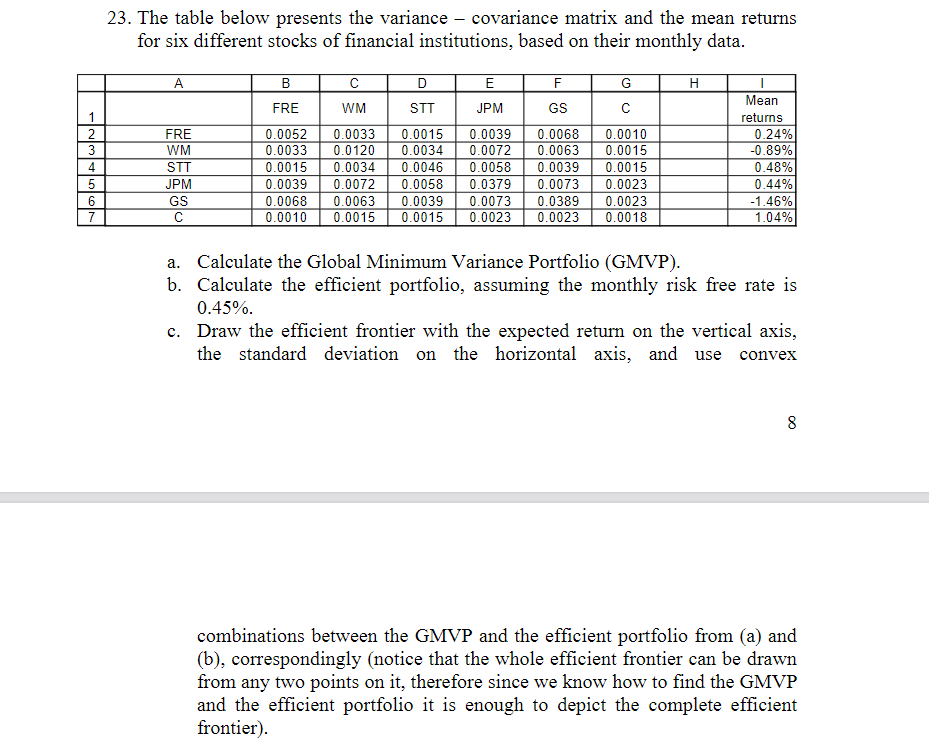

23. The table below presents the variance - covariance matrix and the mean returns for six...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

23. The table below presents the variance - covariance matrix and the mean returns for six different stocks of financial institutions, based on their monthly data. A B C D E F G H Mean FRE WM STT JPM GS 1 returns 2 FRE 0.0052 0.0033 0.0015 3 WM 0.0033 0.0120 0.0034 0.0039 0.0068 0.0010 0.0072 0.0063 0.0015 0.24% -0.89% 4 STT 0.0015 0.0034 5 JPM 0.0039 0.0072 6 GS 7 C 0.0046 0.0058 0.0379 0.0068 0.0063 0.0039 0.0073 0.0010 0.0015 0.0015 0.0023 0.0058 0.0039 0.0015 0.48% 0.0073 0.0023 0.0389 0.0023 0.0023 0.0018 0.44% -1.46% 1.04% a. Calculate the Global Minimum Variance Portfolio (GMVP). b. Calculate the efficient portfolio, assuming the monthly risk free rate is 0.45%. c. Draw the efficient frontier with the expected return on the vertical axis, the standard deviation on the horizontal axis, and use convex 8 combinations between the GMVP and the efficient portfolio from (a) and (b), correspondingly (notice that the whole efficient frontier can be drawn from any two points on it, therefore since we know how to find the GMVP and the efficient portfolio it is enough to depict the complete efficient frontier). 24. Repeat the same steps from question 23, but this time while the variance - covariance matrix is an equally weighted combination (this is actually the shrinkage method with Lambda = 0.5) of the sample matrix in question 23, and a simple diagonal matrix of only the variances (it means the variances along the main diagonal and '0' elsewhere). 23. The table below presents the variance - covariance matrix and the mean returns for six different stocks of financial institutions, based on their monthly data. A B C D E F G H Mean FRE WM STT JPM GS 1 returns 2 FRE 0.0052 0.0033 0.0015 3 WM 0.0033 0.0120 0.0034 0.0039 0.0068 0.0010 0.0072 0.0063 0.0015 0.24% -0.89% 4 STT 0.0015 0.0034 5 JPM 0.0039 0.0072 6 GS 7 C 0.0046 0.0058 0.0379 0.0068 0.0063 0.0039 0.0073 0.0010 0.0015 0.0015 0.0023 0.0058 0.0039 0.0015 0.48% 0.0073 0.0023 0.0389 0.0023 0.0023 0.0018 0.44% -1.46% 1.04% a. Calculate the Global Minimum Variance Portfolio (GMVP). b. Calculate the efficient portfolio, assuming the monthly risk free rate is 0.45%. c. Draw the efficient frontier with the expected return on the vertical axis, the standard deviation on the horizontal axis, and use convex 8 combinations between the GMVP and the efficient portfolio from (a) and (b), correspondingly (notice that the whole efficient frontier can be drawn from any two points on it, therefore since we know how to find the GMVP and the efficient portfolio it is enough to depict the complete efficient frontier). 24. Repeat the same steps from question 23, but this time while the variance - covariance matrix is an equally weighted combination (this is actually the shrinkage method with Lambda = 0.5) of the sample matrix in question 23, and a simple diagonal matrix of only the variances (it means the variances along the main diagonal and '0' elsewhere).

Expert Answer:

Posted Date:

Students also viewed these finance questions

-

Nisha has completed her MBA and has joined a company which was going to raise fund from long term sources such as Debt and Equity. Nisha was asked by her manager to prepare a report on which could be...

-

Determine the annual payment required to fund a future annual annuity of $12,000 per year. You will fund this future liability over the next five years, with the first payment to occur one year from...

-

Calculate product compositions, stage temperatures, interstage vapor and liquid flow rates and compositions, reboiler duty, and condenser duty for the following column specifications. Feed...

-

Use the balance sheet equation to determine the missing values below. Common Assets Liabilities Stock Retained Earnings 320,000 150,000 45,000 ? ? 75,000 30,000 40,000 250,000 90,000 ? 120,000...

-

The educational level of Americans has increased throughout the 20th century. The following U.S. Census data show the level of education attained by American adults over the age of 25 years at...

-

Question Investor C has planned to establish a restaurant in 2 years. The cost to develop a small restaurant is $150,000. Investor C would like to know the required saving amount is needed to deposit...

-

On the first day of the fiscal year, Lisbon Co. issued $1,000,000 of 10-year, 7% bonds for $1,050,000, with interest payable semiannually. The fiscal year of the company is the calendar year. Prepare...

-

Coffin Corporation wants to buy a new hearse for $\$ 60,000$. It will last for five years. They expect to make 100 trips per year. Coffin uses a discount rate of 6 percent. If they charge $\$ 150$...

-

Which system of electing judges, partisan or nonpartisan, do you think is better for preserving the goals of the judicial system?

-

Do you think that there should be more cooperation or sharing of administrative responsibilities either among the court staff or among judges to improve the scheduling and timing problems?

-

Suppose that you have $\$ 50,000$ available today and can invest it at $7 %$ per year. How long will it be before you have accumulated $\$ 500,000$ in the investment?

-

Given that most judges were attorneys who specialized in only one or two areas of law, should they be required to learn (take classes on) other areas of law rather than leaving it up to them to put...

-

SUPERIOR LId makes shoes in two ranges such as Basic and Super. Information relating to each of these products is set out below. Basic Super Selling price per unit Material Cost per unit Labour time...

-

Explain why it is not wise to accept a null hypothesis.

-

Show that formula (2.24) holds for the \(0-1\) loss with \(0-1\) response.

-

Observe that the learner \(g_{\mathscr{T}}\) can be written as a linear combination of the response variable: \(g_{\mathscr{T}}(\boldsymbol{x})=\boldsymbol{x}^{\top} \mathbf{X}^{+} \boldsymbol{Y}\)....

-

Consider again the polynomial regression Example 2. 1. Use the fact that \(\mathbb{E}_{\mathbf{X}} \widehat{\boldsymbol{\beta}}=\mathbf{X}^{+} \boldsymbol{h}^{*}(\boldsymbol{u})\), where...

Study smarter with the SolutionInn App