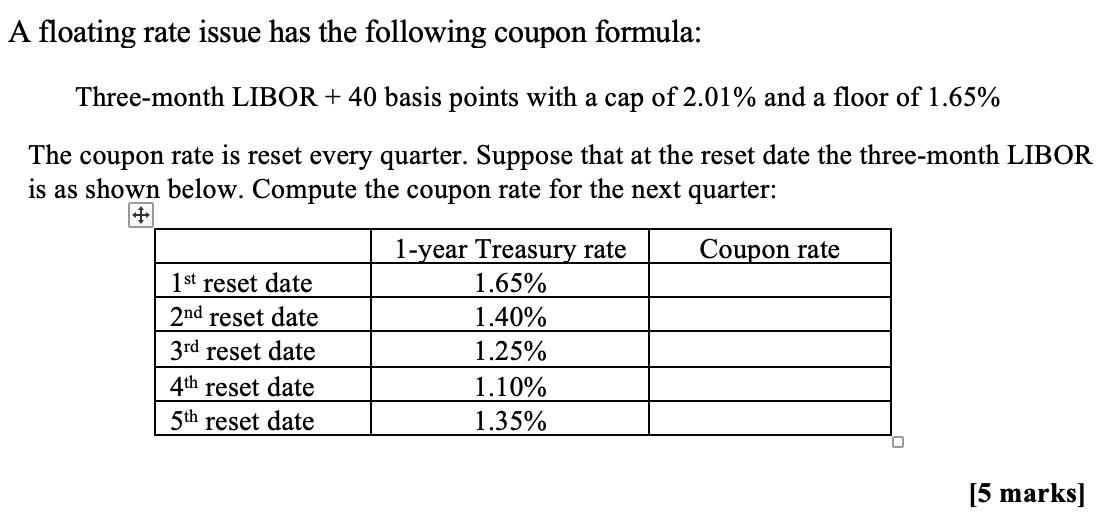

A floating rate issue has the following coupon formula: Three-month LIBOR + 40 basis points with...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

To calculate the coupon rate for the next quarter we need to compare the current threemonth LIBOR ra... View the full answer

Related Book For

Posted Date: