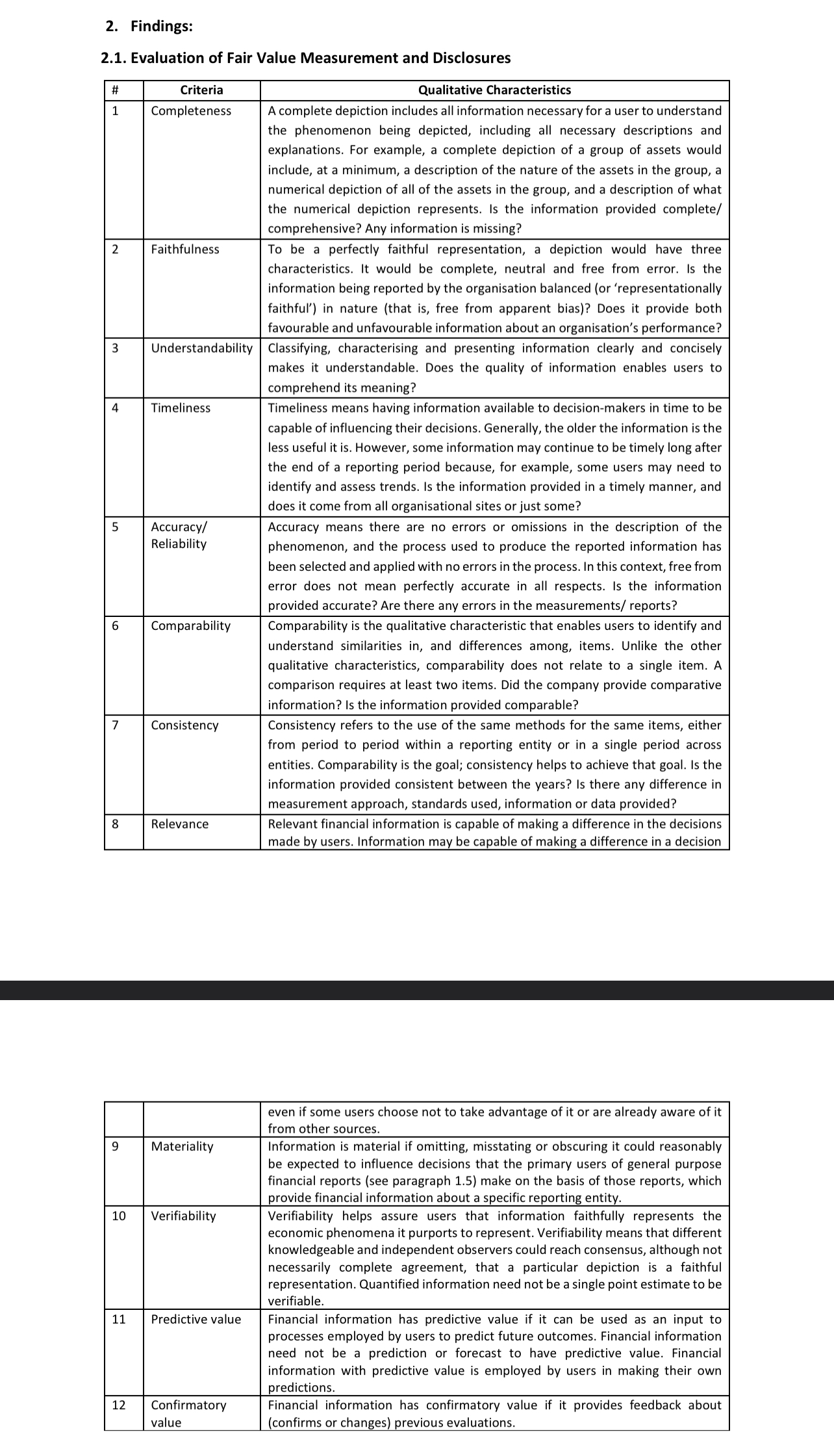

2. Findings: 2.1. Evaluation of Fair Value Measurement and Disclosures # 1 Criteria Completeness 2 Faithfulness...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

2. Findings: 2.1. Evaluation of Fair Value Measurement and Disclosures # 1 Criteria Completeness 2 Faithfulness 3 Qualitative Characteristics A complete depiction includes all information necessary for a user to understand the phenomenon being depicted, including all necessary descriptions and explanations. For example, a complete depiction of a group of assets would include, at a minimum, a description of the nature of the assets in the group, a numerical depiction of all of the assets in the group, and a description of what the numerical depiction represents. Is the information provided complete/ comprehensive? Any information is missing? To be a perfectly faithful representation, a depiction would have three characteristics. It would be complete, neutral and free from error. Is the information being reported by the organisation balanced (or 'representationally faithful') in nature (that is, free from apparent bias)? Does it provide both. favourable and unfavourable information about an organisation's performance? Understandability Classifying, characterising and presenting information clearly and concisely makes it understandable. Does the quality of information enables users to comprehend its meaning? 4 Timeliness 5 Accuracy/ Reliability 6 Comparability 7 Consistency 8 Relevance Timeliness means having information available to decision-makers in time to be capable of influencing their decisions. Generally, the older the information is the less useful it is. However, some information may continue to be timely long after the end of a reporting period because, for example, some users may need to identify and assess trends. Is the information provided in a timely manner, and does it come from all organisational sites or just some? Accuracy means there are no errors or omissions in the description of the phenomenon, and the process used to produce the reported information has been selected and applied with no errors in the process. In this context, free from error does not mean perfectly accurate in all respects. Is the information provided accurate? Are there any errors in the measurements/reports? Comparability is the qualitative characteristic that enables users to identify and understand similarities in, and differences among, items. Unlike the other qualitative characteristics, comparability does not relate to a single item. A comparison requires at least two items. Did the company provide comparative information? Is the information provided comparable? Consistency refers to the use of the same methods for the same items, either from period to period within a reporting entity or in a single period across entities. Comparability is the goal; consistency helps to achieve that goal. Is the information provided consistent between the years? Is there any difference in measurement approach, standards used, information or data provided? Relevant financial information is capable of making a difference in the decisions made by users. Information may be capable of making a difference in a decision 9 Materiality 10 11 Verifiability Predictive value Confirmatory 12 value even if some users choose not to take advantage of it or are already aware of it from other sources. Information is material if omitting, misstating or obscuring it could reasonably be expected to influence decisions that the primary users of general purpose financial reports (see paragraph 1.5) make on the basis of those reports, which provide financial information about a specific reporting entity. Verifiability helps assure users that information faithfully represents the economic phenomena it purports to represent. Verifiability means that different knowledgeable and independent observers could reach consensus, although not necessarily complete agreement, that a particular depiction is a faithful representation. Quantified information need not be a single point estimate to be verifiable. Financial information has predictive value if it can be used as an input to processes employed by users to predict future outcomes. Financial information need not be a prediction or forecast to have predictive value. Financial information with predictive value is employed by users in making their own predictions. Financial information has confirmatory value if it provides feedback about (confirms or changes) previous evaluations. 2. Findings: 2.1. Evaluation of Fair Value Measurement and Disclosures # 1 Criteria Completeness 2 Faithfulness 3 Qualitative Characteristics A complete depiction includes all information necessary for a user to understand the phenomenon being depicted, including all necessary descriptions and explanations. For example, a complete depiction of a group of assets would include, at a minimum, a description of the nature of the assets in the group, a numerical depiction of all of the assets in the group, and a description of what the numerical depiction represents. Is the information provided complete/ comprehensive? Any information is missing? To be a perfectly faithful representation, a depiction would have three characteristics. It would be complete, neutral and free from error. Is the information being reported by the organisation balanced (or 'representationally faithful') in nature (that is, free from apparent bias)? Does it provide both. favourable and unfavourable information about an organisation's performance? Understandability Classifying, characterising and presenting information clearly and concisely makes it understandable. Does the quality of information enables users to comprehend its meaning? 4 Timeliness 5 Accuracy/ Reliability 6 Comparability 7 Consistency 8 Relevance Timeliness means having information available to decision-makers in time to be capable of influencing their decisions. Generally, the older the information is the less useful it is. However, some information may continue to be timely long after the end of a reporting period because, for example, some users may need to identify and assess trends. Is the information provided in a timely manner, and does it come from all organisational sites or just some? Accuracy means there are no errors or omissions in the description of the phenomenon, and the process used to produce the reported information has been selected and applied with no errors in the process. In this context, free from error does not mean perfectly accurate in all respects. Is the information provided accurate? Are there any errors in the measurements/reports? Comparability is the qualitative characteristic that enables users to identify and understand similarities in, and differences among, items. Unlike the other qualitative characteristics, comparability does not relate to a single item. A comparison requires at least two items. Did the company provide comparative information? Is the information provided comparable? Consistency refers to the use of the same methods for the same items, either from period to period within a reporting entity or in a single period across entities. Comparability is the goal; consistency helps to achieve that goal. Is the information provided consistent between the years? Is there any difference in measurement approach, standards used, information or data provided? Relevant financial information is capable of making a difference in the decisions made by users. Information may be capable of making a difference in a decision 9 Materiality 10 11 Verifiability Predictive value Confirmatory 12 value even if some users choose not to take advantage of it or are already aware of it from other sources. Information is material if omitting, misstating or obscuring it could reasonably be expected to influence decisions that the primary users of general purpose financial reports (see paragraph 1.5) make on the basis of those reports, which provide financial information about a specific reporting entity. Verifiability helps assure users that information faithfully represents the economic phenomena it purports to represent. Verifiability means that different knowledgeable and independent observers could reach consensus, although not necessarily complete agreement, that a particular depiction is a faithful representation. Quantified information need not be a single point estimate to be verifiable. Financial information has predictive value if it can be used as an input to processes employed by users to predict future outcomes. Financial information need not be a prediction or forecast to have predictive value. Financial information with predictive value is employed by users in making their own predictions. Financial information has confirmatory value if it provides feedback about (confirms or changes) previous evaluations.

Expert Answer:

Posted Date:

Students also viewed these accounting questions

-

Keshk, Walied; Lu, HungYuan Richard; Mande, Vivek (2020). How have US banks adopted the Financial Accounting Standards Board's Level 3 fair value disclosure rules? Accounting & Finance 60, April...

-

Depreciation policy is an important decision made by a company's Finance Director. A company has purchased some equipment for 85,000, with an estimated scrap value of 9,000 at the end of its useful...

-

1. Based on Vicente Ruizs actions and his conversation with Chuck Moore, what differences do you detect in cultural attitudes toward communications in Mexico as compared with the United States? Is...

-

Lynch Brothers manufactures conveyor belts. Early in January 2011, Lynch Brothers constructed its own building at a materials, labor, and overhead cost of $900,000. Lynch Brothers also paid for...

-

Determine the components of the reactions at A and E when a counterclockwise couple of magnitude120 N m is applied to the frame (a) At B, (b) At D. 100mm - 400 mm 250 m

-

The management of Skysong Inc., a small private company that uses the cost recovery impairment model, was discussing whether certain equipment should be written down as a charge to current operations...

-

374. Maximize U(x, y) = 8x4/5 y 1/5; 4x + 2y = 12

-

Why do companies divest assets?

-

In the mortgage industry, more and more nonconforming loans were purchased, pooled, and segmented into tranches of different grades of risk and then sold to investors as __________ securities.

-

The Commodities Futures Modernization Act of 2000 and the repeal of the Glass-Steagall Act in 1999: (a) Effectively ended the separation of commercial banking from investment banking. (b) Ended the...

-

Explain the reset clause in the pay-option ARM loan agreement.

-

In small groups or in pairs, and based upon the current economic environment, research and discuss top CFO priorities.

Study smarter with the SolutionInn App