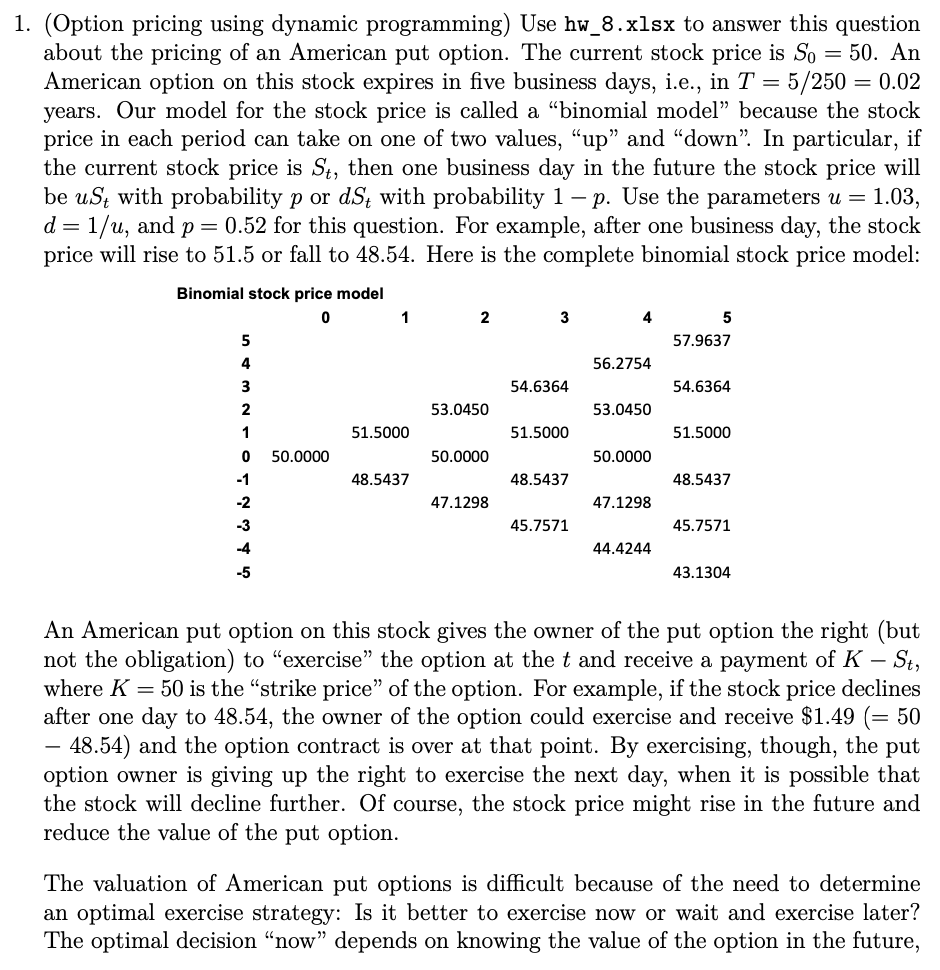

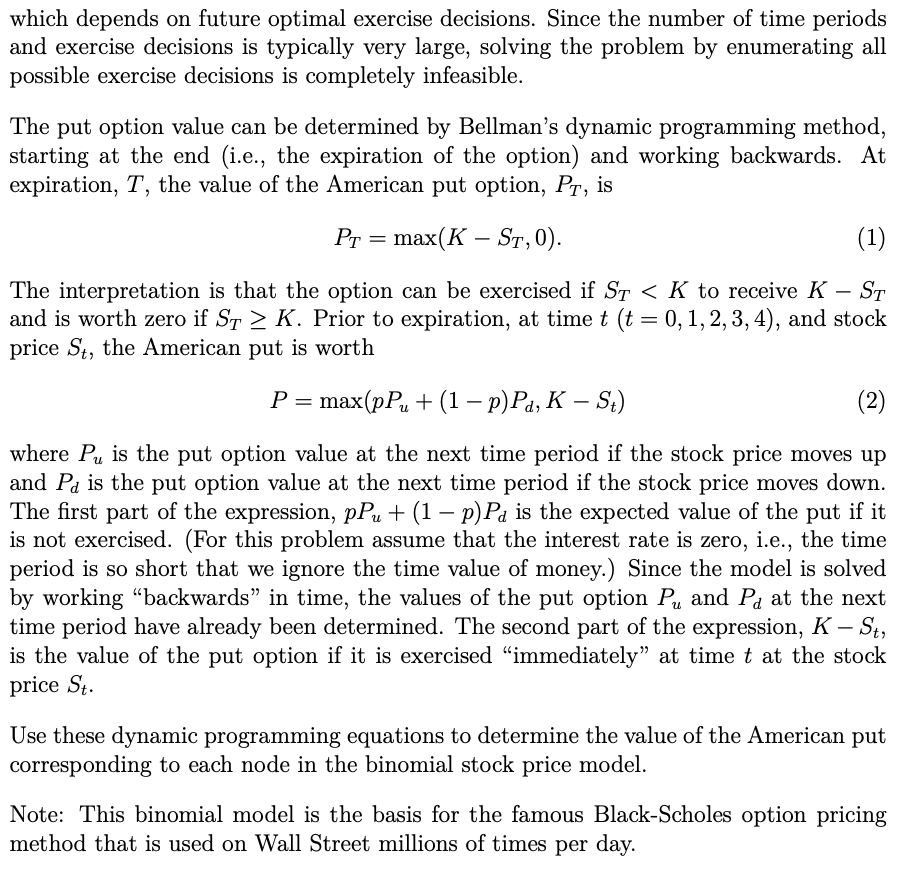

1. (Option pricing using dynamic programming) Use hw_8.xlsx to answer this question about the pricing of...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

1. (Option pricing using dynamic programming) Use hw_8.xlsx to answer this question about the pricing of an American put option. The current stock price is So = 50. An American option on this stock expires in five business days, i.e., in T = 5/250 = 0.02 years. Our model for the stock price is called a "binomial model because the stock price in each period can take on one of two values, "up" and "down". In particular, if the current stock price is St, then one business day in the future the stock price will be ust with probability p or dS with probability 1 - p. Use the parameters u = 1.03, d = 1/u, and p = 0.52 for this question. For example, after one business day, the stock price will rise to 51.5 or fall to 48.54. Here is the complete binomial stock price model: Binomial stock price model 0 5 4 1 2 3 4 5 57.9637 56.2754 3 54.6364 54.6364 2 53.0450 53.0450 1 51.5000 51.5000 51.5000 0 50.0000 50.0000 50.0000 -1 48.5437 48.5437 48.5437 -2 47.1298 47.1298 -3 45.7571 45.7571 -4 44.4244 -5 43.1304 An American put option on this stock gives the owner of the put option the right (but not the obligation) to "exercise" the option at the t and receive a payment of K - St, where K = 50 is the "strike price" of the option. For example, if the stock price declines after one day to 48.54, the owner of the option could exercise and receive $1.49 (= 50 - 48.54) and the option contract is over at that point. By exercising, though, the put option owner is giving up the right to exercise the next day, when it is possible that the stock will decline further. Of course, the stock price might rise in the future and reduce the value of the put option. The valuation of American put options is difficult because of the need to determine an optimal exercise strategy: Is it better to exercise now or wait and exercise later? The optimal decision "now" depends on knowing the value of the option in the future, which depends on future optimal exercise decisions. Since the number of time periods and exercise decisions is typically very large, solving the problem by enumerating all possible exercise decisions is completely infeasible. The put option value can be determined by Bellman's dynamic programming method, starting at the end (i.e., the expiration of the option) and working backwards. At expiration, T, the value of the American put option, PT, is PT = max(K-ST, 0). - (1) ST The interpretation is that the option can be exercised if ST < K to receive K and is worth zero if ST > K. Prior to expiration, at time t (t = 0, 1, 2, 3, 4), and stock price St, the American put is worth - P = max(pP + (1 p)Pa, K St) - (2) where Pu is the put option value at the next time period if the stock price moves up and Pd is the put option value at the next time period if the stock price moves down. The first part of the expression, pPu + (1 p)P is the expected value of the put if it is not exercised. (For this problem assume that the interest rate is zero, i.e., the time period is so short that we ignore the time value of money.) Since the model is solved by working "backwards" in time, the values of the put option Pu and Pd at the next time period have already been determined. The second part of the expression, K St, is the value of the put option if it is exercised "immediately" at time t at the stock price St. - Use these dynamic programming equations to determine the value of the American put corresponding to each node in the binomial stock price model. Note: This binomial model is the basis for the famous Black-Scholes option pricing method that is used on Wall Street millions of times per day. 1. (Option pricing using dynamic programming) Use hw_8.xlsx to answer this question about the pricing of an American put option. The current stock price is So = 50. An American option on this stock expires in five business days, i.e., in T = 5/250 = 0.02 years. Our model for the stock price is called a "binomial model because the stock price in each period can take on one of two values, "up" and "down". In particular, if the current stock price is St, then one business day in the future the stock price will be ust with probability p or dS with probability 1 - p. Use the parameters u = 1.03, d = 1/u, and p = 0.52 for this question. For example, after one business day, the stock price will rise to 51.5 or fall to 48.54. Here is the complete binomial stock price model: Binomial stock price model 0 5 4 1 2 3 4 5 57.9637 56.2754 3 54.6364 54.6364 2 53.0450 53.0450 1 51.5000 51.5000 51.5000 0 50.0000 50.0000 50.0000 -1 48.5437 48.5437 48.5437 -2 47.1298 47.1298 -3 45.7571 45.7571 -4 44.4244 -5 43.1304 An American put option on this stock gives the owner of the put option the right (but not the obligation) to "exercise" the option at the t and receive a payment of K - St, where K = 50 is the "strike price" of the option. For example, if the stock price declines after one day to 48.54, the owner of the option could exercise and receive $1.49 (= 50 - 48.54) and the option contract is over at that point. By exercising, though, the put option owner is giving up the right to exercise the next day, when it is possible that the stock will decline further. Of course, the stock price might rise in the future and reduce the value of the put option. The valuation of American put options is difficult because of the need to determine an optimal exercise strategy: Is it better to exercise now or wait and exercise later? The optimal decision "now" depends on knowing the value of the option in the future, which depends on future optimal exercise decisions. Since the number of time periods and exercise decisions is typically very large, solving the problem by enumerating all possible exercise decisions is completely infeasible. The put option value can be determined by Bellman's dynamic programming method, starting at the end (i.e., the expiration of the option) and working backwards. At expiration, T, the value of the American put option, PT, is PT = max(K-ST, 0). - (1) ST The interpretation is that the option can be exercised if ST < K to receive K and is worth zero if ST > K. Prior to expiration, at time t (t = 0, 1, 2, 3, 4), and stock price St, the American put is worth - P = max(pP + (1 p)Pa, K St) - (2) where Pu is the put option value at the next time period if the stock price moves up and Pd is the put option value at the next time period if the stock price moves down. The first part of the expression, pPu + (1 p)P is the expected value of the put if it is not exercised. (For this problem assume that the interest rate is zero, i.e., the time period is so short that we ignore the time value of money.) Since the model is solved by working "backwards" in time, the values of the put option Pu and Pd at the next time period have already been determined. The second part of the expression, K St, is the value of the put option if it is exercised "immediately" at time t at the stock price St. - Use these dynamic programming equations to determine the value of the American put corresponding to each node in the binomial stock price model. Note: This binomial model is the basis for the famous Black-Scholes option pricing method that is used on Wall Street millions of times per day.

