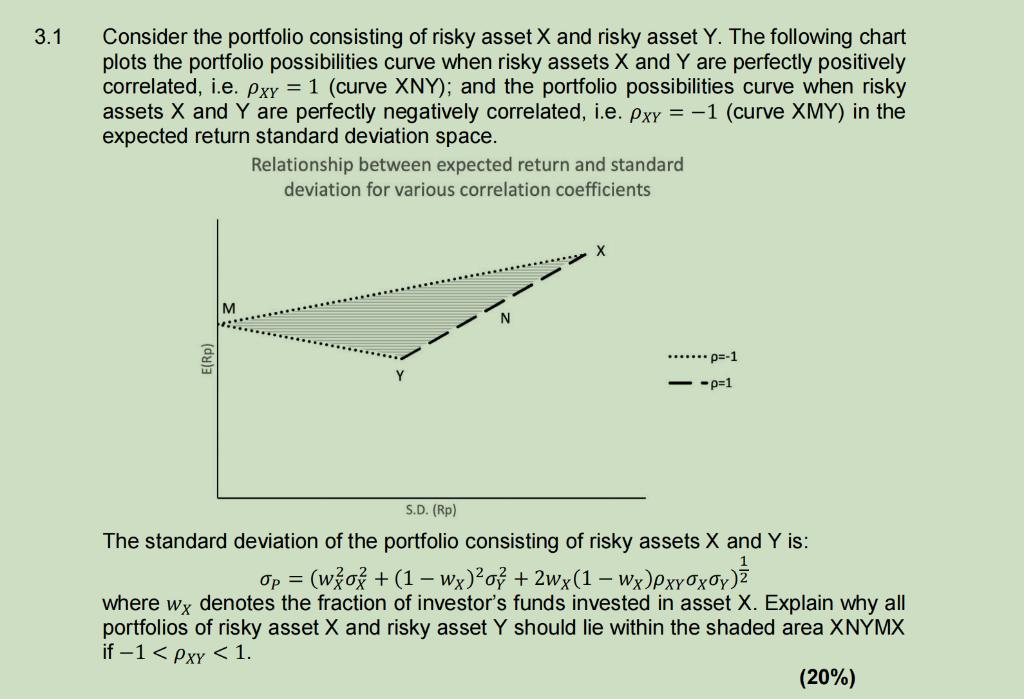

3.1 Consider the portfolio consisting of risky asset X and risky asset Y. The following chart...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

Related Book For

Fundamentals Of Investing

ISBN: 9780135175217

14th Edition

Authors: Scott B. Smart, Lawrence J. Gitman, Michael D. Joehnk

Posted Date: