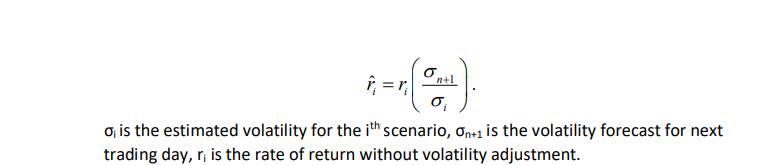

Your task is to estimate expected shortfall (ES) for an equity portfolio using the historical simulation...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

Estimating Expected Shortfall ES for an Equity Portfolio While I cannot execute the calculations involved due to the lack of specific data on daily returns and volatilities I can guide you through the ... View the full answer

Related Book For

Posted Date: