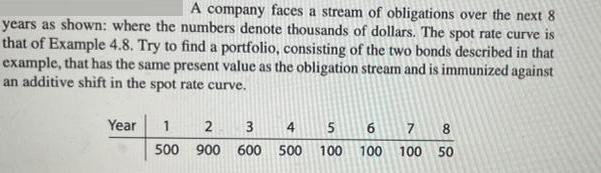

? ? A company faces a stream of obligations over the next 8 years as shown: where

Fantastic news! We've Found the answer you've been seeking!

Question:

?

?

Transcribed Image Text:

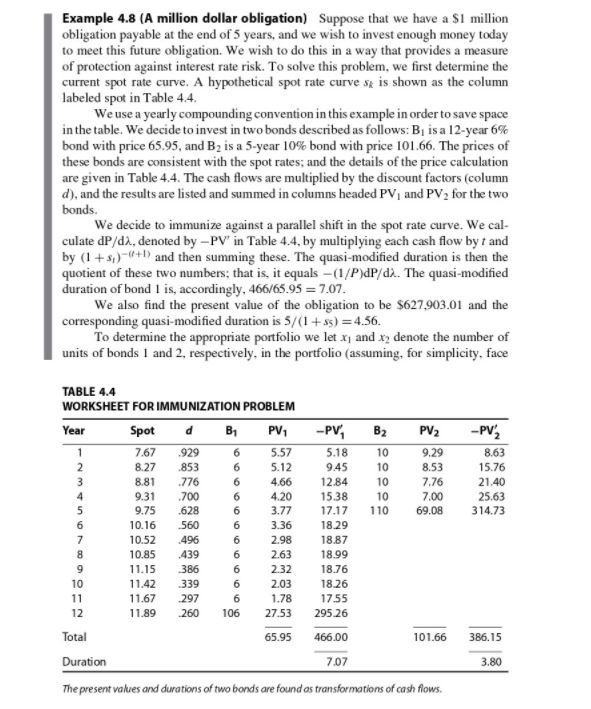

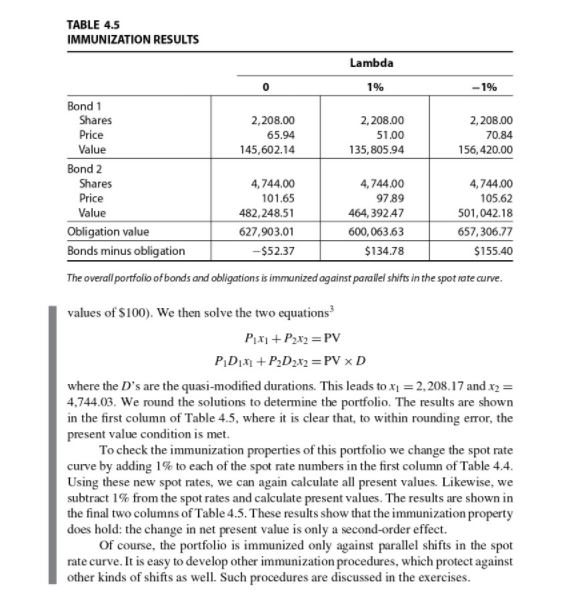

A company faces a stream of obligations over the next 8 years as shown: where the numbers denote thousands of dollars. The spot rate curve is that of Example 4.8. Try to find a portfolio, consisting of the two bonds described in that example, that has the same present value as the obligation stream and is immunized against an additive shift in the spot rate curve. Year 1 2 3 4 500 900 600 500 5 100 10 6 100 7 8 100 50 Example 4.8 (A million dollar obligation) Suppose that we have a $1 million obligation payable at the end of 5 years, and we wish to invest enough money today to meet this future obligation. We wish to do this in a way that provides a measure of protection against interest rate risk. To solve this problem, we first determine the current spot rate curve. A hypothetical spot rate curve s is shown as the column labeled spot in Table 4.4. We use a yearly compounding convention in this example in order to save space in the table. We decide to invest in two bonds described as follows: B₁ is a 12-year 6% bond with price 65.95, and B₂ is a 5-year 10% bond with price 101.66. The prices of these bonds are consistent with the spot rates; and the details of the price calculation are given in Table 4.4. The cash flows are multiplied by the discount factors (column d), and the results are listed and summed in columns headed PV₁ and PV₂ for the two bonds. We decide to immunize against a parallel shift in the spot rate curve. We cal- culate dP/dx, denoted by -PV' in Table 4.4, by multiplying each cash flow by t and by (1+₁)-(+) and then summing these. The quasi-modified duration is then the quotient of these two numbers; that is, it equals -(1/P)dP/dà. The quasi-modified duration of bond 1 is, accordingly, 466/65.95=7.07. We also find the present value of the obligation to be $627.903.01 and the corresponding quasi-modified duration is 5/(1+ ss) = 4.56. To determine the appropriate portfolio we let x₁ and x2 denote the number of units of bonds 1 and 2, respectively, in the portfolio (assuming, for simplicity, face TABLE 4.4 WORKSHEET FOR IMMUNIZATION PROBLEM Year 1 2345 d B₁ 6 6 Spot 7.67 929 8.27 .853 8.81 .776 9.31 .700 9.75 628 10.16 560 10.52 496 10.85 439 11.15 386 339 11.42 11.67 297 11.89 6 6 6 6 6 6 6 6 6 PV₁ 260 106 5.57 5.12 4.66 4.20 3.77 3.36 2.98 2.63 2.32 2.03 1.78 27.53 -PV₁ 5 6 7 8 9 18.76 10 18.26 11 17.55 12 295.26 Total 466.00 Duration 7.07 The present values and durations of two bonds are found as transformations of cash flows. 65.95 5.18 9.45 12.84 15.38 17.17 18.29 18.87 18.99 B₂ PV₂ 10 9.29 10 8.53 10 7.76 10 7.00 110 69.08 101.66 -PV₂ 8.63 15.76 21.40 25.63 314.73 386.15 3.80 TABLE 4.5 IMMUNIZATION RESULTS Bond 1 Shares Price Value Bond 2 0 2,208.00 65.94 145,602.14 4,744.00 101.65 482,248.51 627,903.01 -$52.37 Lambda 1% 2,208.00 51.00 135,805.94 4,744.00 97.89 464,39247 600,063.63 $134.78 -1% Shares Price Value Obligation value Bonds minus obligation The overall portfolio of bonds and obligations is immunized against parallel shifts in the spot rate curve. values of $100). We then solve the two equations³ P₁x₁ + P₂x₂ = PV P₁D₁x + P₂D₂X2=PV x D 2,208.00 70.84 156,420.00 4,744.00 105.62 501,042.18 657,306.77 $155.40 where the D's are the quasi-modified durations. This leads to x₁ = 2,208.17 and x₂ = 4,744.03. We round the solutions to determine the portfolio. The results are shown in the first column of Table 4.5, where it is clear that, to within rounding error, the present value condition is met. To check the immunization properties of this portfolio we change the spot rate curve by adding 1% to each of the spot rate numbers in the first column of Table 4.4. Using these new spot rates, we can again calculate all present values. Likewise, we subtract 1% from the spot rates and calculate present values. The results are shown in the final two columns of Table 4.5. These results show that the immunization property does hold: the change in net present value is only a second-order effect. Of course, the portfolio is immunized only against parallel shifts in the spot rate curve. It is easy to develop other immunization procedures, which protect against other kinds of shifts as well. Such procedures are discussed in the exercises. A company faces a stream of obligations over the next 8 years as shown: where the numbers denote thousands of dollars. The spot rate curve is that of Example 4.8. Try to find a portfolio, consisting of the two bonds described in that example, that has the same present value as the obligation stream and is immunized against an additive shift in the spot rate curve. Year 1 2 3 4 500 900 600 500 5 100 10 6 100 7 8 100 50 Example 4.8 (A million dollar obligation) Suppose that we have a $1 million obligation payable at the end of 5 years, and we wish to invest enough money today to meet this future obligation. We wish to do this in a way that provides a measure of protection against interest rate risk. To solve this problem, we first determine the current spot rate curve. A hypothetical spot rate curve s is shown as the column labeled spot in Table 4.4. We use a yearly compounding convention in this example in order to save space in the table. We decide to invest in two bonds described as follows: B₁ is a 12-year 6% bond with price 65.95, and B₂ is a 5-year 10% bond with price 101.66. The prices of these bonds are consistent with the spot rates; and the details of the price calculation are given in Table 4.4. The cash flows are multiplied by the discount factors (column d), and the results are listed and summed in columns headed PV₁ and PV₂ for the two bonds. We decide to immunize against a parallel shift in the spot rate curve. We cal- culate dP/dx, denoted by -PV' in Table 4.4, by multiplying each cash flow by t and by (1+₁)-(+) and then summing these. The quasi-modified duration is then the quotient of these two numbers; that is, it equals -(1/P)dP/dà. The quasi-modified duration of bond 1 is, accordingly, 466/65.95=7.07. We also find the present value of the obligation to be $627.903.01 and the corresponding quasi-modified duration is 5/(1+ ss) = 4.56. To determine the appropriate portfolio we let x₁ and x2 denote the number of units of bonds 1 and 2, respectively, in the portfolio (assuming, for simplicity, face TABLE 4.4 WORKSHEET FOR IMMUNIZATION PROBLEM Year 1 2345 d B₁ 6 6 Spot 7.67 929 8.27 .853 8.81 .776 9.31 .700 9.75 628 10.16 560 10.52 496 10.85 439 11.15 386 339 11.42 11.67 297 11.89 6 6 6 6 6 6 6 6 6 PV₁ 260 106 5.57 5.12 4.66 4.20 3.77 3.36 2.98 2.63 2.32 2.03 1.78 27.53 -PV₁ 5 6 7 8 9 18.76 10 18.26 11 17.55 12 295.26 Total 466.00 Duration 7.07 The present values and durations of two bonds are found as transformations of cash flows. 65.95 5.18 9.45 12.84 15.38 17.17 18.29 18.87 18.99 B₂ PV₂ 10 9.29 10 8.53 10 7.76 10 7.00 110 69.08 101.66 -PV₂ 8.63 15.76 21.40 25.63 314.73 386.15 3.80 TABLE 4.5 IMMUNIZATION RESULTS Bond 1 Shares Price Value Bond 2 0 2,208.00 65.94 145,602.14 4,744.00 101.65 482,248.51 627,903.01 -$52.37 Lambda 1% 2,208.00 51.00 135,805.94 4,744.00 97.89 464,39247 600,063.63 $134.78 -1% Shares Price Value Obligation value Bonds minus obligation The overall portfolio of bonds and obligations is immunized against parallel shifts in the spot rate curve. values of $100). We then solve the two equations³ P₁x₁ + P₂x₂ = PV P₁D₁x + P₂D₂X2=PV x D 2,208.00 70.84 156,420.00 4,744.00 105.62 501,042.18 657,306.77 $155.40 where the D's are the quasi-modified durations. This leads to x₁ = 2,208.17 and x₂ = 4,744.03. We round the solutions to determine the portfolio. The results are shown in the first column of Table 4.5, where it is clear that, to within rounding error, the present value condition is met. To check the immunization properties of this portfolio we change the spot rate curve by adding 1% to each of the spot rate numbers in the first column of Table 4.4. Using these new spot rates, we can again calculate all present values. Likewise, we subtract 1% from the spot rates and calculate present values. The results are shown in the final two columns of Table 4.5. These results show that the immunization property does hold: the change in net present value is only a second-order effect. Of course, the portfolio is immunized only against parallel shifts in the spot rate curve. It is easy to develop other immunization procedures, which protect against other kinds of shifts as well. Such procedures are discussed in the exercises.

Expert Answer:

Answer rating: 100% (QA)

The articles under this heading describe the main fields of contemporary g... View the full answer

Posted Date:

Students also viewed these mathematics questions

-

Find the total income over the next 8 years from a continuous income stream with an annual rate of flow at time t given by f (t)=8500e-0.2t (dollars per year).

-

3- Two flocks of equipment, each costing 10,000 dinars, the sum of their sale and the cost of operating them one thousand dinars) within five years are shown in the table the children of the required...

-

A company faces two kinds of risk. A firm-specific risk is that a competitor might enter its market and take some of its customers. A market risk is that the economy might enter a recession, reducing...

-

The following information is available for Dylan Inc., a company whose shares are traded on the Toronto Stock Exchange: Other information: 1. For all of the fiscal year 2020, $100,000 of 6%...

-

Who is eligible for Medicare and Medicaid benefits? What do those benefits encompass?

-

The mechanism consists of the four pin-connected bars and three springs, each having a stiffness k and an unstretched length l0 Determine the horizontal forces P that must be applied to the pins in...

-

Chase, Inc., issued 10,000 shares of \(\$ 20\) par value preferred stock at \(\$ 50\) per share and 8,000 shares of no-par value common stock at \(\$ 20\) per share. The common stock has no stated...

-

Corcoran Heavy Industries Company (CHIC) is organized into four divisions, each of which operates in a different industry. The types of customer served and the method used to distribute products...

-

Which of these is NOT a logistics activity?* 1 point inspection warehousing material handling inventory management

-

A particle in one dimension executes oscillatory motion in a potential V(x) = A|x|, where A>0 is a constant of appropriate dimension. If the time period T of its oscillation depends on the total...

-

When working with gas mixtures we often use the approximation that the gas mixture is ideal. However, when studying condensed phases, the simple solution model is often inappropriate. 1. Dene what is...

-

please respond to each post adding viable information and continuing the conversation post 1 Studying gender can make someone more aware of how implicit assumptions influence the structure of...

-

Determine whether the set of vectors in M2,2 is linearly independent or linearly dependent. 2-1 4 3 -7 A = B= C = 4 5 20 23

-

At December 31, Bramble Corporation reports net income of $403,200. Prepare the entry to close net income. (List all debit entries before credit entries. Credit account titles are automatically...

-

Considering the readings Fried "Legal, But Inaccesible" and Cooney "The Way It Was", What are some of the ways (described in both readings) that women's access to reproductive healthcare is being...

-

A CapsLk S Appendix A: Budget/Financial Plans for Bayside Call Centre 6 Month Budget Figures: Month January Budget January Actual February Budget February Actual March April April May May June June...

-

The sales department of P. Gillen Manufacturing Company has forecast sales in March to be 20,000 units. Additional information follows: Finished goods inventory, March 1 . . . . . . . . . . . . . . ....

-

What is compartmentalizing?

-

The increase in total utility that one receives from eating an additional piece of sushi is called a. marginal utility. b. interpersonal utility. c. marginal cost. d. average utility. e. average cost.

-

What is the ultimatum game?

Study smarter with the SolutionInn App