1. The scope of IFRS 6 Exploration for and Evaluation of Mineral Resources is limited to...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

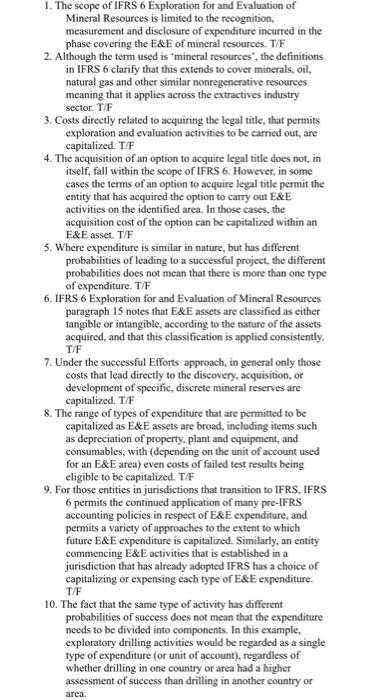

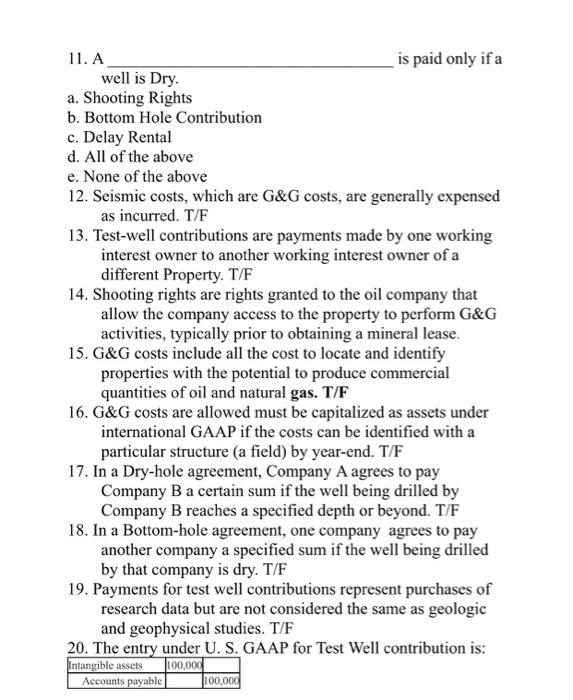

1. The scope of IFRS 6 Exploration for and Evaluation of Mineral Resources is limited to the recognition, measurement and disclosure of expenditure incurred in the phase covering the E&E of mineral resources. T/F 2. Although the term used is "mineral resources, the definitions in IFRS 6 clarify that this extends to cover minerals, oil, natural gas and other similar nonregenerative resources meaning that it applies across the extractives industry sector. T/F 3. Costs directly related to acquiring the legal title, that permits exploration and evaluation activities to be carried out, are capitalized. T/F 4. The acquisition of an option to acquire legal title does not, in itself, fall within the scope of IFRS 6. However, in some cases the terms of an option to acquire legal title permit the entity that has acquired the option to carry out E&E activities on the identified area. In those cases, the acquisition cost of the option can be capitalized within an E&E asset. T/F 5. Where expenditure is similar in nature, but has different probabilities of leading to a successful project, the different probabilities does not mean that there is more than one type of expenditure. T/F 6. IFRS 6 Exploration for and Evaluation of Mineral Resources paragraph 15 notes that E&E assets are classified as either tangible or intangible, according to the nature of the assets acquired, and that this classification is applied consistently. T/F 7. Under the successful Efforts approach, in general only those costs that lead directly to the discovery, acquisition, or development of specific, discrete mineral reserves are capitalized. T/F 8. The range of types of expenditure that are permitted to be capitalized as E&E assets are broad, including items such as depreciation of property, plant and equipment, and consumables, with (depending on the unit of account used for an E&E area) even costs of failed test results being eligible to be capitalized. T/F 9. For those entities in jurisdictions that transition to IFRS, IFRS 6 permits the continued application of many pre-IFRS accounting policies in respect of E&E expenditure, and permits a variety of approaches to the extent to which future E&E expenditure is capitalized. Similarly, an entity commencing E&E activities that is established in a jurisdiction that has already adopted IFRS has a choice of capitalizing or expensing each type of E&E expenditure. T/F 10. The fact that the same type of activity has different probabilities of success does not mean that the expenditure needs to be divided into components. In this example, exploratory drilling activities would be regarded as a single type of expenditure (or unit of account), regardless of whether drilling in one country or area had a higher assessment of success than drilling in another country or area. 11. A well is Dry. a. Shooting Rights b. Bottom Hole Contribution is paid only if a c. Delay Rental d. All of the above e. None of the above 12. Seismic costs, which are G&G costs, are generally expensed as incurred. T/F 13. Test-well contributions are payments made by one working interest owner to another working interest owner of a different Property. T/F 14. Shooting rights are rights granted to the oil company that allow the company access to the property to perform G&G activities, typically prior to obtaining a mineral lease. 15. G&G costs include all the cost to locate and identify properties with the potential to produce commercial quantities of oil and natural gas. T/F 16. G&G costs are allowed must be capitalized as assets under international GAAP if the costs can be identified with a particular structure (a field) by year-end. T/F 17. In a Dry-hole agreement, Company A agrees to pay Company B a certain sum if the well being drilled by Company B reaches a specified depth or beyond. T/F 18. In a Bottom-hole agreement, one company agrees to pay another company a specified sum if the well being drilled by that company is dry. T/F 19. Payments for test well contributions represent purchases of research data but are not considered the same as geologic and geophysical studies. T/F 20. The entry under U. S. GAAP for Test Well contribution is: Intangible assets 100,000 Accounts payable 100,000 1. The scope of IFRS 6 Exploration for and Evaluation of Mineral Resources is limited to the recognition, measurement and disclosure of expenditure incurred in the phase covering the E&E of mineral resources. T/F 2. Although the term used is "mineral resources, the definitions in IFRS 6 clarify that this extends to cover minerals, oil, natural gas and other similar nonregenerative resources meaning that it applies across the extractives industry sector. T/F 3. Costs directly related to acquiring the legal title, that permits exploration and evaluation activities to be carried out, are capitalized. T/F 4. The acquisition of an option to acquire legal title does not, in itself, fall within the scope of IFRS 6. However, in some cases the terms of an option to acquire legal title permit the entity that has acquired the option to carry out E&E activities on the identified area. In those cases, the acquisition cost of the option can be capitalized within an E&E asset. T/F 5. Where expenditure is similar in nature, but has different probabilities of leading to a successful project, the different probabilities does not mean that there is more than one type of expenditure. T/F 6. IFRS 6 Exploration for and Evaluation of Mineral Resources paragraph 15 notes that E&E assets are classified as either tangible or intangible, according to the nature of the assets acquired, and that this classification is applied consistently. T/F 7. Under the successful Efforts approach, in general only those costs that lead directly to the discovery, acquisition, or development of specific, discrete mineral reserves are capitalized. T/F 8. The range of types of expenditure that are permitted to be capitalized as E&E assets are broad, including items such as depreciation of property, plant and equipment, and consumables, with (depending on the unit of account used for an E&E area) even costs of failed test results being eligible to be capitalized. T/F 9. For those entities in jurisdictions that transition to IFRS, IFRS 6 permits the continued application of many pre-IFRS accounting policies in respect of E&E expenditure, and permits a variety of approaches to the extent to which future E&E expenditure is capitalized. Similarly, an entity commencing E&E activities that is established in a jurisdiction that has already adopted IFRS has a choice of capitalizing or expensing each type of E&E expenditure. T/F 10. The fact that the same type of activity has different probabilities of success does not mean that the expenditure needs to be divided into components. In this example, exploratory drilling activities would be regarded as a single type of expenditure (or unit of account), regardless of whether drilling in one country or area had a higher assessment of success than drilling in another country or area. 11. A well is Dry. a. Shooting Rights b. Bottom Hole Contribution is paid only if a c. Delay Rental d. All of the above e. None of the above 12. Seismic costs, which are G&G costs, are generally expensed as incurred. T/F 13. Test-well contributions are payments made by one working interest owner to another working interest owner of a different Property. T/F 14. Shooting rights are rights granted to the oil company that allow the company access to the property to perform G&G activities, typically prior to obtaining a mineral lease. 15. G&G costs include all the cost to locate and identify properties with the potential to produce commercial quantities of oil and natural gas. T/F 16. G&G costs are allowed must be capitalized as assets under international GAAP if the costs can be identified with a particular structure (a field) by year-end. T/F 17. In a Dry-hole agreement, Company A agrees to pay Company B a certain sum if the well being drilled by Company B reaches a specified depth or beyond. T/F 18. In a Bottom-hole agreement, one company agrees to pay another company a specified sum if the well being drilled by that company is dry. T/F 19. Payments for test well contributions represent purchases of research data but are not considered the same as geologic and geophysical studies. T/F 20. The entry under U. S. GAAP for Test Well contribution is: Intangible assets 100,000 Accounts payable 100,000

Expert Answer:

Answer rating: 100% (QA)

ANSWER True IFRS 6 focuses on the recognition measurement and disclosure of expenditures related to the exploration and evaluation EE phase of mineral resources True The term mineral resources in IFRS ... View the full answer

Related Book For

Posted Date:

Students also viewed these accounting questions

-

To which expenditures is the scope of IFRS 6 limited?

-

The following activities must be carried out in your chosen workplace. Typically this is the workplace in which you normally work. However, if your workplace is not suitable (for example it does not...

-

Fruits Limited signed contracts (within the scope of IFRS 15) with various customers in the current financial year. Fruits Limited entered into a contract of sale with Grape Limited for widgets worth...

-

A small company has $4,500,000 in (annual) revenue, spends 57% of its revenues on purchases, and has a net profit margin of 11.75%. They would like to increase their profits and they are looking at...

-

What are the two types of business plan? In what situation(s) would you use each type of plan?

-

The natural rate of unemployment a. The Phillips curve is Rewrite this relation as a relation between the deviation of the unemployment rate from the natural rate, inflation, and expected inflation....

-

In 2016, a father of two minor children in Cuyahoga county, Ohio, filed a claim to determine custody of the children. At the pretrial, the father informed the magistrate he wanted to be named a legal...

-

Investment Classifications For the following investments identify whether they are: 1. Trading Securities 2. Available-for-Sale Securities 3. Held-to-Maturity Securities Each case is independent of...

-

5. What effect do each of the following have on the regular payment and the total interest paid on a mortgage? Change Effect on Regular Payments (up/down) Effect on Total Interest Paid (up/down)...

-

Farmer John Industries Inc. is in the business of producing organic foods for sale to restaurants and in local markets. The company uses IFRS and has a June 30 fiscal year end. As an experiment, the...

-

Five years after the purchase of a machinery its value reduces to $4250. After eight years of use the value reduces to $2150. a) Find the linear equation that models value (V) in terms of time (t, in...

-

What two HR functions did you address and why? For example, HR function might include reduced voluntary turnover of key talent.

-

List the stages of federalism, and explain the interaction between the federal government and state governments. You should Include historical events and presidents who helped drive this development.

-

Daniel is a physiotherapist who works at Murdoch Hospital. Daniel earns $98,000 per annum from his job and has a tax credit of $18,000. Daniel's physio membership and insurance costs him $5,000 per...

-

"What are the emerging trends in bootstrapping techniques, including container-based boot loading, hypervisor-assisted bootstrapping, and cloud-initiated boot sequences, and what are their...

-

Use military time in calculating the completion time of the following IV flow problems. The doctor orders 1000 mL D10W to infuse at 100 mL / hr. The nurse starts the IV at 2030. At 2200, the IV rate...

-

The vector x is in a subspace H with a basis B = {b,b}. Find the B-coordinate vector of x. b [X]B = 1 2b -4 - 3 -5 11 1 X = - 8 - 13 29

-

A fast-food restaurant averages 150 customers per hour. The average processing time per customer is 90 seconds. a. Determine how many cash registers the restaurant should have if it wishes to...

-

Identify whether the following items are intangible assets according to the definition under IFRS: ItemIntangible asset (Yes/No) a. Cash b. Costs of research and development c. Computer software...

-

West Pacific (WP) is a financial institution incorporated in 1997 and traded on the Toronto Stock Exchange. Its performance has been exceptional since the original issue. Your firm of chartered...

-

Construction Co. started a contract in June 2011 to build a small foot bridge at a fixed price of $ 10 million. The bridge was to be completed by October 2013 at a total estimated cost of $8 million....

-

What is the difference between internal and external audiences?

-

Like most major corporations, the U.S. Census Bureau has multiple, conflicting audiences, among them the president, Congress, press, state governments, citizens (both as providers and users of data),...

-

Listed here are several things an organization might like its employees to do: 1. Write fewer emails. 2. Volunteer at a local food pantry. 3. Volunteer to recruit interns at a job fair. 4. Attend...

Study smarter with the SolutionInn App