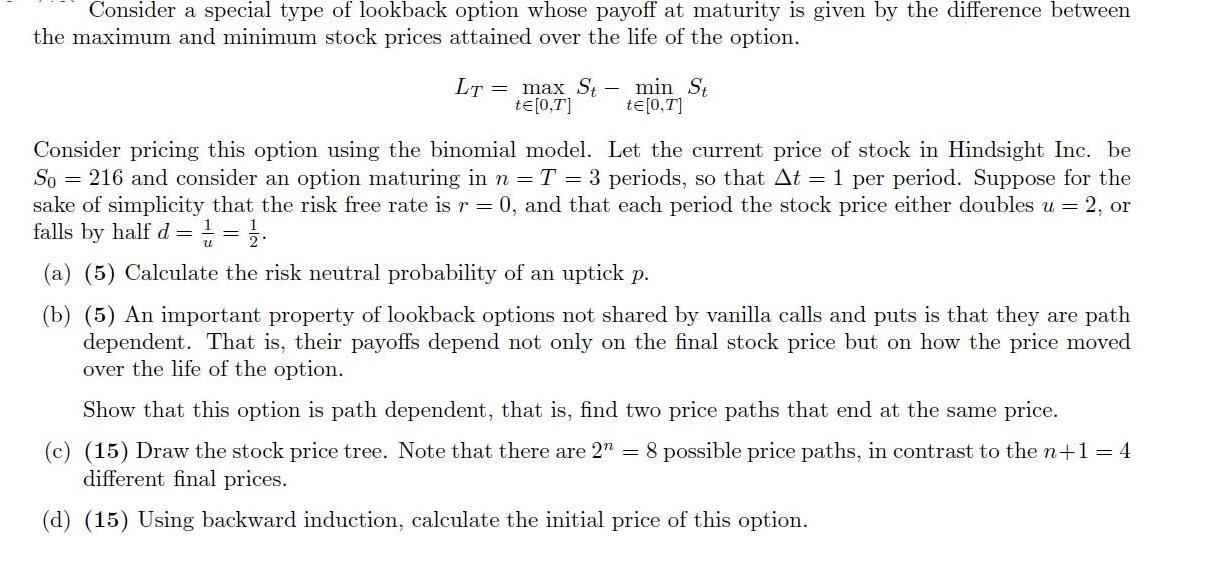

Consider a special type of lookback option whose payoff at maturity is given by the difference...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

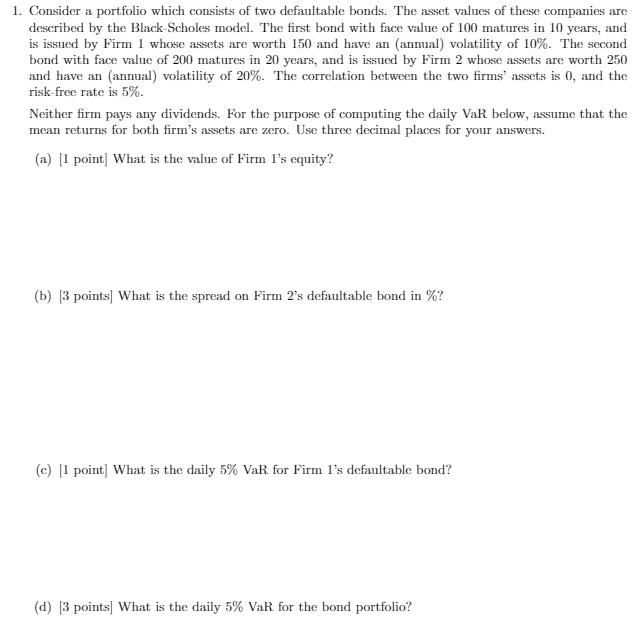

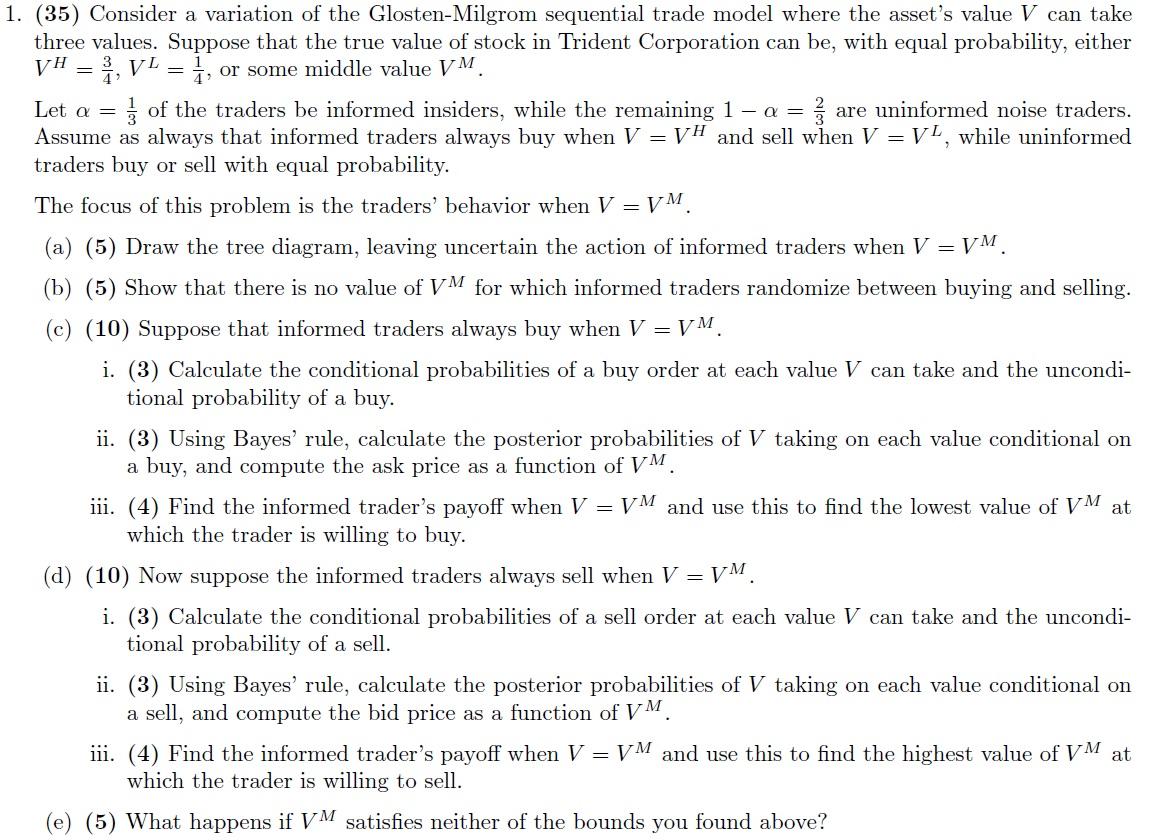

Consider a special type of lookback option whose payoff at maturity is given by the difference between the maximum and minimum stock prices attained over the life of the option. LT = max St te [0,T] min St te [0,T] Consider pricing this option using the binomial model. Let the current price of stock in Hindsight Inc. be So = 216 and consider an option maturing in n = T = 3 periods, so that At = 1 per period. Suppose for the sake of simplicity that the risk free rate is r = 0, and that each period the stock price either doubles u = 2, or falls by half d = 1=1/1 (a) (5) Calculate the risk neutral probability of an uptick p. (b) (5) An important property of lookback options not shared by vanilla calls and puts is that they are path dependent. That is, their payoffs depend not only on the final stock price but on how the price moved over the life of the option. Show that this option is path dependent, that is, find two price paths that end at the same price. (c) (15) Draw the stock price tree. Note that there are 2" = 8 possible price paths, in contrast to the n+1 = 4 different final prices. (d) (15) Using backward induction, calculate the initial price of this option. 1. Consider a portfolio which consists of two defaultable bonds. The asset values of these companies are described by the Black-Scholes model. The first bond with face value of 100 matures in 10 years, and is issued by Firm 1 whose assets are worth 150 and have an (annual) volatility of 10%. The second bond with face value of 200 matures in 20 years, and is issued by Firm 2 whose assets are worth 250 and have an (annual) volatility of 20%. The correlation between the two firms' assets is 0, and the risk-free rate is 5%. Neither firm pays any dividends. For the purpose of computing the daily VaR below, assume that the mean returns for both firm's assets are zero. Use three decimal places for your answers. (a) [1 point] What is the value of Firm I's equity? (b) [3 points] What is the spread on Firm 2's defaultable bond in %? (c) [1 point] What is the daily 5% VaR for Firm I's defaultable bond? (d) [3 points] What is the daily 5% VaR for the bond portfolio? 1. (35) Consider a variation of the Glosten-Milgrom sequential trade model where the asset's value V can take three values. Suppose that the true value of stock in Trident Corporation can be, with equal probability, either VH 3,VL = 1, or some middle value VM Let a = 3 of the traders be informed insiders, while the remaining 1 - a = 륭 are uninformed noise traders. Assume as always that informed traders always buy when V = VH and sell when V = VL, while uninformed traders buy or sell with equal probability. - The focus of this problem is the traders' behavior when V = (a) (5) Draw the tree diagram, leaving uncertain the action of informed traders when V = VM. (b) (5) Show that there is no value of VM for which informed traders randomize between buying and selling. (c) (10) Suppose that informed traders always buy when V = VM i. (3) Calculate the conditional probabilities of a buy order at each value V can take and the uncondi- tional probability of a buy. ii. (3) Using Bayes' rule, calculate the posterior probabilities of V taking on each value conditional on a buy, and compute the ask price as a function of VM iii. (4) Find the informed trader's payoff when V = VM and use this to find the lowest value of VM at which the trader is willing to buy. (d) (10) Now suppose the informed traders always sell when V - ᏙᎷ . i. (3) Calculate the conditional probabilities of a sell order at each value V can take and the uncondi- tional probability of a sell. ii. (3) Using Bayes' rule, calculate the posterior probabilities of V taking on each value conditional on a sell, and compute the bid price as a function of VM. iii. (4) Find the informed trader's payoff when V = VM and use this to find the highest value of VM at which the trader is willing to sell. (5) What happens if VM satisfies neither of the bounds you found above? Consider a special type of lookback option whose payoff at maturity is given by the difference between the maximum and minimum stock prices attained over the life of the option. LT = max St te [0,T] min St te [0,T] Consider pricing this option using the binomial model. Let the current price of stock in Hindsight Inc. be So = 216 and consider an option maturing in n = T = 3 periods, so that At = 1 per period. Suppose for the sake of simplicity that the risk free rate is r = 0, and that each period the stock price either doubles u = 2, or falls by half d = 1=1/1 (a) (5) Calculate the risk neutral probability of an uptick p. (b) (5) An important property of lookback options not shared by vanilla calls and puts is that they are path dependent. That is, their payoffs depend not only on the final stock price but on how the price moved over the life of the option. Show that this option is path dependent, that is, find two price paths that end at the same price. (c) (15) Draw the stock price tree. Note that there are 2" = 8 possible price paths, in contrast to the n+1 = 4 different final prices. (d) (15) Using backward induction, calculate the initial price of this option. 1. Consider a portfolio which consists of two defaultable bonds. The asset values of these companies are described by the Black-Scholes model. The first bond with face value of 100 matures in 10 years, and is issued by Firm 1 whose assets are worth 150 and have an (annual) volatility of 10%. The second bond with face value of 200 matures in 20 years, and is issued by Firm 2 whose assets are worth 250 and have an (annual) volatility of 20%. The correlation between the two firms' assets is 0, and the risk-free rate is 5%. Neither firm pays any dividends. For the purpose of computing the daily VaR below, assume that the mean returns for both firm's assets are zero. Use three decimal places for your answers. (a) [1 point] What is the value of Firm I's equity? (b) [3 points] What is the spread on Firm 2's defaultable bond in %? (c) [1 point] What is the daily 5% VaR for Firm I's defaultable bond? (d) [3 points] What is the daily 5% VaR for the bond portfolio? 1. (35) Consider a variation of the Glosten-Milgrom sequential trade model where the asset's value V can take three values. Suppose that the true value of stock in Trident Corporation can be, with equal probability, either VH 3,VL = 1, or some middle value VM Let a = 3 of the traders be informed insiders, while the remaining 1 - a = 륭 are uninformed noise traders. Assume as always that informed traders always buy when V = VH and sell when V = VL, while uninformed traders buy or sell with equal probability. - The focus of this problem is the traders' behavior when V = (a) (5) Draw the tree diagram, leaving uncertain the action of informed traders when V = VM. (b) (5) Show that there is no value of VM for which informed traders randomize between buying and selling. (c) (10) Suppose that informed traders always buy when V = VM i. (3) Calculate the conditional probabilities of a buy order at each value V can take and the uncondi- tional probability of a buy. ii. (3) Using Bayes' rule, calculate the posterior probabilities of V taking on each value conditional on a buy, and compute the ask price as a function of VM iii. (4) Find the informed trader's payoff when V = VM and use this to find the lowest value of VM at which the trader is willing to buy. (d) (10) Now suppose the informed traders always sell when V - ᏙᎷ . i. (3) Calculate the conditional probabilities of a sell order at each value V can take and the uncondi- tional probability of a sell. ii. (3) Using Bayes' rule, calculate the posterior probabilities of V taking on each value conditional on a sell, and compute the bid price as a function of VM. iii. (4) Find the informed trader's payoff when V = VM and use this to find the highest value of VM at which the trader is willing to sell. (5) What happens if VM satisfies neither of the bounds you found above?

Expert Answer:

Answer rating: 100% (QA)

a To calculate the value of Firm Is equity we need to subtract the face value of the bond from the v... View the full answer

Related Book For

An Introduction to Derivative Securities Financial Markets and Risk Management

ISBN: 978-0393913071

1st edition

Authors: Robert A. Jarrow, Arkadev Chatterjee

Posted Date:

Students also viewed these finance questions

-

Consider the following exotic option whose payoff at maturity is given by the square root of the stock price less the strike price if it has a positive value, zero otherwise: max[ S(2) K,0]. Using...

-

KYC's stock price can go up by 15 percent every year, or down by 10 percent. Both outcomes are equally likely. The risk free rate is 5 percent, and the current stock price of KYC is 100. (a) Price a...

-

Consider the following exotic option whose payoff at expiration is given by the stock price squared less a strike price if it has a positive value, zero otherwise: max[S(1)2 K, 0] Assuming that the...

-

A company is implementing Dynamics 365 Supply Chain Management. The company plans to implement the solution in a phased approach across several incremental projects. The project manager needs a...

-

The structural components of modern aircraft are commonly fabricated of high-performance composite materials. These materials are fabricated by impregnating mats of extremely strong fibers that are...

-

In a simple random sample of size 75, there were 42 individuals in the category of interest. a. Compute the sample proportion p. b. Are the assumptions for a hypothesis test satisfied? Explain. c. It...

-

What rules apply to service and filing of pleadings?

-

The mix of salary and commission Belleville Fashions sells high-quality womens, mens, and childrens clothing. The store employs a sales staff of 11 full-time employees and 12 part-time employees....

-

Working required Unanswered Question 8 Correct Answer 0/200 pts Let f (x) be a function defined for all real numbers, such that f(3x-9) = f(x) for all R. If f(x) 5x2 +7 lim x2 = 20 2-x find (if it...

-

Copy Fast Services was opened by Jarenz on January 1, 2008 with a cash investment of P 10,000. Additional transactions for the month are as follows: Jan 245678 6 7 8 9 14 15 19 20 25 6456 33333 30 31...

-

Br Name the following molecules. JS 2 2

-

Make a folio of 5 different paper sizes, types, colors and their associated use. Also 5 different envelopes sizes, types and colors.

-

A particle is moving along a line. Its displacement (in centimeters) after t seconds is: s(t) = -4t Find the Instantaneous velocity at t = 2. Write your answer as an integer or a fraction. Simplify...

-

How are today's Evolving media content and mobility options increasing or decrease the quality and value of the media we have available to USE AS CONSUMER'S !"

-

Mr. U is actively involved in church activities in his community. During the current year, he incurred the following church-related expenses: Cash contributed to the church $2,000 Round-trip mileage...

-

Consider this expression. m2 - 71+n2 When m = -2 and n 5, the value of the expression is

-

What is maintenance CAPEX for Poodle Bites in Year 4? Poodle Bites Inc. Selected Financial Information Revenues Depreciation PP&E, Net CAPEX Depreciation Rate Year 3 $782,431 $621,568 26,269 Year 4...

-

Extend Algorithms 3.4 and 3.5 to include as output the first and second derivatives of the spline at the nodes.

-

Suppose a two-year Treasury note is trading at its par value $1,000. You examine the cash flows, and if you sell them individually in the market, you get $47.85 for the six-month coupon, $45.79 for...

-

Explain why derivatives are zero-sum games.

-

What is marking-to-market for a future? Why is this marking-to-market important for reducing counterparty risk?

-

Using data from a random sample of elementary schools, a researcher regresses average test scores on the fraction of students who qualify for reduced-price meals. The regression indicates a negative...

-

In the demand curve model of Equation (12.3), is \(\ln \left(P_{i}^{\text {butter }} ight)\) positively or negatively correlated with the error, \(u_{i}\) ? If \(\beta_{1}\) is estimated by OLS,...

-

In the study of cigarette demand in this chapter, suppose we used as an instrument the number of trees per capita in the state. Is this instrument relevant? Is it exogenous? Is it a valid instrument?

Study smarter with the SolutionInn App