A discussion of the impact of different types of standards on motivations, and specifically the likely effect

Fantastic news! We've Found the answer you've been seeking!

Question:

A discussion of the impact of different types of standards on motivations, and specifically the likely effect on motivation of adopting the labour standard recommended for Harden Company by the engineering firm.

2. An evaluation of Harden Company's decision to employ dual standards in its standard cost system.

Transcribed Image Text:

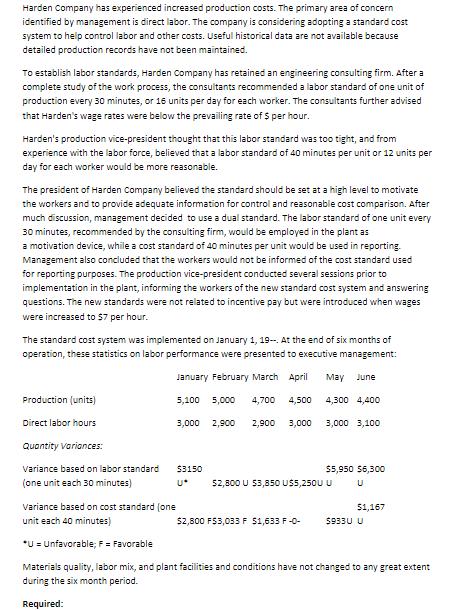

Harden Company has experienced increased production costs. The primary area of concern identified by management is direct labor. The company is considering adopting a standard cost system to help control labor and other costs. Useful historical data are not available because detailed production records have not been maintained. To establish labor standards, Harden Company has retained an engineering consulting firm. After a complete study of the work process, the consultants recommended a labor standard of one unit of production every 30 minutes, or 16 units per day for each worker. The consultants further advised that Harden's wage rates were below the prevailing rate of $ per hour. Harden's production vice-president thought that this labor standard was too tight, and from experience with the labor force, believed that a labor standard of 40 minutes per unit or 12 units per day for each worker would be more reasonable. The president of Harden Company believed the standard should be set at a high level to motivate the workers and to provide adequate information for control and reasonable cost comparison. After much discussion, management decided to use a dual standard. The labor standard of one unit every 30 minutes, recommended by the consulting firm, would be employed in the plant as a motivation device, while a cost standard of 40 minutes per unit would be used in reporting. Management also concluded that the workers would not be informed of the cost standard used for reporting purposes. The production vice-president conducted several sessions prior to implementation in the plant, informing the workers of the new standard cost system and answering questions. The new standards were not related to incentive pay but were introduced when wages were increased to 57 per hour. The standard cost system was implemented on January 1, 19--. At the end of six months of operation, these statistics on labor performance were presented to executive management: January February March April May June Production (units) 5,100 5,000 4,700 4,500 4,300 4,400 Direct labor hours 3,000 2,900 2,900 3,000 3,000 3,100 Quantity Variances: Variance based on labor standard $3150 $5,950 56,300 (one unit each 30 minutes) U* 52,800 U 53,850 US5,250U U Variance based on cost standard (one 51,167 unit each 40 minutes) $2,800 F53,033 F 51,633 F-0- 5933U U *U = Unfavorable, F = Favorable Materials quality, labor mix, and plant facilities and conditions have not changed to any great extent during the six month period. Required: Harden Company has experienced increased production costs. The primary area of concern identified by management is direct labor. The company is considering adopting a standard cost system to help control labor and other costs. Useful historical data are not available because detailed production records have not been maintained. To establish labor standards, Harden Company has retained an engineering consulting firm. After a complete study of the work process, the consultants recommended a labor standard of one unit of production every 30 minutes, or 16 units per day for each worker. The consultants further advised that Harden's wage rates were below the prevailing rate of $ per hour. Harden's production vice-president thought that this labor standard was too tight, and from experience with the labor force, believed that a labor standard of 40 minutes per unit or 12 units per day for each worker would be more reasonable. The president of Harden Company believed the standard should be set at a high level to motivate the workers and to provide adequate information for control and reasonable cost comparison. After much discussion, management decided to use a dual standard. The labor standard of one unit every 30 minutes, recommended by the consulting firm, would be employed in the plant as a motivation device, while a cost standard of 40 minutes per unit would be used in reporting. Management also concluded that the workers would not be informed of the cost standard used for reporting purposes. The production vice-president conducted several sessions prior to implementation in the plant, informing the workers of the new standard cost system and answering questions. The new standards were not related to incentive pay but were introduced when wages were increased to 57 per hour. The standard cost system was implemented on January 1, 19--. At the end of six months of operation, these statistics on labor performance were presented to executive management: January February March April May June Production (units) 5,100 5,000 4,700 4,500 4,300 4,400 Direct labor hours 3,000 2,900 2,900 3,000 3,000 3,100 Quantity Variances: Variance based on labor standard $3150 $5,950 56,300 (one unit each 30 minutes) U* 52,800 U 53,850 US5,250U U Variance based on cost standard (one 51,167 unit each 40 minutes) $2,800 F53,033 F 51,633 F-0- 5933U U *U = Unfavorable, F = Favorable Materials quality, labor mix, and plant facilities and conditions have not changed to any great extent during the six month period. Required: Harden Company has experienced increased production costs. The primary area of concern identified by management is direct labor. The company is considering adopting a standard cost system to help control labor and other costs. Useful historical data are not available because detailed production records have not been maintained. To establish labor standards, Harden Company has retained an engineering consulting firm. After a complete study of the work process, the consultants recommended a labor standard of one unit of production every 30 minutes, or 16 units per day for each worker. The consultants further advised that Harden's wage rates were below the prevailing rate of $ per hour. Harden's production vice-president thought that this labor standard was too tight, and from experience with the labor force, believed that a labor standard of 40 minutes per unit or 12 units per day for each worker would be more reasonable. The president of Harden Company believed the standard should be set at a high level to motivate the workers and to provide adequate information for control and reasonable cost comparison. After much discussion, management decided to use a dual standard. The labor standard of one unit every 30 minutes, recommended by the consulting firm, would be employed in the plant as a motivation device, while a cost standard of 40 minutes per unit would be used in reporting. Management also concluded that the workers would not be informed of the cost standard used for reporting purposes. The production vice-president conducted several sessions prior to implementation in the plant, informing the workers of the new standard cost system and answering questions. The new standards were not related to incentive pay but were introduced when wages were increased to 57 per hour. The standard cost system was implemented on January 1, 19--. At the end of six months of operation, these statistics on labor performance were presented to executive management: January February March April May June Production (units) 5,100 5,000 4,700 4,500 4,300 4,400 Direct labor hours 3,000 2,900 2,900 3,000 3,000 3,100 Quantity Variances: Variance based on labor standard $3150 $5,950 56,300 (one unit each 30 minutes) U* 52,800 U 53,850 US5,250U U Variance based on cost standard (one 51,167 unit each 40 minutes) $2,800 F53,033 F 51,633 F-0- 5933U U *U = Unfavorable, F = Favorable Materials quality, labor mix, and plant facilities and conditions have not changed to any great extent during the six month period. Required: Harden Company has experienced increased production costs. The primary area of concern identified by management is direct labor. The company is considering adopting a standard cost system to help control labor and other costs. Useful historical data are not available because detailed production records have not been maintained. To establish labor standards, Harden Company has retained an engineering consulting firm. After a complete study of the work process, the consultants recommended a labor standard of one unit of production every 30 minutes, or 16 units per day for each worker. The consultants further advised that Harden's wage rates were below the prevailing rate of $ per hour. Harden's production vice-president thought that this labor standard was too tight, and from experience with the labor force, believed that a labor standard of 40 minutes per unit or 12 units per day for each worker would be more reasonable. The president of Harden Company believed the standard should be set at a high level to motivate the workers and to provide adequate information for control and reasonable cost comparison. After much discussion, management decided to use a dual standard. The labor standard of one unit every 30 minutes, recommended by the consulting firm, would be employed in the plant as a motivation device, while a cost standard of 40 minutes per unit would be used in reporting. Management also concluded that the workers would not be informed of the cost standard used for reporting purposes. The production vice-president conducted several sessions prior to implementation in the plant, informing the workers of the new standard cost system and answering questions. The new standards were not related to incentive pay but were introduced when wages were increased to 57 per hour. The standard cost system was implemented on January 1, 19--. At the end of six months of operation, these statistics on labor performance were presented to executive management: January February March April May June Production (units) 5,100 5,000 4,700 4,500 4,300 4,400 Direct labor hours 3,000 2,900 2,900 3,000 3,000 3,100 Quantity Variances: Variance based on labor standard $3150 $5,950 56,300 (one unit each 30 minutes) U* 52,800 U 53,850 US5,250U U Variance based on cost standard (one 51,167 unit each 40 minutes) $2,800 F53,033 F 51,633 F-0- 5933U U *U = Unfavorable, F = Favorable Materials quality, labor mix, and plant facilities and conditions have not changed to any great extent during the six month period. Required: Harden Company has experienced increased production costs. The primary area of concern identified by management is direct labor. The company is considering adopting a standard cost system to help control labor and other costs. Useful historical data are not available because detailed production records have not been maintained. To establish labor standards, Harden Company has retained an engineering consulting firm. After a complete study of the work process, the consultants recommended a labor standard of one unit of production every 30 minutes, or 16 units per day for each worker. The consultants further advised that Harden's wage rates were below the prevailing rate of $ per hour. Harden's production vice-president thought that this labor standard was too tight, and from experience with the labor force, believed that a labor standard of 40 minutes per unit or 12 units per day for each worker would be more reasonable. The president of Harden Company believed the standard should be set at a high level to motivate the workers and to provide adequate information for control and reasonable cost comparison. After much discussion, management decided to use a dual standard. The labor standard of one unit every 30 minutes, recommended by the consulting firm, would be employed in the plant as a motivation device, while a cost standard of 40 minutes per unit would be used in reporting. Management also concluded that the workers would not be informed of the cost standard used for reporting purposes. The production vice-president conducted several sessions prior to implementation in the plant, informing the workers of the new standard cost system and answering questions. The new standards were not related to incentive pay but were introduced when wages were increased to 57 per hour. The standard cost system was implemented on January 1, 19--. At the end of six months of operation, these statistics on labor performance were presented to executive management: January February March April May June Production (units) 5,100 5,000 4,700 4,500 4,300 4,400 Direct labor hours 3,000 2,900 2,900 3,000 3,000 3,100 Quantity Variances: Variance based on labor standard $3150 $5,950 56,300 (one unit each 30 minutes) U* 52,800 U 53,850 US5,250U U Variance based on cost standard (one 51,167 unit each 40 minutes) $2,800 F53,033 F 51,633 F-0- 5933U U *U = Unfavorable, F = Favorable Materials quality, labor mix, and plant facilities and conditions have not changed to any great extent during the six month period. Required: Harden Company has experienced increased production costs. The primary area of concern identified by management is direct labor. The company is considering adopting a standard cost system to help control labor and other costs. Useful historical data are not available because detailed production records have not been maintained. To establish labor standards, Harden Company has retained an engineering consulting firm. After a complete study of the work process, the consultants recommended a labor standard of one unit of production every 30 minutes, or 16 units per day for each worker. The consultants further advised that Harden's wage rates were below the prevailing rate of $ per hour. Harden's production vice-president thought that this labor standard was too tight, and from experience with the labor force, believed that a labor standard of 40 minutes per unit or 12 units per day for each worker would be more reasonable. The president of Harden Company believed the standard should be set at a high level to motivate the workers and to provide adequate information for control and reasonable cost comparison. After much discussion, management decided to use a dual standard. The labor standard of one unit every 30 minutes, recommended by the consulting firm, would be employed in the plant as a motivation device, while a cost standard of 40 minutes per unit would be used in reporting. Management also concluded that the workers would not be informed of the cost standard used for reporting purposes. The production vice-president conducted several sessions prior to implementation in the plant, informing the workers of the new standard cost system and answering questions. The new standards were not related to incentive pay but were introduced when wages were increased to 57 per hour. The standard cost system was implemented on January 1, 19--. At the end of six months of operation, these statistics on labor performance were presented to executive management: January February March April May June Production (units) 5,100 5,000 4,700 4,500 4,300 4,400 Direct labor hours 3,000 2,900 2,900 3,000 3,000 3,100 Quantity Variances: Variance based on labor standard $3150 $5,950 56,300 (one unit each 30 minutes) U* 52,800 U 53,850 US5,250U U Variance based on cost standard (one 51,167 unit each 40 minutes) $2,800 F53,033 F 51,633 F-0- 5933U U *U = Unfavorable, F = Favorable