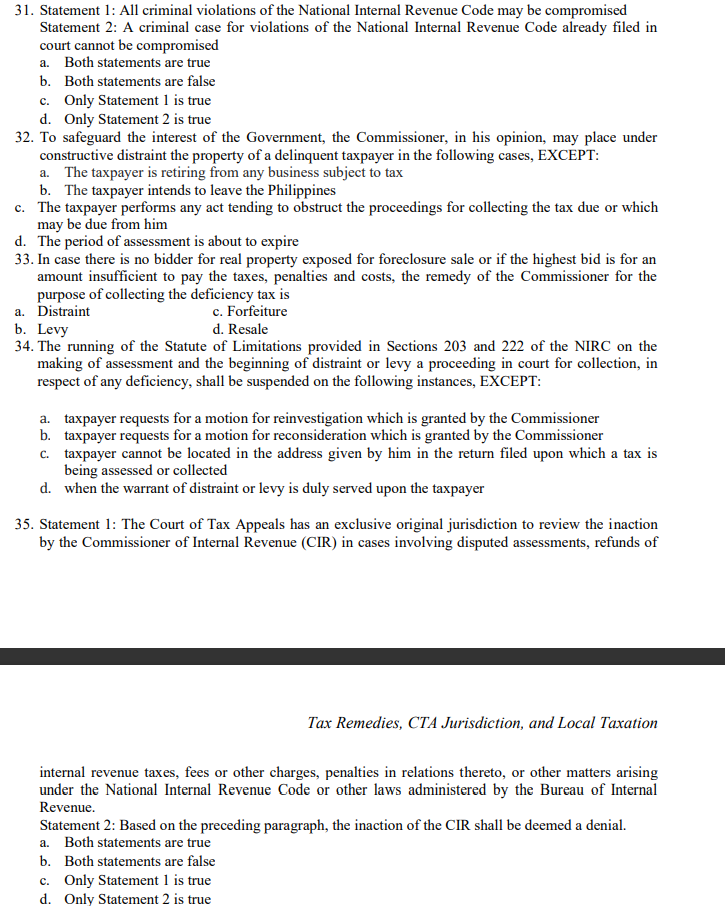

31. Statement 1: All criminal violations of the National Internal Revenue Code may be compromised Statement...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

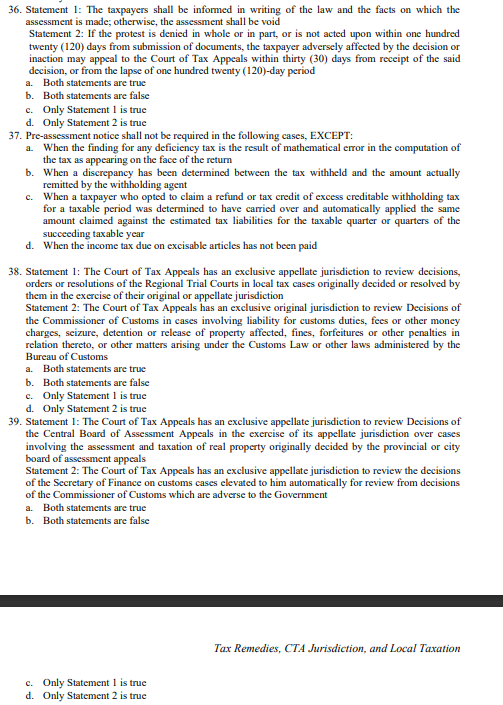

31. Statement 1: All criminal violations of the National Internal Revenue Code may be compromised Statement 2: A criminal case for violations of the National Internal Revenue Code already filed in court cannot be compromised a. Both statements are true b. Both statements are false c. Only Statement 1 is true d. Only Statement 2 is true 32. To safeguard the interest of the Government, the Commissioner, in his opinion, may place under constructive distraint the property of a delinquent taxpayer in the following cases, EXCEPT: a. The taxpayer is retiring from any business subject to tax b. The taxpayer intends to leave the Philippines c. The taxpayer performs any act tending to obstruct the proceedings for collecting the tax due or which may be due from him d. The period of assessment is about to expire 33. In case there is no bidder for real property exposed for foreclosure sale or if the highest bid is for an amount insufficient to pay the taxes, penalties and costs, the remedy of the Commissioner for the purpose of collecting the deficiency tax is a. Distraint c. Forfeiture b. Levy d. Resale 34. The running of the Statute of Limitations provided in Sections 203 and 222 of the NIRC on the making of assessment and the beginning of distraint or levy a proceeding in court for collection, in respect of any deficiency, shall be suspended on the following instances, EXCEPT: a. taxpayer requests for a motion for reinvestigation which is granted by the Commissioner b. taxpayer requests for a motion for reconsideration which is granted by the Commissioner c. taxpayer cannot be located in the address given by him in the return filed upon which a tax is being assessed or collected d. when the warrant of distraint or levy is duly served upon the taxpayer 35. Statement 1: The Court of Tax Appeals has an exclusive original jurisdiction to review the inaction by the Commissioner of Internal Revenue (CIR) in cases involving disputed assessments, refunds of Tax Remedies, CTA Jurisdiction, and Local Taxation internal revenue taxes, fees or other charges, penalties in relations thereto, or other matters arising under the National Internal Revenue Code or other laws administered by the Bureau of Internal Revenue. Statement 2: Based on the preceding paragraph, the inaction of the CIR shall be deemed a denial. a. Both statements are true b. Both statements are false c. Only Statement 1 is true d. Only Statement 2 is true 36. Statement 1: The taxpayers shall be informed in writing of the law and the facts on which the assessment is made; otherwise, the assessment shall be void Statement 2: If the protest is denied in whole or in part, or is not acted upon within one hundred twenty (120) days from submission of documents, the taxpayer adversely affected by the decision or inaction may appeal to the Court of Tax Appeals within thirty (30) days from receipt of the said decision, or from the lapse of one hundred twenty (120)-day period a. Both statements are true b. Both statements are false c. Only Statement 1 is true d. Only Statement 2 is true 37. Pre-assessment notice shall not be required in the following cases, EXCEPT: a. When the finding for any deficiency tax is the result of mathematical error in the computation of the tax as appearing on the face of the return b. When a discrepancy has been determined between the tax withheld and the amount actually remitted by the withholding agent c. When a taxpayer who opted to claim a refund or tax credit of excess creditable withholding tax for a taxable period was determined to have carried over and automatically applied the same amount claimed against the estimated tax liabilities for the taxable quarter or quarters of the succeeding taxable year d. When the income tax due on excisable articles has not been paid 38. Statement 1: The Court of Tax Appeals has an exclusive appellate jurisdiction to review decisions, orders or resolutions of the Regional Trial Courts in local tax cases originally decided or resolved by them in the exercise of their original or appellate jurisdiction Statement 2: The Court of Tax Appeals has an exclusive original jurisdiction to review Decisions of the Commissioner of Customs in cases involving liability for customs duties, fees or other money charges, seizure, detention or release of property affected, fines, forfeitures or other penalties in relation thereto, or other matters arising under the Customs Law or other laws administered by the Bureau of Customs a. Both statements are true b. Both statements are false c. Only Statement 1 is true d. Only Statement 2 is true 39. Statement 1: The Court of Tax Appeals has an exclusive appellate jurisdiction to review Decisions of the Central Board of Assessment Appeals in the exercise of its appellate jurisdiction over cases involving the assessment and taxation of real property originally decided by the provincial or city board of assessment appeals Statement 2: The Court of Tax Appeals has an exclusive appellate jurisdiction to review the decisions of the Secretary of Finance on customs cases elevated to him automatically for review from decisions of the Commissioner of Customs which are adverse to the Government a. Both statements are true b. Both statements are false c. Only Statement 1 is true d. Only Statement 2 is true Tax Remedies, CTA Jurisdiction, and Local Taxation 31. Statement 1: All criminal violations of the National Internal Revenue Code may be compromised Statement 2: A criminal case for violations of the National Internal Revenue Code already filed in court cannot be compromised a. Both statements are true b. Both statements are false c. Only Statement 1 is true d. Only Statement 2 is true 32. To safeguard the interest of the Government, the Commissioner, in his opinion, may place under constructive distraint the property of a delinquent taxpayer in the following cases, EXCEPT: a. The taxpayer is retiring from any business subject to tax b. The taxpayer intends to leave the Philippines c. The taxpayer performs any act tending to obstruct the proceedings for collecting the tax due or which may be due from him d. The period of assessment is about to expire 33. In case there is no bidder for real property exposed for foreclosure sale or if the highest bid is for an amount insufficient to pay the taxes, penalties and costs, the remedy of the Commissioner for the purpose of collecting the deficiency tax is a. Distraint c. Forfeiture b. Levy d. Resale 34. The running of the Statute of Limitations provided in Sections 203 and 222 of the NIRC on the making of assessment and the beginning of distraint or levy a proceeding in court for collection, in respect of any deficiency, shall be suspended on the following instances, EXCEPT: a. taxpayer requests for a motion for reinvestigation which is granted by the Commissioner b. taxpayer requests for a motion for reconsideration which is granted by the Commissioner c. taxpayer cannot be located in the address given by him in the return filed upon which a tax is being assessed or collected d. when the warrant of distraint or levy is duly served upon the taxpayer 35. Statement 1: The Court of Tax Appeals has an exclusive original jurisdiction to review the inaction by the Commissioner of Internal Revenue (CIR) in cases involving disputed assessments, refunds of Tax Remedies, CTA Jurisdiction, and Local Taxation internal revenue taxes, fees or other charges, penalties in relations thereto, or other matters arising under the National Internal Revenue Code or other laws administered by the Bureau of Internal Revenue. Statement 2: Based on the preceding paragraph, the inaction of the CIR shall be deemed a denial. a. Both statements are true b. Both statements are false c. Only Statement 1 is true d. Only Statement 2 is true 36. Statement 1: The taxpayers shall be informed in writing of the law and the facts on which the assessment is made; otherwise, the assessment shall be void Statement 2: If the protest is denied in whole or in part, or is not acted upon within one hundred twenty (120) days from submission of documents, the taxpayer adversely affected by the decision or inaction may appeal to the Court of Tax Appeals within thirty (30) days from receipt of the said decision, or from the lapse of one hundred twenty (120)-day period a. Both statements are true b. Both statements are false c. Only Statement 1 is true d. Only Statement 2 is true 37. Pre-assessment notice shall not be required in the following cases, EXCEPT: a. When the finding for any deficiency tax is the result of mathematical error in the computation of the tax as appearing on the face of the return b. When a discrepancy has been determined between the tax withheld and the amount actually remitted by the withholding agent c. When a taxpayer who opted to claim a refund or tax credit of excess creditable withholding tax for a taxable period was determined to have carried over and automatically applied the same amount claimed against the estimated tax liabilities for the taxable quarter or quarters of the succeeding taxable year d. When the income tax due on excisable articles has not been paid 38. Statement 1: The Court of Tax Appeals has an exclusive appellate jurisdiction to review decisions, orders or resolutions of the Regional Trial Courts in local tax cases originally decided or resolved by them in the exercise of their original or appellate jurisdiction Statement 2: The Court of Tax Appeals has an exclusive original jurisdiction to review Decisions of the Commissioner of Customs in cases involving liability for customs duties, fees or other money charges, seizure, detention or release of property affected, fines, forfeitures or other penalties in relation thereto, or other matters arising under the Customs Law or other laws administered by the Bureau of Customs a. Both statements are true b. Both statements are false c. Only Statement 1 is true d. Only Statement 2 is true 39. Statement 1: The Court of Tax Appeals has an exclusive appellate jurisdiction to review Decisions of the Central Board of Assessment Appeals in the exercise of its appellate jurisdiction over cases involving the assessment and taxation of real property originally decided by the provincial or city board of assessment appeals Statement 2: The Court of Tax Appeals has an exclusive appellate jurisdiction to review the decisions of the Secretary of Finance on customs cases elevated to him automatically for review from decisions of the Commissioner of Customs which are adverse to the Government a. Both statements are true b. Both statements are false c. Only Statement 1 is true d. Only Statement 2 is true Tax Remedies, CTA Jurisdiction, and Local Taxation

Expert Answer:

Answer rating: 100% (QA)

Certainly Here are the answers with explanations 31 d Only Statement 2 is true Explanation Statement 1 is false because not all criminal violations of the National Internal Revenue Code may be comprom... View the full answer

Related Book For

Income Tax Fundamentals 2013

ISBN: 9781285586618

31st Edition

Authors: Gerald E. Whittenburg, Martha Altus Buller, Steven L Gill

Posted Date:

Students also viewed these law questions

-

The Crazy Eddie fraud may appear smaller and gentler than the massive billion-dollar frauds exposed in recent times, such as Bernie Madoffs Ponzi scheme, frauds in the subprime mortgage market, the...

-

The company of choice is APPLE INC (AAPL). Brief description of the company (one paragraph, briefly summarizing the companys business) Company history (origin, major developments, etc.) Organization...

-

A satellite circles the earth in an orbit whose radius is twice the earth's radius. The earth's mass is 5.98 1024 kg, and its radius is 6.38 106 m. What is the period of the satellite?

-

Which of these levels of conflict refers to the internal conflict or annoyance of a human being has? Functional conflict Dysfunctional conflict Interpersonal conflict Intrapersonal conflict

-

A 2-kg block resting on a low-friction floor is subjected to the time-dependent force \(F(t)=0.5 t^{2}\). The block starts out \(1.0 \mathrm{~m}\) away from the origin. (a) What is speed of the...

-

Formulate the Krampf Lines Railway Company situation (Problem 9-17) as a linear program and solve using computer software.

-

You plan to deploy a dockerized application in an AWS ECS cluster. The application needs access to an S 3 bucket to read files. The ECS containers should have the AmazonS 3 ReadOnlyAccess permission....

-

Select one or more of the following modern items or devices and conduct an Internet search in order to determine what specific material(s) is (are) used and what specific properties this (these)...

-

What are Document existing and developing threats related to Artificial Intelligence. Which one are you the most concerned about and why?

-

How would you manage the unexpected work demands using technology? Develop a work plan for the unexpected work demands of your workplace.

-

Explain global economic integration and give examples. Contrast international strategies for entering foreign markets versus domestic markets. Explain deeply with proper real life example

-

How do you think business owners deal with this in their contracts?

-

There are certain elements that has to be proved before the plaintiff can recover in a Negligence lawsuit. What are the elements?

-

a) Draw the free body diagram of each link and show all forces acting on the links b) Using analytical solution method, determine the reaction forces at the joints and the torque applied to input...

-

Which provision could best be justified as encouraging small business? a. Ordinary loss allowed on $ 1244 stuck. b. Percentage depletion. c. Domestic production activates deductions. d. Interest...

-

Tom has a successful business with $100,000 of income in 2012. He purchases one new asset in 2012, a new machine which is 7-year MACRS property and costs $25,000. If you are Tom's tax advisor, how...

-

Linda and Richard are married and file a joint return for 2012. During the year, Linda, who works as an accountant for a national airline, used $2,100 worth of free passes for travel on the airline;...

-

For each of the following cases, indicate the filing status for the taxpayer(s) for 2012 using the following legend: A - Single B - Married, filing a joint return C - Married, filing separate returns...

-

Show that the relations (14.23) follow from Eqs. (14.21) and (14.22). Data from Eq. 14.21 Data from Eq. 14.22 Data from Eq. 14.23 VR (P) = E+m+o.p VR (0) 2m(E+m)

-

Verify that the Pauli-Dirac representation (14.43) satisfies Eq. (14.27). Data from Eq. 14.27 Data from Eq. 14.43 {,} = + = 2

-

Verify the projection characteristics implied by equations (14.51). Data from Eq.14.51 2 In = (s + I) Da 1- 24(1-y's) = UR

Study smarter with the SolutionInn App