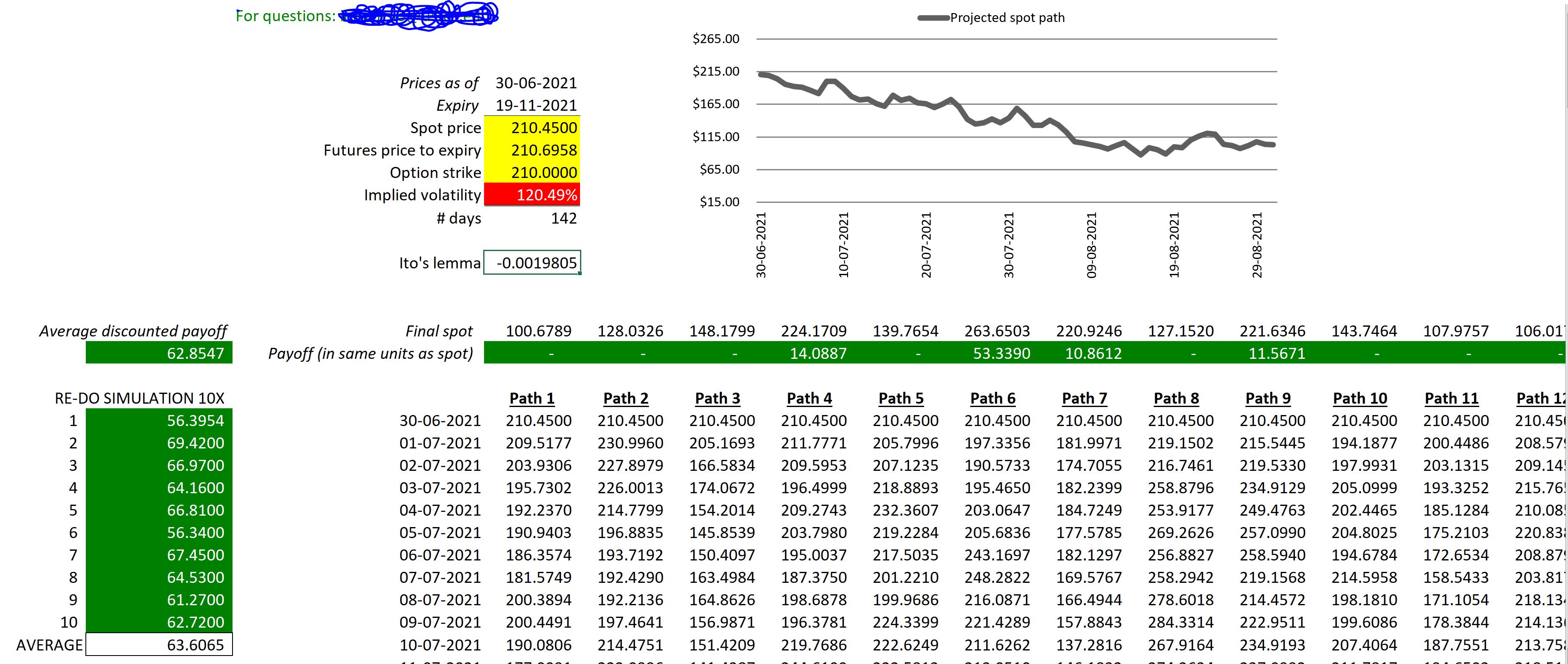

A barrier option is an 'exotic' option that shares all the attributes of vanilla option, but adds

Question:

A barrier option is an 'exotic' option that shares all the attributes of vanilla option, but adds a contingency such that the price of a barrier option is generally worth less than the equivalent vanilla option. Investors like barrier options because they are less expensive, offer better leverage, and enable expressing more well-defined views.

Generally-speaking, a contingency that limits the potential payoff will lower the initial premium. A knock-out (knock-in) option is a special type of barrier option that shares all the attributes of a vanilla option,but the option ceases to (will only) exist if the spot price of the asset trades at a predetermined level (aka the barrier) at *anytime* during the life of the option. The barrier of a reverse knock-out (knock-in) option is placed such that the option would be in-the-money if breached. The barrier of a knock-out (knock-in)option is placed such that the option would be out-of-the-money if breached.

1. Use the Monte Carlo model to price a reverse knock-in (RKI)option that is equivalent to the vanilla call option we priced in class, referenced above, except that the option does not exist unless the spot price of $500 trades at anytime between the pricing date and the expiry date. Note we are using daily data for pricing this option via Monte Carlo, but in actual practice the option would be priced in continuous time.

2. Use the Monte Carlo model to price a reverse knock-out (RKO) option that is equivalent to the vanilla call option we priced in class, referenced above, except that the option ceases to exist if the spot price of $500 trades at anytime between the pricing date and the expiry date. Note we are using daily data for pricing this option via Monte Carlo, but in actual practice the option would be priced in continuous time.

3. Why is the price of the RKI so different than the price of the RKO? Explain.

4. Use the Monte Carlo model to price a knock-in (KI) option that is equivalent to the vanilla call option we priced in class, referenced above, except that the option does not exist unless the spot price of $100 trades at anytime between the pricing date and the expiry date. Note we are using daily data for pricing this option via Monte Carlo, but in actual practice the option would be priced in continuous time.

5. Use the Monte Carlo model to price a knock-in (KO) option that is equivalent to the vanilla call option we priced in class, referenced above, except that the option ceases to exist if the spot price of $100 trades at anytime between the pricing date and the expiry date. Note we are using daily data for pricing this option via Monte Carlo, but in actual practice the option would be priced in continuous time.

6. Why is the price of the KI so different than the price of the KO? Explain.

7. Can you think about an option combination from the set we covered in class that would offer a similar risk/reward proposition as the RKO in question 2? Fully describe the strategy, the payoffs, and how it is both similar and different to the RKO.

Expert Answer:

Contemporary Human Resource Management Text And Cases

ISBN: 9780273757825

4th Edition

Authors: Tom Redman, Adrian Wilkinson