Materials quality, labor mix, and plant facilities and conditions have not changed to any great extent during the six month period. Required: Harden Company has experienced increased production costs. The primary area of concern identified by management is direct labor. The company is considering adopting a standard cost system to help control labor and other costs. Useful historical data are not available because detailed production records have not been maintained. To establish labor standards, Harden Company has retained an engineering consulting firm. After a complete study of the work process, the consultants recommended a labor standard of one unit of production every 30 minutes, or 16 units per day for each worker. The consultants further advised that Harden's wage rates were below the prevailing rate of $ per hour. Harden's production vice-president thought that this labor standard was too tight, and from experience with the labor force, believed that a labor standard of 40 minutes per unit or 12 units per day for each worker would be more reasonable. The president of Harden Company believed the standard should be set at a high level to motivate the workers and to provide adequate information for control and reasonable cost comparison. After much discussion, management decided to use a dual standard. The labor standard of one unit every 30 minutes, recommended by the consulting firm, would be employed in the plant as a motivation device, while a cost standard of 40 minutes per unit would be used in reporting. Management also concluded that the workers would not be informed of the cost standard used for reporting purposes. The production vice-president conducted several sessions prior to implementation in the plant, informing the workers of the new standard cost system and answering questions. The new standards were not related to incentive pay but were introduced when wages were increased to 57 per hour. The standard cost system was implemented on January 1, 19--. At the end of six months of operation, these statistics on labor performance were presented to executive management: January February March April May June Production (units) 5,100 5,000 4,700 4,500 4,300 4,400 Direct labor hours 3,000 2,900 2,900 3,000 3,000 3,100 Quantity Variances: Variance based on labor standard $3150 $5,950 56,300 (one unit each 30 minutes) U* 52,800 U 53,850 US5,250U U Variance based on cost standard (one 51,167 unit each 40 minutes) $2,800 F53,033 F 51,633 F-0- 5933U U *U = Unfavorable, F = Favorable Materials quality, labor mix, and plant facilities and conditions have not changed to any great extent during the six month period. Required: Harden Company has experienced increased production costs. The primary area of concern identified by management is direct labor. The company is considering adopting a standard cost system to help control labor and other costs. Useful historical data are not available because detailed production records have not been maintained. To establish labor standards, Harden Company has retained an engineering consulting firm. After a complete study of the work process, the consultants recommended a labor standard of one unit of production every 30 minutes, or 16 units per day for each worker. The consultants further advised that Harden's wage rates were below the prevailing rate of $ per hour. Harden's production vice-president thought that this labor standard was too tight, and from experience with the labor force, believed that a labor standard of 40 minutes per unit or 12 units per day for each worker would be more reasonable. The president of Harden Company believed the standard should be set at a high level to motivate the workers and to provide adequate information for control and reasonable cost comparison. After much discussion, management decided to use a dual standard. The labor standard of one unit every 30 minutes, recommended by the consulting firm, would be employed in the plant as a motivation device, while a cost standard of 40 minutes per unit would be used in reporting. Management also concluded that the workers would not be informed of the cost standard used for reporting purposes. The production vice-president conducted several sessions prior to implementation in the plant, informing the workers of the new standard cost system and answering questions. The new standards were not related to incentive pay but were introduced when wages were increased to 57 per hour. The standard cost system was implemented on January 1, 19--. At the end of six months of operation, these statistics on labor performance were presented to executive management: January February March April May June Production (units) 5,100 5,000 4,700 4,500 4,300 4,400 Direct labor hours 3,000 2,900 2,900 3,000 3,000 3,100 Quantity Variances: Variance based on labor standard $3150 $5,950 56,300 (one unit each 30 minutes) U* 52,800 U 53,850 US5,250U U Variance based on cost standard (one 51,167 unit each 40 minutes) $2,800 F53,033 F 51,633 F-0- 5933U U *U = Unfavorable, F = Favorable Materials quality, labor mix, and plant facilities and conditions have not changed to any great extent during the six month period. Required:

Expert Answer:

Answer rating: 100% (QA)

Different types of standards can have different effects on motivation For example if a company adopt... View the full answer

Related Book For

Posted Date:

Students also viewed these accounting questions

-

How would you explain a companys decision to employ centralized decision-making processes and decentralized control processes, considering the two are so interconnected? Provide an industry example...

-

Standard direct labor hours budgeted by Witherspoon Company for April production were 1,200, with factory overhead at that level budgeted at $16,800, of which $4,800 is variable and $12,000 is fixed....

-

Standard direct labor hours budgeted by Turner Company for February production were 2,000. Factory overhead at that level was budgeted at $10,000, of which $3,000 is variable. Actual direct labor...

-

On May 1, Johnson Corporation purchased inventory for $40,000 on credit. On May 15, Johnson sold inventory with a cost of $10,000 for $25,000 on credit. Prepare journal entries to record these...

-

Compare structure and culture of two or more firms. Which would you prefer to work for?

-

The plaintiff and the defendant entered into a three- year contract in which the defendant would be the sole supplier of steel parts that the plaintiff used in its products. A dispute arose after the...

-

What is meant by a systems control flow?

-

The Ulmer Uranium Company is deciding whether or not it should open a strip mine, the net cost of which is $4.4 million. Net cash inflows are expected to be $27.7 million, all coming at the end of...

-

Make This ERD Diagram On Microsoft Visio Software and upload Answer. Customer name Email (Password) Customer App/website Logins View JD Admin (Password) Manage Product name) Category Product Courier...

-

Suppose there is an urn containing 300 balls, of those 100 balls are red, while the remaining 200 balls are either black or white with unknown proportions. The balls are well-mixed that any...

-

a) Sketch the velocity distribution against radial positions in a perfectly smooth pipe with a circular cross-section for: a laminar flow; a turbulent flow. i) ii) [2 marks] [2 marks] b) A pump...

-

Determine whether each of the figures in Problems 30-37 will be a solution to an Instant Insanity puzzle.

-

Use XDR and htonl to encode a 1000-element array of integers. Measure and compare the performance of each. How do these compare to a simple loop that reads and writes a 1000-element array of...

-

Write your own implementation of htonl. Using both your own htonl and (if little-endian hardware is available) the standard library version, run appropriate experiments to determine how much longer...

-

a. One variation of Instant Insanity is a puzzle with five blocks instead of four. How many arrangements are possible? b. If you carry out one arrangement every second, how much time is required to...

-

What are the different approaches to test the sensitivity of a CBA model?

-

Which statement best describes an example of a short-term investment strategy? A. Mariam invests $4,000 in a mutual fund to create a new income stream. B. Mariam buys an IRA that she can't withdraw...

-

As long as we can't lose any money, we have a risk-free investment." Discuss this comment. Q2: Both investing and gambling can be defined as "undertaking risk in order to earn a profit." Explain how...

-

Continue with Exercise 14.56. The college responds to Shemekia. Based on the same information, what argument could the college make for why she shouldnt be offered admission? Data from exercise 14.56...

-

Given R = 3, C = 3, and n = 11, find (a) q Rows , (b) q Columns , and (c) q Cells .

-

If df Between = 3 and df Within = 36, what is F cv if = .05

-

How does the product life cycle influence marketing strategy decisions?

-

What are the stages in the product life cycle?

-

What is the difference between secondary demand and primary demand?

Study smarter with the SolutionInn App