6 Review the minutes of the board of directors and committee meetings for the year and...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

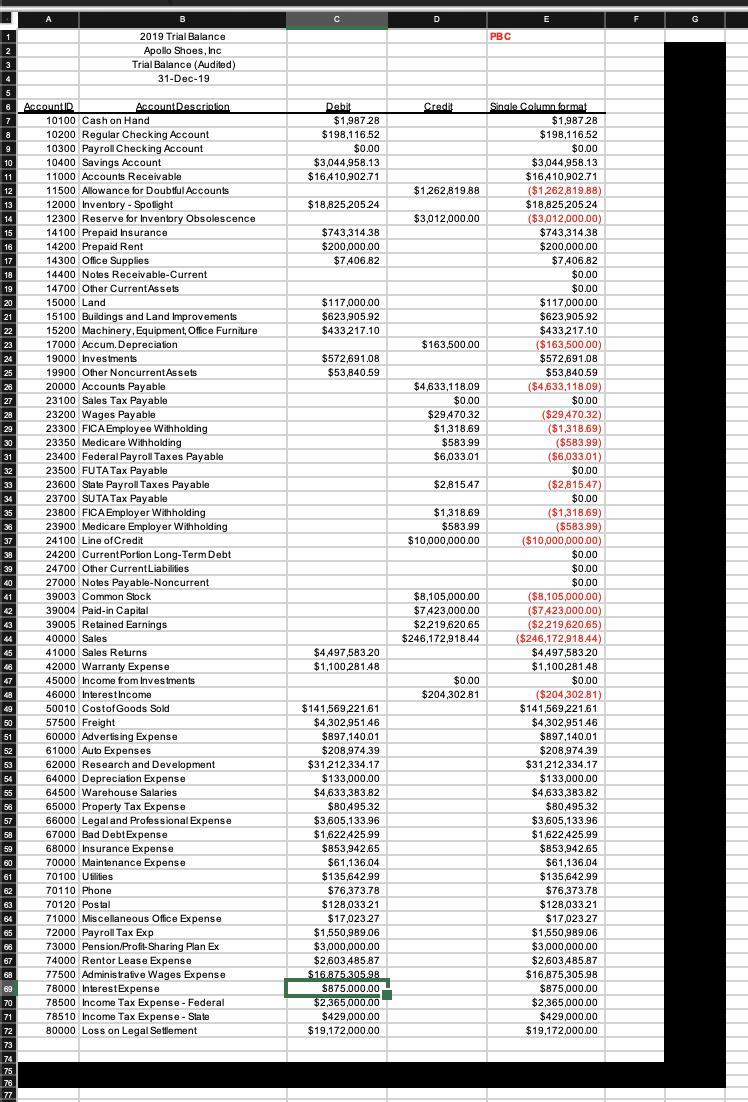

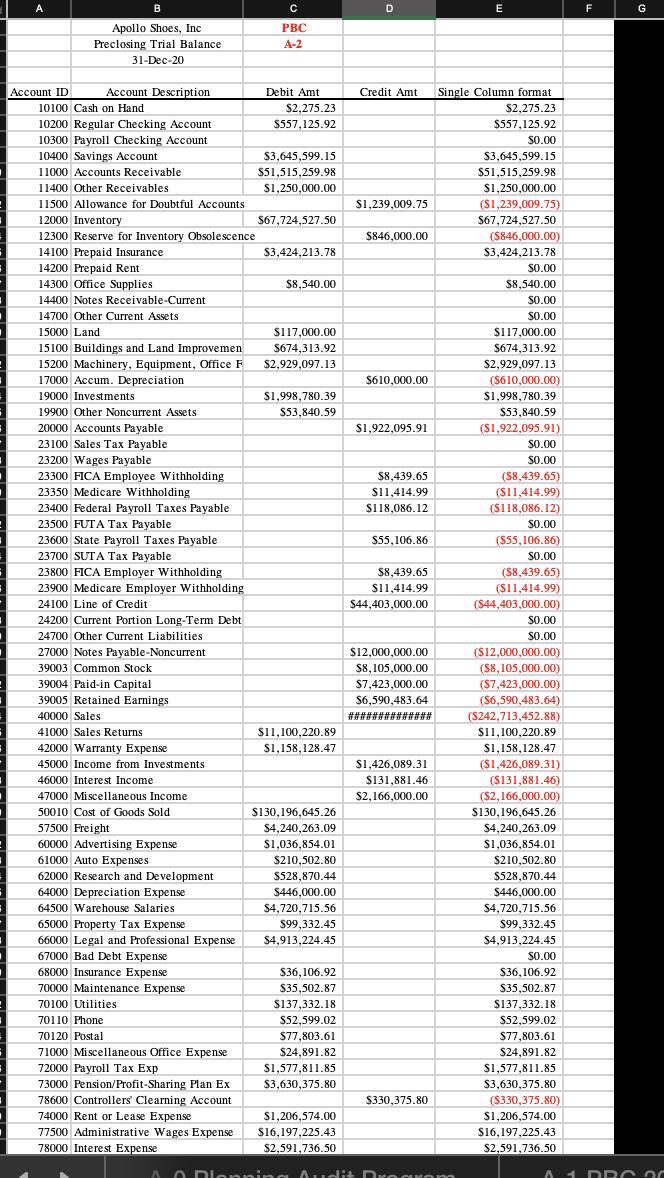

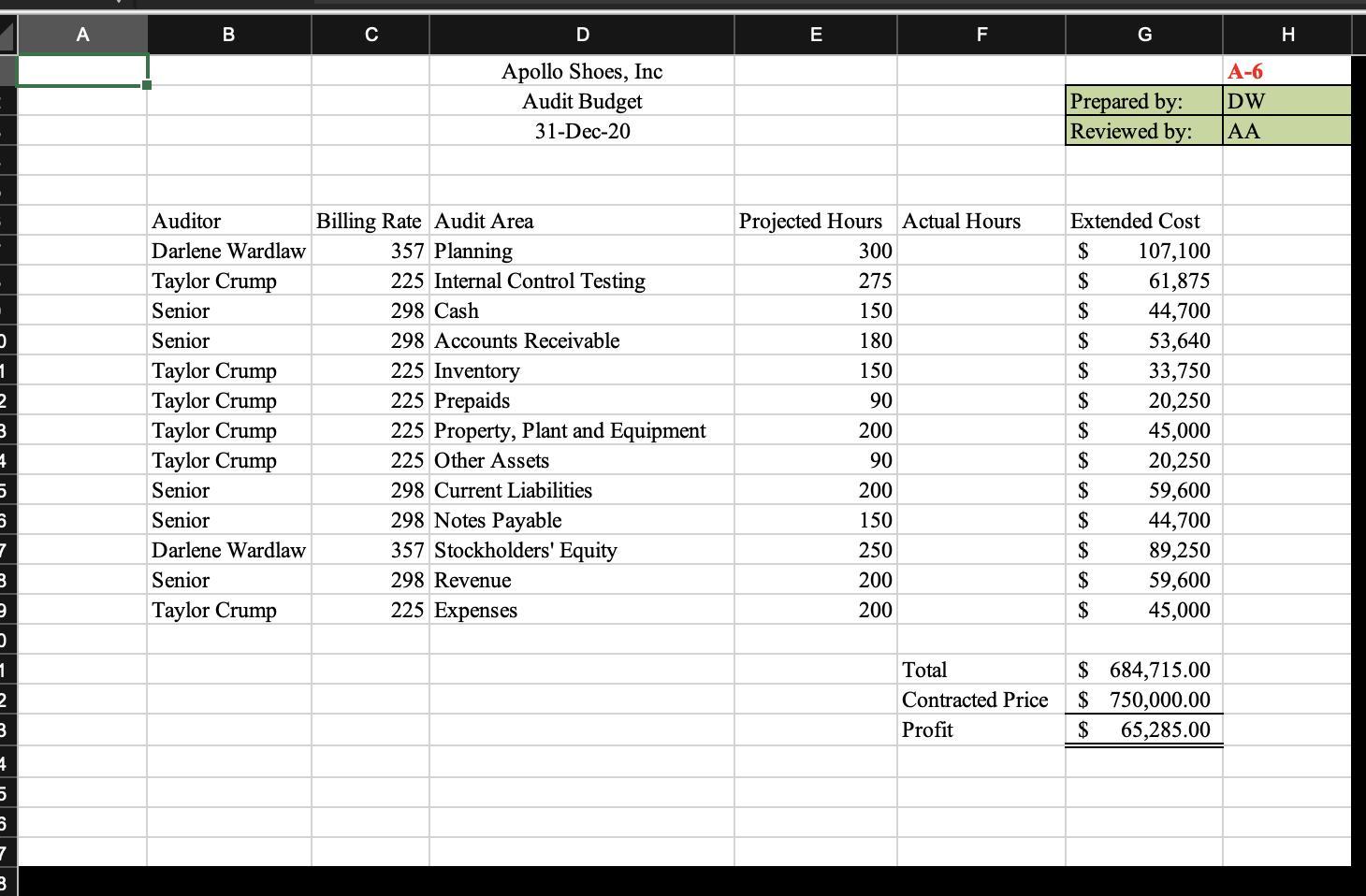

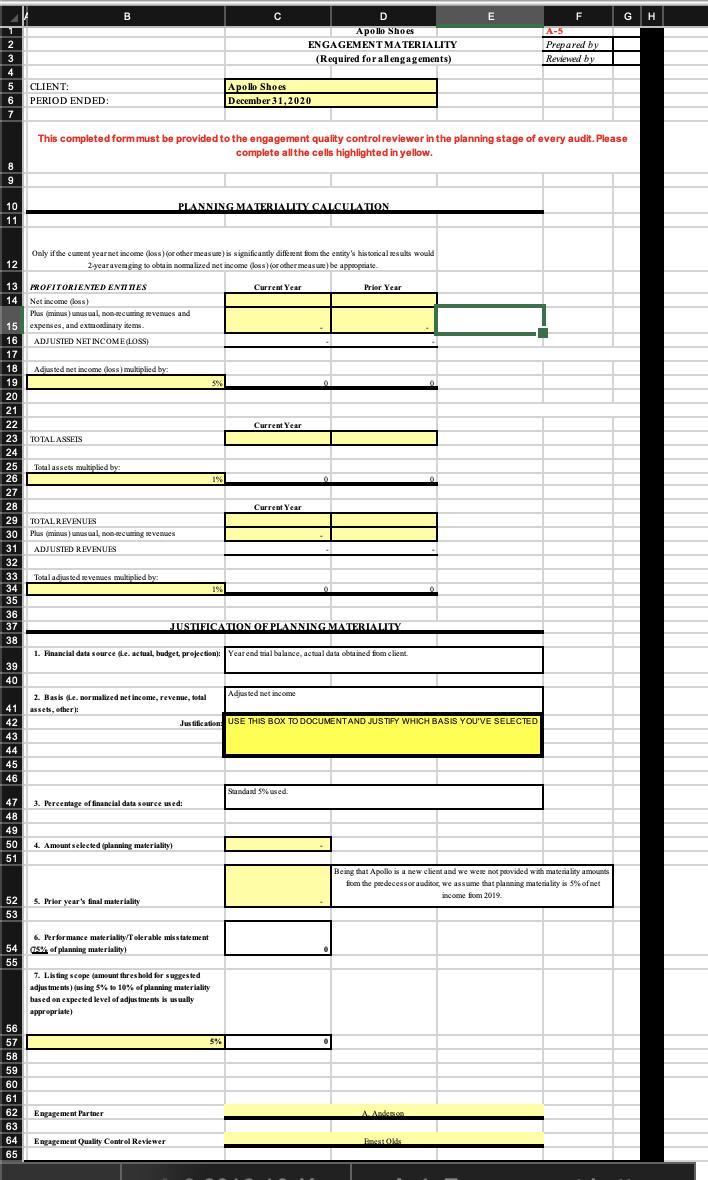

6 Review the minutes of the board of directors and committee meetings for the year and any new agreements, leases, contracts, or other important documents. Obtain copies of the minutes or agreements for the current or permanent workpaper files. Highlight matters relevant to the related audit area or for which disclosure will be required in the financial statement or notes A-3 TC Notes on A-3. 1 2 3 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 48 49 50 51 52 53 54 55 56 57 58 59 60 61 62 63 64 65 66 67 68 69 70 71 72 73 74 75 76 77 A Account ID B 2019 Trial Balance Apollo Shoes, Inc. Trial Balance (Audited) 31-Dec-19 Account Description 10100 Cash on Hand 10200 Regular Checking Account 10300 Payroll Checking Account 10400 Savings Account 11000 Accounts Receivable. 11500 Allowance for Doubtful Accounts 12000 Inventory - Spotlight 12300 Reserve for Inventory Obsolescence 14100 Prepaid Insurance 14200 Prepaid Rent 14300 Office Supplies 14400 Notes Receivable-Current 14700 Other Current Assets 15000 Land 15100 Buildings and Land Improvements. 15200 Machinery, Equipment, Office Furniture 17000 Accum. Depreciation 19000 Investments 19900 Other Noncurrent Assets 20000 Accounts Payable 23100 Sales Tax Payable 23200 Wages Payable 23300 FICA Employee Withholding 23350 Medicare Withholding 23400 Federal Payroll Taxes Payable 23500 FUTA Tax Payable 23600 State Payroll Taxes Payable 23700 SUTA Tax Payable 23800 FICA Employer Withholding 23900 Medicare Employer Withholding 24100 Line of Credit 24200 Current Portion Long-Term Debt 24700 Other Current Liabilities 27000 Notes Payable-Noncurrent 39003 Common Stock 39004 Paid-in Capital 39005 Retained Earnings 40000 Sales 41000 Sales Returns 42000 Warranty Expense 45000 Income from Investments 46000 Interest Income 50010 Costof Goods Sold 57500 Freight 60000 Advertising Expense 61000 Auto Expenses 62000 Research and Development 64000 Depreciation Expense 64500 Warehouse Salaries 65000 Property Tax Expense 66000 Legal and Professional Expense 67000 Bad Debt Expense 68000 Insurance Expense 70000 Maintenance Expense 70100 Utilities 70110 Phone 70120 Postal 71000 Miscellaneous Office Expense 72000 Payroll Tax Exp 73000 Pension/Profit-Sharing Plan Ex 74000 Rentor Lease Expense 77500 Administrative Wages Expense 78000 Interest Expense 78500 Income Tax Expense - Federal 78510 Income Tax Expense - State 80000 Loss on Legal Setlement C Debit $1,987.28 $198.116.52 $0.00 $3,044,958.13 $16,410,902.71 $18,825,205.24 $743,314.38 $200,000.00 $7.406.82 $117,000.00 $623,905.92 $433,217.10 $572,691.08 $53,840.59 $4,497,583.20 $1,100,281.48 $141,569,221.61 $4,302,95146 $897,140.01 $208,974.39 $31,212,334.17 $133,000.00 $4,633,383.82 $80,495.32 $3,605,133.96 $1,622,425.99 $853,942.65 $61,136.04 $135.642.99 $76,373.78 $128,033.21 $17,023.27 $1,550,989.06 $3,000,000.00 $2.603,485.87 $16.875.305.98 $875.000.00 $2,365,000.00 $429,000.00 $19,172,000.00 D Credit $1,262,819.88 $3,012,000.00 $163,500.00 $4,633,118.09 $0.00 $29,470.32 $1,318.69 $583.99 $6,033.01 $2,815.47 $1,318.69 $583.99 $10,000,000.00 $8,105,000.00 $7423,000.00 $2,219,620.65 $246,172,918.44 $0.00 $204,302.81 PBC E Single Column format $1,987.28 $198,116.52 $0.00 $3,044,958.13 $16,410,902.71 ($1,262,819.88) $18,825,205.24 ($3,012,000.00) $743,314.38 $200,000.00 $7,406.82 $0.00 $0.00 $117,000.00 $623,905.92 $433,217.10 ($163,500.00) $572,691.08 $53,840.59 ($4,633,118.09) $0.00 ($29,470.32) ($1,318.69) ($583.99) ($6,033.01) $0.00 ($2,815.47) $0.00 ($1,318.69) ($583.99) ($10,000,000.00) $0.00 $0.00 $0.00 ($8,105,000.00) ($7423,000.00) ($2,219,620.65) ($246,172,918.44) $4,497,583.20 $1,100,28148 $0.00 ($204,302.81) $141,569,221.61 $4,302,951.46 $897,140.01 $208,974.39 $31,212,334.17 $133,000.00 $4,633,383.82 $80,495.32 $3,605,133.96 $1,622,425.99 $853,942.65 $61,136.04 $135,642.99 $76,373.78 $128,033.21 $17,023.27 $1,550,989.06 $3,000,000.00 $2,603,485.87 $16,875,305.98 $875,000.00 $2,365,000.00 $429,000.00 $19,172,000.00 F G 1 Account ID B Apollo Shoes, Inc Preclosing Trial Balance: 31-Dec-20 Account Description. 10100 Cash on Hand 10200 Regular Checking Account 10300 Payroll Checking Account 10400 Savings Account 11000 Accounts Receivable 11400 Other Receivables 11500 Allowance for Doubtful Accounts. conomnog 12000 Inventory 12300 Reserve for Inventory Obsolescence 14100 Prepaid Insurance pro doparg 14200 Prepaid Rent. Expan 14300 Office Supplies *** St 14400 Notes Receivable-Current www 14700 Other Current Assets *600* 15000 Land ********** 15100 Buildings and Land Improvemen 15200 Machinery, Equipment, Office F 1000 17000 Accum. Depreciation wwwww 19000 Investments 19900 Other Noncurrent Assets * 20000 Accounts Payable *** mater 23100 Sales Tax Payable 53000 23200 Wages Payable 23300 FICA Employee Withholding 23350 Medicare Withholding 23400 Federal Payroll Taxes Payable 23500 FUTA Tax Payable 23600 State Payroll Taxes Payable 23700 SUTA Tax Payable 23800 FICA Employer Withholding 23900 Medicare Emplover Withholding 24100 Line of Credit 24200 Current Portion Long-Term Debt 24200 Current Portion 24700 Other Current Liabilities 27000 Notes Payable-Noncurrent 39003 Common Stock 39004 Paid-in Capital 39005 35009 Retained Earnings 40000 Sales 40000 Sales 41000 Sales Returns 71000 Sales 42000 Warranty Expense 45000 Income from Investments 46000 Interest Income 10000 47000 Miscellaneous Income 50010 Cost of Goods Sold 30010 COST OF 57500 Freight 60000 Advertising Expense 61000 Auto Expenses 62000 Research and Development www 64000 Depreciation Expense 64500 Warehouse Salaries 65000 Property Tax Expense supe 66000 Legal and Professional Expense Groning and Ad 67000 Bad Debt Expense CORPO 68000 Insurance Expense www. 70000 Maintenance Expense www 70100 Utilities. wwwww conte 70110 Phone 70120 Postal on 16 71000 Miscellaneous Office Expense 72000 Payroll Tax Exp. www 73000 Pension/Profit-Sharing Plan Ex 78600 Controllers' Clearning Account 74000 Rent or Lease Expense 77500 Administrative Wages Expense 78000 Interest Expense с PBC A-2 Debit Amt $2,275.23 $557,125.92 $3,645,599.15 $51,515,259.98 $1,250,000.00 $67,724,527.50 $3,424,213.78 $8,540.00 $117,000.00 $674,313.92 $2,929,097.13 $1,998,780.39 $53,840.59 $11,100,220.89 $1,158,128.47 $130,196,645.26 $4,240,263.09 $1,036,854.01 $210,502.80 $528,870.44 $446,000.00 $4,720,715.56 $99,332.45 $4,913,224.45 $36,106.92 $35,502.87 $137,332.18 $52,599.02 $77,803.61 $24,891.82 $1,577,811.85 $3.630.375.80 $1,206,574.00 $16,197.225.43 $2,591,736.50 D Credit Amt $1,239,009.75 $846,000.00 $610,000.00 $1,922,095.91 $8,439.65 $11,414.99 $118,086.12 $55,106.86 $8,439.65 $11,414.99 $44,403,000.00 $12,000,000.00 $8,105,000.00 $7,423,000.00 $6,590,483.64 ############## $1,426,089.31 $131,881.46 $2,166,000.00 $330,375.80 E Single Column format $2,275.23 $557,125.92 $0.00 O Planning Audit Drogrom $3,645,599.15 $51,515,259.98 $1,250,000.00 ($1,239,009.75) Cooperat $67,724,527.50 www.com ($846,000.00) 2015 20 $3,424,213.78 250.08 non Doku $0.00 www.we $8,540.00 Bronne $0.00 www.ne $0.00 www.www $117,000.00 2015.05 $674,313.92 CA $2,929,097.13 ($610,000.00) $1,998,780.39 400 $53,840.59 Coroa ($1,922,095.91) 20.00 $0.00 $0.00 ($8,439.65) ($11,414.99) ($118,086.12) $0.00 ($55,100.00 $0.00 ($8.439.0 ($11,414.99) ($44,403,000.00) ,000.00) $0.00 $0.00 ($12,000,000.00) 1.000.00 ($8,105.000.00) ($7,423,000.00) ($6,590,483.64) ($242,713,452.88) $11,100,220.89 $1,158,128.47 $1,156,126:47 ($1,426,089.31) ($131,881.46) ($2,166,000.00) $130,150,0.co $4,240,203.09 $1,036,854.01 $210.502.80 $210,502.80 $528,870.44 $446,000.00 $4,720,715.56 $99,332.45 $4,913,224.45 $0.00 826 10 $36,106.92 www. $35,502.87 ******** $137,332.18 AD FOR A $52,599.02 $77,803.61 RASPR $24,891.82 _ $1,577,811.85 $3,630,375.80 ($330,375.80) $1,206,574.00 $16,197,225.43 $2,591,736.50 F G A1 DRC 30 0 1 2 3 4 5 5 7 3 9 0 1 2 3 4 5 6 7 B A B Auditor Darlene Wardlaw Taylor Crump Senior Senior Taylor Crump Taylor Crump Crump Taylor Crump Senior Senior Darlene Wardlaw Senior Taylor Crump D Apollo Shoes, Inc Audit Budget 31-Dec-20 Billing Rate Audit Area 357 Planning 225 Internal Control Testing 298 Cash 298 Accounts Receivable 225 Inventory 225 Prepaids 225 Property, Plant and Equipment 225 Other Assets 298 Current Liabilities 298 Notes Payable 357 Stockholders' Equity 298 Revenue 225 Expenses E F Projected Hours Actual Hours 300 275 150 180 150 90 200 90 200 150 250 200 200 Total Contracted Price Profit Prepared by: Reviewed by: Extended Cost 107,100 61,875 44,700 53,640 33,750 20,250 45,000 20,250 59,600 44,700 89,250 59,600 45,000 $ $ $ $ $ $ $ $ $ $ $ $ $ $ 684,715.00 $ 750,000.00 $ 65,285.00 A-6 DW AA H 1 MASON 2 -2~~~~~~~~88588388588429494 49985 5 11 12 13 14 21 52 53 54 55 56 57 58 15 expenses, and extacadinary item ADJUSTED NET INCOME (LOSS) 59 60 CLIENT: PERIOD ENDED: 61 62 63 64 65 B PROFITORIENTED Net income (loss) Plus (minus) unusual, non-curring revenues and Adjusted net income (loss) multiplied by TOTAL ASSEIS Only if the curent year net income (loss) (or other measure) is significantly different from the entity's historical results would 2-year avenging to obtain normalized net income (loss) (or other measure) be appropriate. ENTITIES Total assets multiplied by: This completed form must be provided to the engagement quality control reviewer in the planning stage of every audit. Please complete all the cells highlighted in yellow. TOTAL REVENUES Plus (minus) usual, non-recurring revenues ADJUSTED REVENUES Total adjusted revenues multiplied by: 2. Basis (Le normalized net income, revenue, total assets, other): 4. Amount selected (planning materiality) 5. Prior year's final materiality PLANNING MATERIALITY CALCULATION 3. Percentage of financial data source used: Engagement Partner 6. Performance materiality/Tolerable misstatement 75% of planning materiality) Engagement Quality Control Reviewer 5% 7. Listing scope (amount threshold for suggested adjustments) (using 5% to 10% of planning materiality based on expected level of adjustments is usually appropriate) C 1% 1% Apollo Shoes December 31, 2020 1. Financial data source (Le. actual, budget, projection): Year end trial balance, actual data obtained from client. Current Year JUSTIFICATION OF PLANNING MATERIALITY 5% D Apollo Shoes ENGAGEMENT MATERIALITY (Required for all engagements) Current Year Current Year Adjusted net income 0 Justification: USE THIS BOX TO DOCUMENT AND JUSTIFY WHICH BASIS YOU'VE SELECTED Standard 5% used Prior Year ● E A Andenon F Emeat Olds A-5 Prepared by Reviewed by Being that Apollo is a new client and we were not provided with materiality amounts from the predecessor auditor, we assume that planning materiality is 5% of net income from 2019. G H Apollo Shoes, Inc. Audit Staffing Memo - A-7 December 31, 2020 A-7 Prepared by: DW Reviewed by: AA Based on the information reviewed in the Apollo Shoes 10-K, minutes of the board of directors, and other documents, I believe that the audit team will require the following specialized expertise: a. Special expertise in Apollo's business and products is probably not necessary. The products are ordinary shoes. The company gave no indication of dealing in complicated transactions such as rubber futures hedging. Auditors with general retail and wholesale experience ought to be able to cope with the expertise demands. b. The audit team will need some special expertise in several areas: (1) the tax personnel probably know how to prepare the state franchise tax return, and that expertise might not be very special, (2) auditors with SEC knowledge and experience will need to participate, and (3) the team will need people with computer expertise on the engagement. 6 Review the minutes of the board of directors and committee meetings for the year and any new agreements, leases, contracts, or other important documents. Obtain copies of the minutes or agreements for the current or permanent workpaper files. Highlight matters relevant to the related audit area or for which disclosure will be required in the financial statement or notes A-3 TC Notes on A-3. 1 2 3 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 48 49 50 51 52 53 54 55 56 57 58 59 60 61 62 63 64 65 66 67 68 69 70 71 72 73 74 75 76 77 A Account ID B 2019 Trial Balance Apollo Shoes, Inc. Trial Balance (Audited) 31-Dec-19 Account Description 10100 Cash on Hand 10200 Regular Checking Account 10300 Payroll Checking Account 10400 Savings Account 11000 Accounts Receivable. 11500 Allowance for Doubtful Accounts 12000 Inventory - Spotlight 12300 Reserve for Inventory Obsolescence 14100 Prepaid Insurance 14200 Prepaid Rent 14300 Office Supplies 14400 Notes Receivable-Current 14700 Other Current Assets 15000 Land 15100 Buildings and Land Improvements. 15200 Machinery, Equipment, Office Furniture 17000 Accum. Depreciation 19000 Investments 19900 Other Noncurrent Assets 20000 Accounts Payable 23100 Sales Tax Payable 23200 Wages Payable 23300 FICA Employee Withholding 23350 Medicare Withholding 23400 Federal Payroll Taxes Payable 23500 FUTA Tax Payable 23600 State Payroll Taxes Payable 23700 SUTA Tax Payable 23800 FICA Employer Withholding 23900 Medicare Employer Withholding 24100 Line of Credit 24200 Current Portion Long-Term Debt 24700 Other Current Liabilities 27000 Notes Payable-Noncurrent 39003 Common Stock 39004 Paid-in Capital 39005 Retained Earnings 40000 Sales 41000 Sales Returns 42000 Warranty Expense 45000 Income from Investments 46000 Interest Income 50010 Costof Goods Sold 57500 Freight 60000 Advertising Expense 61000 Auto Expenses 62000 Research and Development 64000 Depreciation Expense 64500 Warehouse Salaries 65000 Property Tax Expense 66000 Legal and Professional Expense 67000 Bad Debt Expense 68000 Insurance Expense 70000 Maintenance Expense 70100 Utilities 70110 Phone 70120 Postal 71000 Miscellaneous Office Expense 72000 Payroll Tax Exp 73000 Pension/Profit-Sharing Plan Ex 74000 Rentor Lease Expense 77500 Administrative Wages Expense 78000 Interest Expense 78500 Income Tax Expense - Federal 78510 Income Tax Expense - State 80000 Loss on Legal Setlement C Debit $1,987.28 $198.116.52 $0.00 $3,044,958.13 $16,410,902.71 $18,825,205.24 $743,314.38 $200,000.00 $7.406.82 $117,000.00 $623,905.92 $433,217.10 $572,691.08 $53,840.59 $4,497,583.20 $1,100,281.48 $141,569,221.61 $4,302,95146 $897,140.01 $208,974.39 $31,212,334.17 $133,000.00 $4,633,383.82 $80,495.32 $3,605,133.96 $1,622,425.99 $853,942.65 $61,136.04 $135.642.99 $76,373.78 $128,033.21 $17,023.27 $1,550,989.06 $3,000,000.00 $2.603,485.87 $16.875.305.98 $875.000.00 $2,365,000.00 $429,000.00 $19,172,000.00 D Credit $1,262,819.88 $3,012,000.00 $163,500.00 $4,633,118.09 $0.00 $29,470.32 $1,318.69 $583.99 $6,033.01 $2,815.47 $1,318.69 $583.99 $10,000,000.00 $8,105,000.00 $7423,000.00 $2,219,620.65 $246,172,918.44 $0.00 $204,302.81 PBC E Single Column format $1,987.28 $198,116.52 $0.00 $3,044,958.13 $16,410,902.71 ($1,262,819.88) $18,825,205.24 ($3,012,000.00) $743,314.38 $200,000.00 $7,406.82 $0.00 $0.00 $117,000.00 $623,905.92 $433,217.10 ($163,500.00) $572,691.08 $53,840.59 ($4,633,118.09) $0.00 ($29,470.32) ($1,318.69) ($583.99) ($6,033.01) $0.00 ($2,815.47) $0.00 ($1,318.69) ($583.99) ($10,000,000.00) $0.00 $0.00 $0.00 ($8,105,000.00) ($7423,000.00) ($2,219,620.65) ($246,172,918.44) $4,497,583.20 $1,100,28148 $0.00 ($204,302.81) $141,569,221.61 $4,302,951.46 $897,140.01 $208,974.39 $31,212,334.17 $133,000.00 $4,633,383.82 $80,495.32 $3,605,133.96 $1,622,425.99 $853,942.65 $61,136.04 $135,642.99 $76,373.78 $128,033.21 $17,023.27 $1,550,989.06 $3,000,000.00 $2,603,485.87 $16,875,305.98 $875,000.00 $2,365,000.00 $429,000.00 $19,172,000.00 F G 1 Account ID B Apollo Shoes, Inc Preclosing Trial Balance: 31-Dec-20 Account Description. 10100 Cash on Hand 10200 Regular Checking Account 10300 Payroll Checking Account 10400 Savings Account 11000 Accounts Receivable 11400 Other Receivables 11500 Allowance for Doubtful Accounts. conomnog 12000 Inventory 12300 Reserve for Inventory Obsolescence 14100 Prepaid Insurance pro doparg 14200 Prepaid Rent. Expan 14300 Office Supplies *** St 14400 Notes Receivable-Current www 14700 Other Current Assets *600* 15000 Land ********** 15100 Buildings and Land Improvemen 15200 Machinery, Equipment, Office F 1000 17000 Accum. Depreciation wwwww 19000 Investments 19900 Other Noncurrent Assets * 20000 Accounts Payable *** mater 23100 Sales Tax Payable 53000 23200 Wages Payable 23300 FICA Employee Withholding 23350 Medicare Withholding 23400 Federal Payroll Taxes Payable 23500 FUTA Tax Payable 23600 State Payroll Taxes Payable 23700 SUTA Tax Payable 23800 FICA Employer Withholding 23900 Medicare Emplover Withholding 24100 Line of Credit 24200 Current Portion Long-Term Debt 24200 Current Portion 24700 Other Current Liabilities 27000 Notes Payable-Noncurrent 39003 Common Stock 39004 Paid-in Capital 39005 35009 Retained Earnings 40000 Sales 40000 Sales 41000 Sales Returns 71000 Sales 42000 Warranty Expense 45000 Income from Investments 46000 Interest Income 10000 47000 Miscellaneous Income 50010 Cost of Goods Sold 30010 COST OF 57500 Freight 60000 Advertising Expense 61000 Auto Expenses 62000 Research and Development www 64000 Depreciation Expense 64500 Warehouse Salaries 65000 Property Tax Expense supe 66000 Legal and Professional Expense Groning and Ad 67000 Bad Debt Expense CORPO 68000 Insurance Expense www. 70000 Maintenance Expense www 70100 Utilities. wwwww conte 70110 Phone 70120 Postal on 16 71000 Miscellaneous Office Expense 72000 Payroll Tax Exp. www 73000 Pension/Profit-Sharing Plan Ex 78600 Controllers' Clearning Account 74000 Rent or Lease Expense 77500 Administrative Wages Expense 78000 Interest Expense с PBC A-2 Debit Amt $2,275.23 $557,125.92 $3,645,599.15 $51,515,259.98 $1,250,000.00 $67,724,527.50 $3,424,213.78 $8,540.00 $117,000.00 $674,313.92 $2,929,097.13 $1,998,780.39 $53,840.59 $11,100,220.89 $1,158,128.47 $130,196,645.26 $4,240,263.09 $1,036,854.01 $210,502.80 $528,870.44 $446,000.00 $4,720,715.56 $99,332.45 $4,913,224.45 $36,106.92 $35,502.87 $137,332.18 $52,599.02 $77,803.61 $24,891.82 $1,577,811.85 $3.630.375.80 $1,206,574.00 $16,197.225.43 $2,591,736.50 D Credit Amt $1,239,009.75 $846,000.00 $610,000.00 $1,922,095.91 $8,439.65 $11,414.99 $118,086.12 $55,106.86 $8,439.65 $11,414.99 $44,403,000.00 $12,000,000.00 $8,105,000.00 $7,423,000.00 $6,590,483.64 ############## $1,426,089.31 $131,881.46 $2,166,000.00 $330,375.80 E Single Column format $2,275.23 $557,125.92 $0.00 O Planning Audit Drogrom $3,645,599.15 $51,515,259.98 $1,250,000.00 ($1,239,009.75) Cooperat $67,724,527.50 www.com ($846,000.00) 2015 20 $3,424,213.78 250.08 non Doku $0.00 www.we $8,540.00 Bronne $0.00 www.ne $0.00 www.www $117,000.00 2015.05 $674,313.92 CA $2,929,097.13 ($610,000.00) $1,998,780.39 400 $53,840.59 Coroa ($1,922,095.91) 20.00 $0.00 $0.00 ($8,439.65) ($11,414.99) ($118,086.12) $0.00 ($55,100.00 $0.00 ($8.439.0 ($11,414.99) ($44,403,000.00) ,000.00) $0.00 $0.00 ($12,000,000.00) 1.000.00 ($8,105.000.00) ($7,423,000.00) ($6,590,483.64) ($242,713,452.88) $11,100,220.89 $1,158,128.47 $1,156,126:47 ($1,426,089.31) ($131,881.46) ($2,166,000.00) $130,150,0.co $4,240,203.09 $1,036,854.01 $210.502.80 $210,502.80 $528,870.44 $446,000.00 $4,720,715.56 $99,332.45 $4,913,224.45 $0.00 826 10 $36,106.92 www. $35,502.87 ******** $137,332.18 AD FOR A $52,599.02 $77,803.61 RASPR $24,891.82 _ $1,577,811.85 $3,630,375.80 ($330,375.80) $1,206,574.00 $16,197,225.43 $2,591,736.50 F G A1 DRC 30 0 1 2 3 4 5 5 7 3 9 0 1 2 3 4 5 6 7 B A B Auditor Darlene Wardlaw Taylor Crump Senior Senior Taylor Crump Taylor Crump Crump Taylor Crump Senior Senior Darlene Wardlaw Senior Taylor Crump D Apollo Shoes, Inc Audit Budget 31-Dec-20 Billing Rate Audit Area 357 Planning 225 Internal Control Testing 298 Cash 298 Accounts Receivable 225 Inventory 225 Prepaids 225 Property, Plant and Equipment 225 Other Assets 298 Current Liabilities 298 Notes Payable 357 Stockholders' Equity 298 Revenue 225 Expenses E F Projected Hours Actual Hours 300 275 150 180 150 90 200 90 200 150 250 200 200 Total Contracted Price Profit Prepared by: Reviewed by: Extended Cost 107,100 61,875 44,700 53,640 33,750 20,250 45,000 20,250 59,600 44,700 89,250 59,600 45,000 $ $ $ $ $ $ $ $ $ $ $ $ $ $ 684,715.00 $ 750,000.00 $ 65,285.00 A-6 DW AA H 1 MASON 2 -2~~~~~~~~88588388588429494 49985 5 11 12 13 14 21 52 53 54 55 56 57 58 15 expenses, and extacadinary item ADJUSTED NET INCOME (LOSS) 59 60 CLIENT: PERIOD ENDED: 61 62 63 64 65 B PROFITORIENTED Net income (loss) Plus (minus) unusual, non-curring revenues and Adjusted net income (loss) multiplied by TOTAL ASSEIS Only if the curent year net income (loss) (or other measure) is significantly different from the entity's historical results would 2-year avenging to obtain normalized net income (loss) (or other measure) be appropriate. ENTITIES Total assets multiplied by: This completed form must be provided to the engagement quality control reviewer in the planning stage of every audit. Please complete all the cells highlighted in yellow. TOTAL REVENUES Plus (minus) usual, non-recurring revenues ADJUSTED REVENUES Total adjusted revenues multiplied by: 2. Basis (Le normalized net income, revenue, total assets, other): 4. Amount selected (planning materiality) 5. Prior year's final materiality PLANNING MATERIALITY CALCULATION 3. Percentage of financial data source used: Engagement Partner 6. Performance materiality/Tolerable misstatement 75% of planning materiality) Engagement Quality Control Reviewer 5% 7. Listing scope (amount threshold for suggested adjustments) (using 5% to 10% of planning materiality based on expected level of adjustments is usually appropriate) C 1% 1% Apollo Shoes December 31, 2020 1. Financial data source (Le. actual, budget, projection): Year end trial balance, actual data obtained from client. Current Year JUSTIFICATION OF PLANNING MATERIALITY 5% D Apollo Shoes ENGAGEMENT MATERIALITY (Required for all engagements) Current Year Current Year Adjusted net income 0 Justification: USE THIS BOX TO DOCUMENT AND JUSTIFY WHICH BASIS YOU'VE SELECTED Standard 5% used Prior Year ● E A Andenon F Emeat Olds A-5 Prepared by Reviewed by Being that Apollo is a new client and we were not provided with materiality amounts from the predecessor auditor, we assume that planning materiality is 5% of net income from 2019. G H Apollo Shoes, Inc. Audit Staffing Memo - A-7 December 31, 2020 A-7 Prepared by: DW Reviewed by: AA Based on the information reviewed in the Apollo Shoes 10-K, minutes of the board of directors, and other documents, I believe that the audit team will require the following specialized expertise: a. Special expertise in Apollo's business and products is probably not necessary. The products are ordinary shoes. The company gave no indication of dealing in complicated transactions such as rubber futures hedging. Auditors with general retail and wholesale experience ought to be able to cope with the expertise demands. b. The audit team will need some special expertise in several areas: (1) the tax personnel probably know how to prepare the state franchise tax return, and that expertise might not be very special, (2) auditors with SEC knowledge and experience will need to participate, and (3) the team will need people with computer expertise on the engagement.

Expert Answer:

Related Book For

Auditing and Assurance services an integrated approach

ISBN: 978-0132575959

14th Edition

Authors: Alvin a. arens, Randal j. elder, Mark s. Beasley

Posted Date:

Students also viewed these accounting questions

-

Each province in Canada has passed legislation that governs the local sale of goods transactions. There is no Federal sale of goods transaction act in Canada. Do you believe that a Federal sale of...

-

Review the minutes of the board of directors and committee meetings for the year and any new agreements, leases, contracts, or other important documents. Obtain copies of the minutes or agreements...

-

The Crazy Eddie fraud may appear smaller and gentler than the massive billion-dollar frauds exposed in recent times, such as Bernie Madoffs Ponzi scheme, frauds in the subprime mortgage market, the...

-

Modesto Trading Berhad has recently appointed Messrs. Suresh Kumar & Co., Chartered Accountants, to audit the companys financial statements for the year ended 30 June 2021. You are assigned by...

-

In Fig P2.71 gate AB is 3 m wide into the paper and is connected by a rod and pulley to a concrete sphere (SG = 2.40). What sphere diameter is just right to close the gate? Concrete phere SG 2.4 6 m...

-

a. Firm D has net income of $61,750, sales of $1,625,000, and average total assets of $650,000. Calculate the firm's margin, turnover, and ROI. b. Firm E has net income of $241,500, sales of...

-

In a turbulent pipe flow that is fully developed, the axial velocity profile is, \[ u=u_{c}\left[1-\left(\frac{r}{R} ight) ight]^{1 / 7} \] as is illustrated in Fig. P5.68. Compare the axial...

-

The Vernom Corporation produces and sells to wholesalers a highly successful line of summer lotion and insect repellents. Vernom has decided to diversify to stabilize sales throughout the year. A...

-

Helix Corporation uses the weighted-average method of process costing. It produces prefabricated flooring in a series of steps carried out in production departments. All of the material used in the...

-

What is activity-based costing, and what are its potential benefits?

-

In the 1976 Pro Bowl. NFL punter Ray Guy of the Oakland Raiders kicked the. ball so high it hit the scoreboard hanging from the roof of the New Orleans SuperDome. If we let h(t) represent the height...

-

Define: Interest-Rate Risk. Define such concept. 2 - Describe: Explain Interest-Rate Risk. The explanation should be using an example. 3 - Reflect: Make a conclusion about how this concept helps you...

-

Claim sizes are normally distributed with mean 0 and variance 1,000,000. The parameter 0 varies by risk class, and is normally distributed with mean 2,500 and variance 4,000,000. In a given risk...

-

How do different valuation methods, such as discounted cash flow (DCF) analysis, price-to-earnings (P/E) ratios, and price-to-book (P/B) ratios, differ in their approach to determining stock value?

-

John takes out a 14% 30-year mortgage in the amount of $65,000. The loan constant is .011849. What is the balance of the loan after the second payment? a. $64,976.14 b. $64,988.14 $64,964.00...

-

1. (30 points) Write a Verilog code to describe the circuit below using the gate-level primitives. 2. (30 points) Write a Verilog code to describe the following functions: (a)...

-

(1) (a) (5 pts) Find 4 x 4 matrices A, B, C so that AB=AC = 0, but BA # 0 and B # C. (b) (10 pts) Find a solution for the following matrix equation (if exists): 0 1 -1 0

-

What are bounds and what do companies do with them?

-

The following internal controls were tested in prior audits. Evaluate each internal control independently and determine which controls must be tested in the current year's audit of the December 31,...

-

Lauren Yost & Co., a medium-sized CPA firm, was engaged to audit Stuart Supply Company. Several staff were involved in the audit, all of whom had attended the firm's in-house training program on...

-

Explain what is meant by a proof of cash receipts and state its purpose.

-

Two small pith balls, initially separated by a large distance, are each given a positive charge of \(5.0 \mathrm{nC}\). By how much does the electric potential energy of the two-ball system change if...

-

The negative terminal of a \(9-\mathrm{V}\) battery is connected to ground via a wire. (a) What is the potential of the negative terminal? (b) What is the potential of the positive terminal? (c) What...

-

Two metallic spheres A and B are placed on nonconducting stands. Sphere A carries a positive charge, and sphere B is electrically neutral. The two spheres are connected to each other via a wire, and...

Study smarter with the SolutionInn App