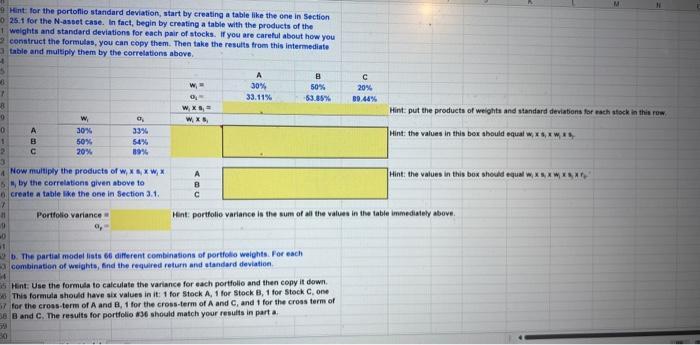

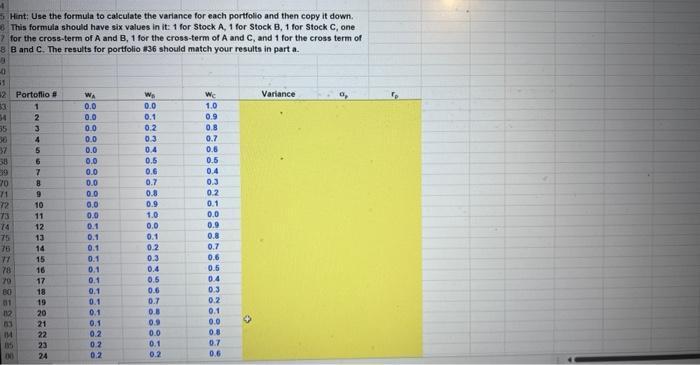

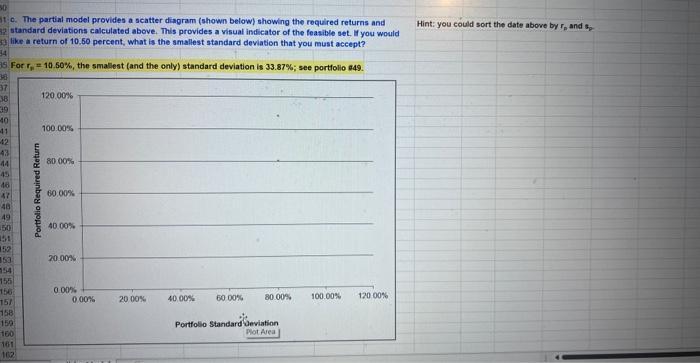

9 Hint for the portoflio standard deviation, start by creating a table like the one in...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

Answer a Expected Return WA Return A WB Return B WC Return C Expected Return Portfolio Weight W Ret... View the full answer

Related Book For

Posted Date: