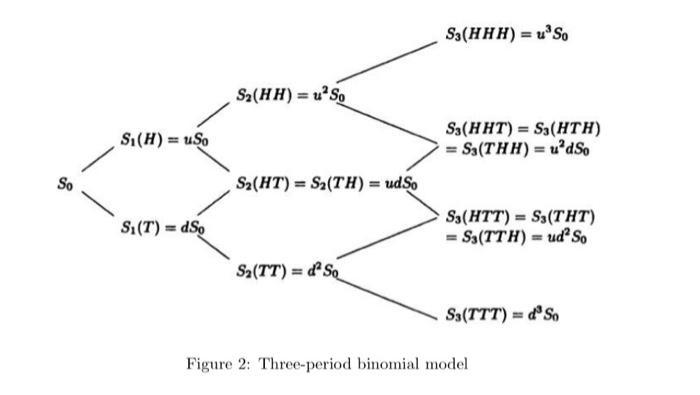

2. Consider a three-period binomial model in Figure 2 with So 4, u = 2, and...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

SOLUTION To answer these questions we need to use the principles of the binomial option pricing model Lets go through each question step by step a The ... View the full answer

Related Book For

Income Tax Fundamentals 2013

ISBN: 9781285586618

31st Edition

Authors: Gerald E. Whittenburg, Martha Altus Buller, Steven L Gill

Posted Date: