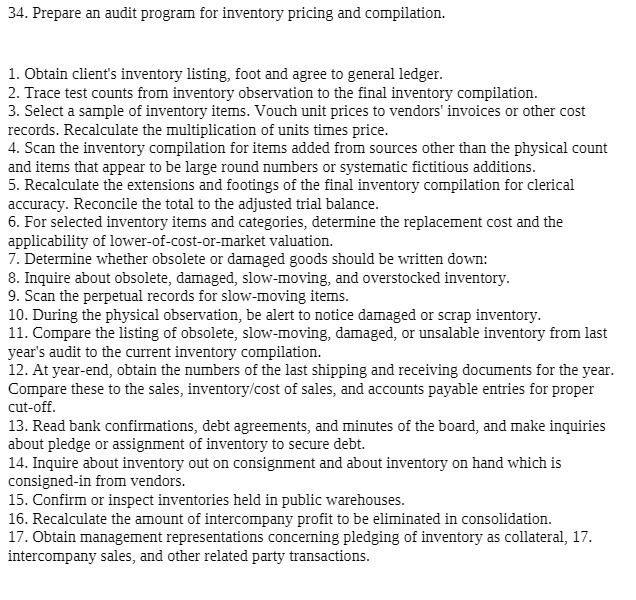

34. Prepare an audit program for inventory pricing and compilation. 1. Obtain client's inventory listing, foot...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

Posted Date: