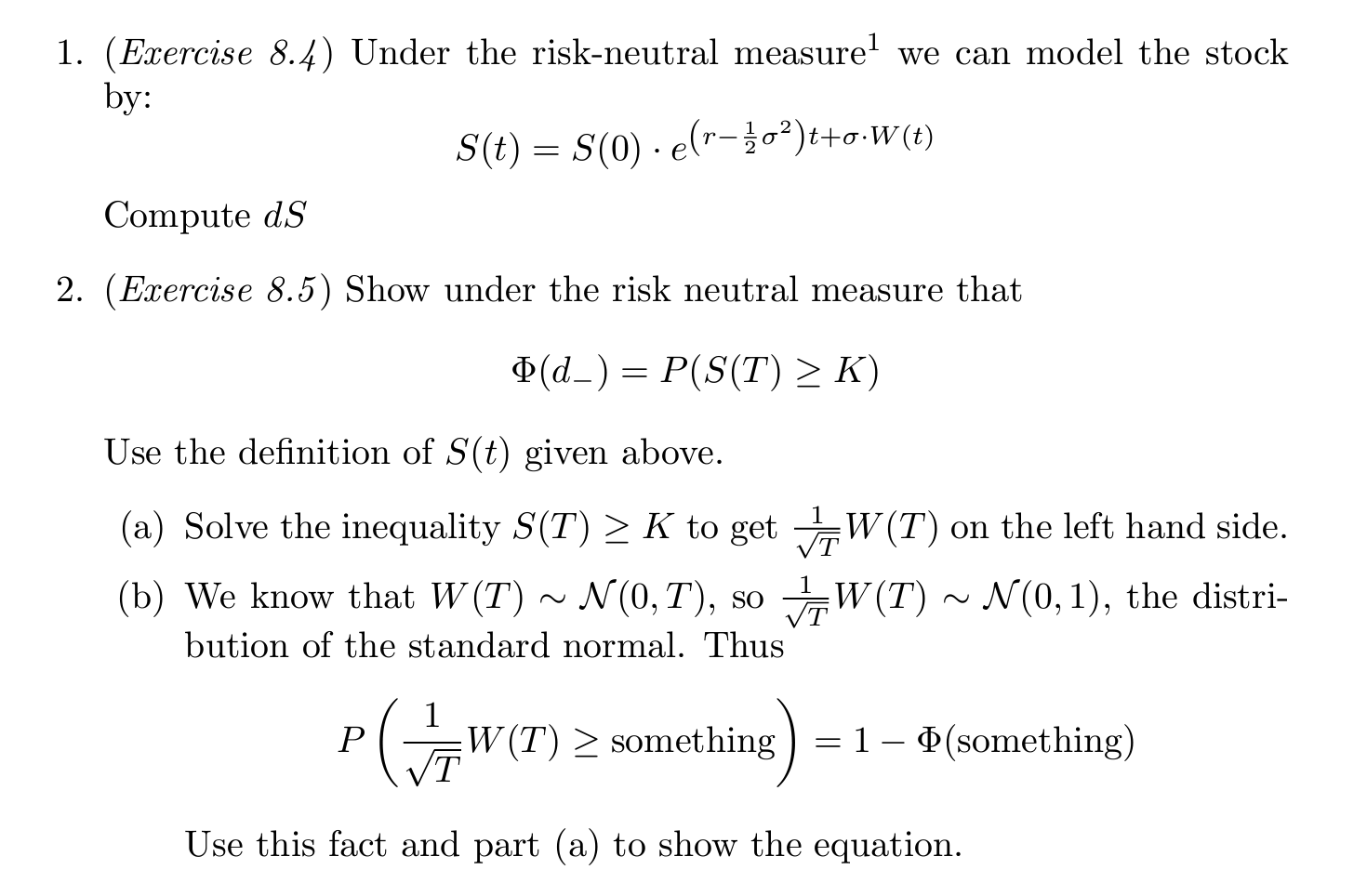

1. (Exercise 8.4) Under the risk-neutral measure we can model the stock by: S(t) = S(0)...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

Related Book For

Posted Date: