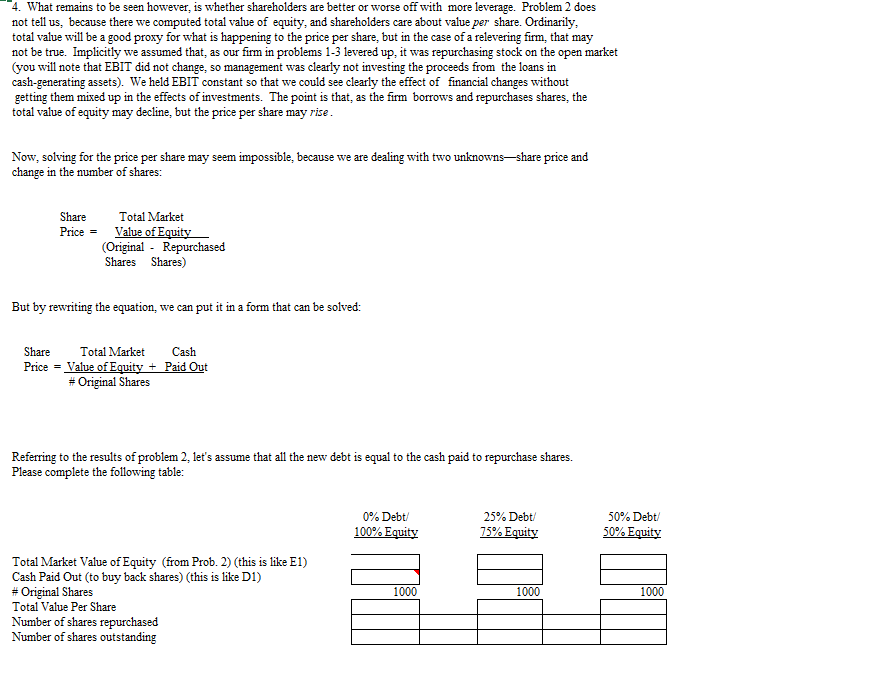

4. What remains to be seen however, is whether shareholders are better or worse off with...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

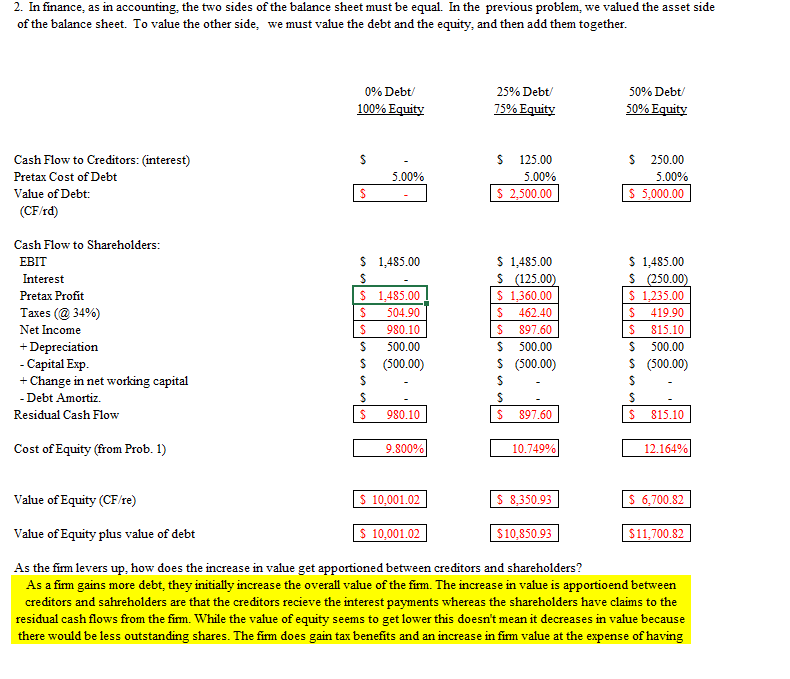

4. What remains to be seen however, is whether shareholders are better or worse off with more leverage. Problem 2 does not tell us, because there we computed total value of equity, and shareholders care about value per share. Ordinarily, total value will be a good proxy for what is happening to the price per share, but in the case of a relevering firm, that may not be true. Implicitly we assumed that, as our firm in problems 1-3 levered up, it was repurchasing stock on the open market (you will note that EBIT did not change, so management was clearly not investing the proceeds from the loans in cash-generating assets). We held EBIT constant so that we could see clearly the effect of financial changes without getting them mixed up in the effects of investments. The point is that, as the firm borrows and repurchases shares, the total value of equity may decline, but the price per share may rise. Now, solving for the price per share may seem impossible, because we are dealing with two unknowns-share price and change in the number of shares: Share Price = Total Market Value of Equity (Original - Repurchased Shares Shares) But by rewriting the equation, we can put it in a form that can be solved: Share Total Market Cash Price = Value of Equity + Paid Out # Original Shares Referring to the results of problem 2, let's assume that all the new debt is equal to the cash paid to repurchase shares. Please complete the following table: Total Market Value of Equity (from Prob. 2) (this is like E1) Cash Paid Out (to buy back shares) (this is like D1) # Original Shares Total Value Per Share Number of shares repurchased Number of shares outstanding 0% Debt/ 100% Equity 1000 25% Debt/ 75% Equity 1000 50% Debt/ 50% Equity 1000 2. In finance, as in accounting, the two sides of the balance sheet must be equal. In the previous problem, we valued the asset side of the balance sheet. To value the other side, we must value the debt and the equity, and then add them together. Cash Flow to Creditors: (interest) Pretax Cost of Debt Value of Debt: (CF/rd) Cash Flow to Shareholders: EBIT Interest Pretax Profit Taxes (@34%) Net Income + Depreciation - Capital Exp. + Change in net working capital -Debt Amortiz. Residual Cash Flow Cost of Equity (from Prob. 1) 0% Debt/ 100% Equity S $ $ 1,485.00 S $ $ $ S 5.00% S S S $ 1,485.00 504.90 980.10 500.00 (500.00) 980.10 9.800% $ 10,001.02 25% Debt/ 75% Equity $ 10,001.02 $ 125.00 5.00% $ 2,500.00 $ 1,485.00 $ (125.00) $ 1,360.00 $ 462.40 897.60 500.00 $ $ $ S S $ (500.00) 897.60 10.749% $ 8,350.93 50% Debt/ 50% Equity $10,850.93 $ 250.00 5.00% $ 5,000.00 Value of Equity (CF/re) Value of Equity plus value of debt As the firm levers up, how does the increase in value get apportioned between creditors and shareholders? As a firm gains more debt, they initially increase the overall value of the firm. The increase in value is apportioend between creditors and sahreholders are that the creditors recieve the interest payments whereas the shareholders have claims to the residual cash flows from the firm. While the value of equity seems to get lower this doesn't mean it decreases in value because there would be less outstanding shares. The firm does gain tax benefits and an increase in firm value at the expense of having $ 1,485.00 $ (250.00) $ 1,235.00 S 419.90 $ 815.10 500.00 $ (500.00) S S $ 815.10 12.164% $ 6,700.82 $11,700.82 4. What remains to be seen however, is whether shareholders are better or worse off with more leverage. Problem 2 does not tell us, because there we computed total value of equity, and shareholders care about value per share. Ordinarily, total value will be a good proxy for what is happening to the price per share, but in the case of a relevering firm, that may not be true. Implicitly we assumed that, as our firm in problems 1-3 levered up, it was repurchasing stock on the open market (you will note that EBIT did not change, so management was clearly not investing the proceeds from the loans in cash-generating assets). We held EBIT constant so that we could see clearly the effect of financial changes without getting them mixed up in the effects of investments. The point is that, as the firm borrows and repurchases shares, the total value of equity may decline, but the price per share may rise. Now, solving for the price per share may seem impossible, because we are dealing with two unknowns-share price and change in the number of shares: Share Price = Total Market Value of Equity (Original - Repurchased Shares Shares) But by rewriting the equation, we can put it in a form that can be solved: Share Total Market Cash Price = Value of Equity + Paid Out # Original Shares Referring to the results of problem 2, let's assume that all the new debt is equal to the cash paid to repurchase shares. Please complete the following table: Total Market Value of Equity (from Prob. 2) (this is like E1) Cash Paid Out (to buy back shares) (this is like D1) # Original Shares Total Value Per Share Number of shares repurchased Number of shares outstanding 0% Debt/ 100% Equity 1000 25% Debt/ 75% Equity 1000 50% Debt/ 50% Equity 1000 2. In finance, as in accounting, the two sides of the balance sheet must be equal. In the previous problem, we valued the asset side of the balance sheet. To value the other side, we must value the debt and the equity, and then add them together. Cash Flow to Creditors: (interest) Pretax Cost of Debt Value of Debt: (CF/rd) Cash Flow to Shareholders: EBIT Interest Pretax Profit Taxes (@34%) Net Income + Depreciation - Capital Exp. + Change in net working capital -Debt Amortiz. Residual Cash Flow Cost of Equity (from Prob. 1) 0% Debt/ 100% Equity S $ $ 1,485.00 S $ $ $ S 5.00% S S S $ 1,485.00 504.90 980.10 500.00 (500.00) 980.10 9.800% $ 10,001.02 25% Debt/ 75% Equity $ 10,001.02 $ 125.00 5.00% $ 2,500.00 $ 1,485.00 $ (125.00) $ 1,360.00 $ 462.40 897.60 500.00 $ $ $ S S $ (500.00) 897.60 10.749% $ 8,350.93 50% Debt/ 50% Equity $10,850.93 $ 250.00 5.00% $ 5,000.00 Value of Equity (CF/re) Value of Equity plus value of debt As the firm levers up, how does the increase in value get apportioned between creditors and shareholders? As a firm gains more debt, they initially increase the overall value of the firm. The increase in value is apportioend between creditors and sahreholders are that the creditors recieve the interest payments whereas the shareholders have claims to the residual cash flows from the firm. While the value of equity seems to get lower this doesn't mean it decreases in value because there would be less outstanding shares. The firm does gain tax benefits and an increase in firm value at the expense of having $ 1,485.00 $ (250.00) $ 1,235.00 S 419.90 $ 815.10 500.00 $ (500.00) S S $ 815.10 12.164% $ 6,700.82 $11,700.82

Expert Answer:

Answer rating: 100% (QA)

Based on the table provided we can observe the following 0 Debt100 Equity Total Market Value of Equi... View the full answer

Related Book For

Posted Date:

Students also viewed these finance questions

-

Read the case study "Southwest Airlines," found in Part 2 of your textbook. Review the "Guide to Case Analysis" found on pp. CA1 - CA11 of your textbook. (This guide follows the last case in the...

-

The Crazy Eddie fraud may appear smaller and gentler than the massive billion-dollar frauds exposed in recent times, such as Bernie Madoffs Ponzi scheme, frauds in the subprime mortgage market, the...

-

The data below provides weekly sales for the past 12 weeks (weeks 21-32). Week Sales 21 4,000 22 3,655 23 3,958 24 3,983 25 4,538 26 4,120 27 4,692 28 4,421 29 4,859 30 5,030 31 5,540 32 5,670 Use a...

-

Supply and Demand in the Cell Phone Market. (Make sure to include a graph with the initial equilibrium price and quantity and the new price and quantity as well as an explanation to support your...

-

Explain the differences in the boiling points between the members of each of these pairs of compounds: (a) CH 3 (CH 2 )6 CH3 bp: 126C CH3 (CH2)8 CH3 bp: 174C (b) CH3CH2CH2OH bp: 97C CH3CH2OCH3 bp:...

-

Forced circulation boiler is: (a) La-Mont boiler (b) Benson boiler (b) Loeffler boiler (d) All of the above

-

An experiment was conducted on a new model of a particular make of an automobile to determine the stopping distance at various speeds. The following data were recorded. (a) Fit a multiple regression...

-

Differentiate between accelerator principle of investment and investment multiplier. Explain the determinants of induced investment in an economy. Given C=a+bY, explain "a" and "b" and then sketch...

-

Most air travellers now use e-tickets. Electronic ticketing allows passengers to not worry about a paper ticket, and it costs the airline companies less than paper ticketing. However, recently the...

-

What is prepare adjusting journal entry for the change in accounting policy. Including credit and debit trasaction. What ever is given in the solution of part ( b ) is right. Rest of the blanks need...

-

The Mini-Triangle source program below contains several contextual errors. Show how contextual analysis will detect these errors. let in var a: Integer; var b: Boolean; var i: Logical; if i then bi =...

-

4. According to th 4. According to the savings-investment spending identity in an economy open to capital flows from and to abroad, the following must hold: I = Private savings + Budget bal- ance +...

-

I. a) What are the components of the transformed stiffness matrix [C] for an orthotropic material in a coordinate system rotated 90 about the 1-axis? Express your answer in terms of the original...

-

Multiply and simplify: -3x2(x+2x-5)

-

Scenario Details The Automated Parcel Delivery company is examining a proposal to provide a drone parcel delivery service for supermarkets across the Perth Metropolitan area. It will operate the...

-

Making use of the tables of atomic masses, find the velocity with which the products of the reaction B10 (n, ) Li7 come apart; the reaction proceeds via interaction of very slow neutrons with...

-

Suppose that Al Deardwarf from the last problem cannot vary the amount of wood that he uses in the short run and is stuck with using 20 units of wood. Suppose that he can change the amount of plastic...

-

Vanna Boogie likes to have large parties. She also has a strong preference for having exactly as many men as women at her parties. In fact, Vannas preferences among parties can be represented by the...

-

In Gomorrah, New Jersey, there is only one newspaper, the Daily Calumny. The demand for the paper depends on the price and the amount of scandal reported. The demand function is Q = 15S1/2P3, where Q...

-

A second-order dynamic system is modeled as \[9 \ddot{x}+6 \dot{x}+\frac{10}{9} x=14 \delta(t), \quad x(0)=0, \quad \dot{x}(0)=-\frac{1}{4}\] a. Find the response \(x(t)\) in closed form. b. Plot the...

-

Consider a first-order system with time constant \(\tau\) and zero initial condition. Find the system's unit-step response for \(\tau=\frac{1}{3}\) and \(\frac{2}{3}\), plot the two curves versus \(0...

-

a. Identify the damping type and find the free response. b. Plot the free response by using the initial command. \(\ddot{x}+3 \dot{x}+4 x=0, \quad x(0)=\frac{2}{5}, \quad \dot{x}(0)=0\)

Study smarter with the SolutionInn App