the overhead controllable variance and the overhead volume variance. Data From Problem 11-2B: Huang Company uses a standard cost accounting system to account...

-

Government regulations can affect the viability and effectiveness of a company using the Internet as a foreign market entry mode. Contrast the government regulations governing e-commerce in the...

-

Primex Marketing, Inc., formed in 1982, is an international niche marketer of Roleez wheels and a limited line of products using the wheels. The patented wheels use very low pressure, soft, wide, and...

-

In the decade of the 2010s, the plans and operations of Avon Inc. in marketing, research, and manufacturing throughout Asia are still being affected by actions taken after a 1998 meeting. The US...

-

At 30 June 2024, the accountant for Woodbine Construction, Mary Ellam, is preparing the financial statements for the year ended on that date. To calculate the annual leave payable, the accountant had...

-

How would each of the following liabilities be classified (current, non-current, or both) at the end of the financial year? Unearned revenue Accrued expenses Provision for warranty repair costs...

-

The following were among transactions of Everluck Enterprises Ltd during the financial years ending 30 June 2023 and 30 June 2024. Required Record in general journal form all the above transactions,...

Study smarter with the SolutionInn App