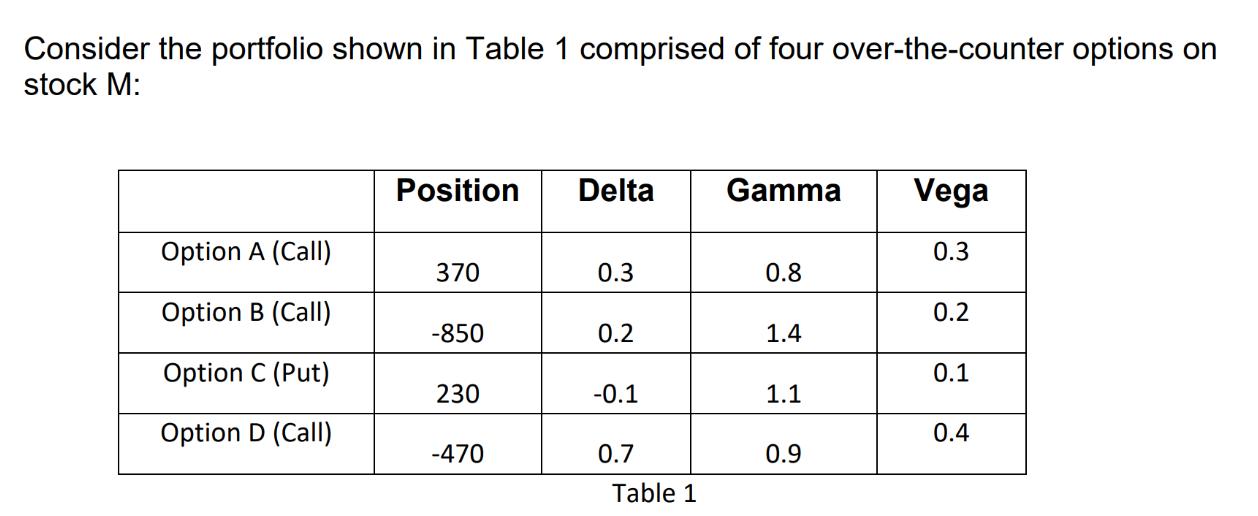

a) Compute the delta, gamma and vega of the portfolio. What position is needed to make the

Fantastic news! We've Found the answer you've been seeking!

Question:

a) Compute the delta, gamma and vega of the portfolio. What position is needed to make the portfolio delta neutral? [10 marks]

a) Compute the delta, gamma and vega of the portfolio. What position is needed to make the portfolio delta neutral? [10 marks] b) A new traded option (Option 1) is available on the market with a delta of -0.3, a gamma of 0.8 and a vega of 0.3. What are the positions needed to make the portfolio gamma and delta neutral? [10 marks]

c) Is it possible to make the portfolio gamma, vega and delta neutral using only Option 1? [5 marks]

d) Suppose that a second traded option is available (Option 2). The option has a delta of 0.2, a gamma of 0.2 and a vega of 0.6. Use Options 1 and 2 to make the portfolio gamma, vega and delta neutral.

Expert Answer:

To solve the given problem lets calculate the delta gamma and vega of the portfolio and then determine the positions needed to make the portfolio delt... View the full answer

Related Book For

Posted Date: