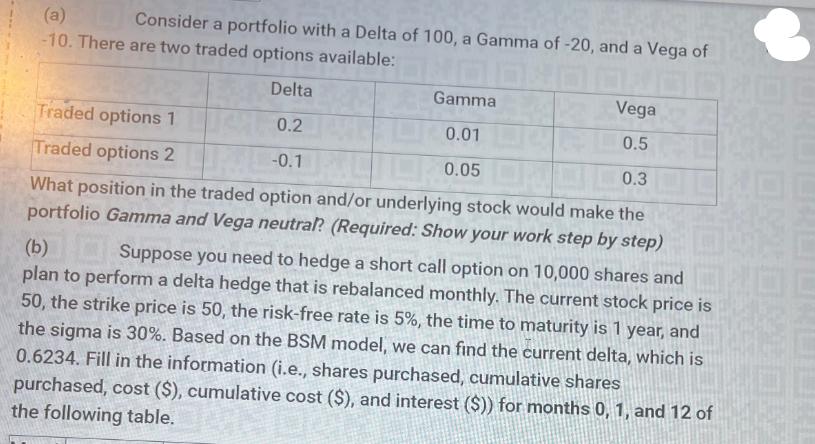

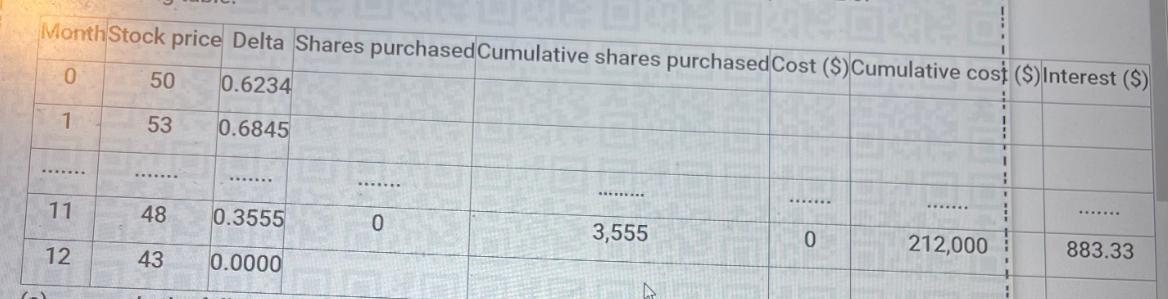

(a) -10. There are two traded options available: Delta Traded options 1 0.2 Traded options 2...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

Gamma and Vega Neutral Portfolio To make the portfolio gamma and vega neutral you need to create a combination of Traded Option 1 and Traded Option 2 ... View the full answer

Related Book For

Posted Date: