1. You are an employee at a full-service bookkeeping and auditing firm called Accounting Solutions. Two different...

Question:

1. You are an employee at a full-service bookkeeping and auditing firm called Accounting Solutions. Two different retail operations have asked you for some help.

One of the businesses near your office is The Candy Store. The owner of The Candy Store, Mr. Taffy, stopped by your office. His bookkeeper was called out of town, and Mr. Taffy needs some transactions recorded before the month ends. There are a few purchases and sales transactions to record. The Candy Store uses a perpetual inventory.

During January the following purchase transactions occurred:

8-Jan Purchased $5,900 of merchandise from The Chocolate Shop. Terms 2/15, n/45, FOB shipping point. The Candy Store prepaid $300 in shipping and the amount was added it to their invoice.

10-Jan Purchased $350 of supplies on account from The Office Barn.Terms 2/10, n/30, FOB destination.

17-Jan A return was recorded for $1400 of the merchandise purchased on January 8 and the customer received credit.

19-Jan Paid for the supplies purchased on January 10.

22-Jan Paid the Chocolate Shop the amount due from the January 8 purchase in full

During January the following sales transactions occurred:

14-Jan Sold $950 (cost $500) of merchandise (inventory) on account to Maple Fair. Terms 3/15, n/45, FOB destination.

15-Jan Paid $75 freight charges to deliver goods to Maple Fair.

18-Jan Sold $650 (cost $350) of merchandise to cash customers.

24-Jan Maple Fair returned $175 (cost $100) of merchandise from the January 14 sale.

28-Jan Received payment in full from Maple Fair for the January 14 sale.

Adjusting entry:

31-Jan The Candy Store's inventory account shows a balance of $27,500, but the physical counts shows only $27,350 of inventory exists.

Required

Record the adjusting entry:

- Journalize the transactions

2.  Required

Required

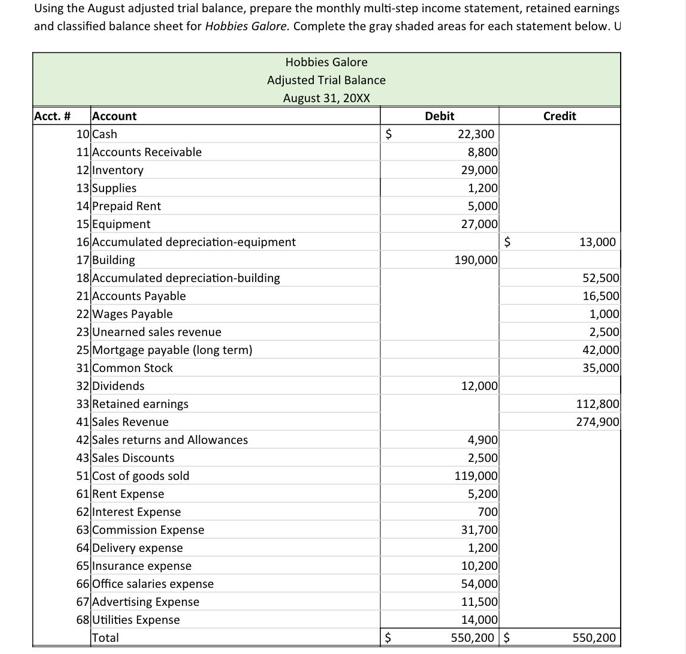

1. Prepare the multiple step income statement for the period ending August 31 20xx

2. Prepare the statement of retained earnings for the month ending in 8/31/20xx

3. Prepare the classified balance sheet for the month ending in 8/21/20xx

4. Answer these questions:

-How are the income statement and the balance sheet different? Why are the dates recorded differently on the sheet?

-Explain how gross profit, operating profit, and net profit are different?

-What is the book value of the equipment?

Expert Answer:

Solution for Problem1 below During January the following purchase transactions occurred 8Jan Purchased 5900 of merchandise from The Chocolate Shop Terms 215 n45 FOB shipping point The Candy Store prep... View the full answer

Auditing a risk based approach to conducting a quality audit

ISBN: 978-1133939153

9th edition

Authors: Karla Johnstone, Audrey Gramling, Larry Rittenberg