Expert Answer:

Related Book For

Posted Date:

Students also viewed these finance questions

-

13. What is a lower bound for the price of 3-month call option on a non- dividend-paying stock when the stock price is $50, the strike price is $45, and the 3-month risk-free interest rate is 8%?...

-

CANMNMM January of this year. (a) Each item will be held in a record. Describe all the data structures that must refer to these records to implement the required functionality. Describe all the...

-

Q3: Prove: For any sets A and B, Ax B = B A ?

-

Consider a two-stage cascade refrigeration system operating between -60oC and 50oC. Each stage operates on an ideal vapor-compression refrigeration cycle. The upper cycle uses R-134a as working...

-

You are evaluating a project with the following cash flows: initial investment is $ - 1 1 , and the expected cash flows for years 1 - 3 are $ 6 , $ 1 4 and $ 1 1 ( all cash flows are in millions of...

-

Solve Exercise 16 in Chapter 14 assuming that the annual storage cost of cut lumber is \(5 \%\) of its value. Data from Exercises 16 chapter 14 You are considering an investment in a tree farm. Trees...

-

A tank full of water has the shape of a paraboloid of revolution as shown in the figure; that is, its shape is obtained by rotating a parabola about a vertical axis. (a) If its height is 4 ft and the...

-

1. Fire Safety Management is an integral part of the organization's overall state of emergency preparedness and management. As the appointed fire salety manager. Discuss the fire safety management...

-

Let (an) be a sequence. Define the sequence In = a + a+...an. Assume that {n} is convergent. Show that {an) is convergent and find its limit.

-

It has been identified that the costs of printing paper consumption in your office have increased and the use of colour instead of black and white copying has doubled. This has therefore resulted in...

-

In the introduction to your proposal, address the following: Identify the problem you seek to address. Describe the proposed solution in a summary statement that is concise but complete. Identify the...

-

Topic for Discussion : Describe how HRD is linked to the overall goals and strategies of an organization; identify the major external and internal factors that influence employee behavior. Human...

-

What are some recent (within the past 12 months) articles, webinars, or blogs on effective Human Resource Management strategies? Identify key information for managers and why. How would one apply the...

-

My team - Director Nominated supervisor Educational leader Two room leaders 1 educator 4 trainee's Question Describe the structure of the team in your service. (e.g. Director/manager, administrative...

-

Faros Hats, Etc. has two product lines?baseball helmets and football helmets. Income statement data for the most recent year follow: Assuming fixed costs remain unchanged, and that there would be no...

-

It is possible to investigate the thermo chemical properties of hydrocarbons with molecular modeling methods. (a) Use electronic structure software to predict cHo values for the alkanes methane...

-

What would be the most effective option to increase employee motivation to stay and reduce the driver turnover rate? Why do you believe this option will be effective?

-

How else might the manager have handled the situation to prevent potential issues, including a negative impact on the teams performance?

-

This chapter discusses the use of job redesign to reduce turnover. Do you think this is feasible in this case? Why or why not? If so, how should the job be redesigned?

Study smarter with the SolutionInn App