(a) For Scenario 1 (X acquires Z on 1 January 2024), apply the appropriate accounting rules in...

Question:

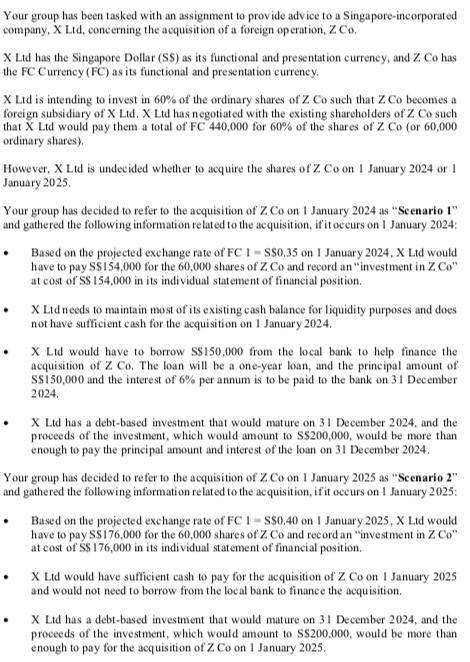

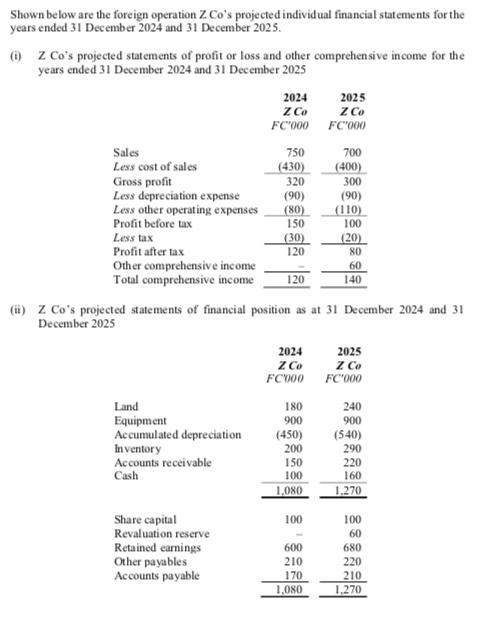

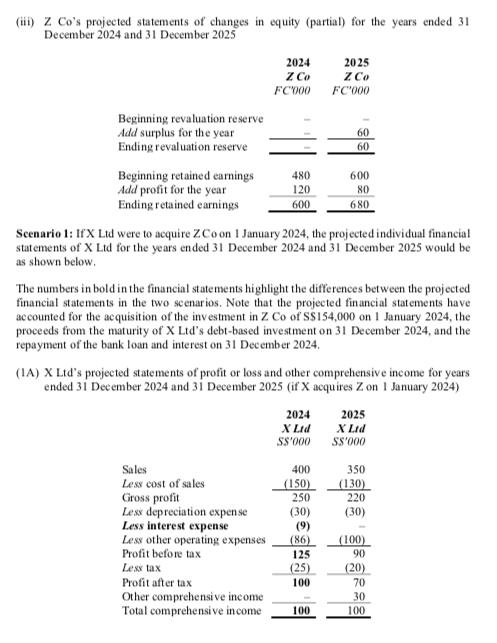

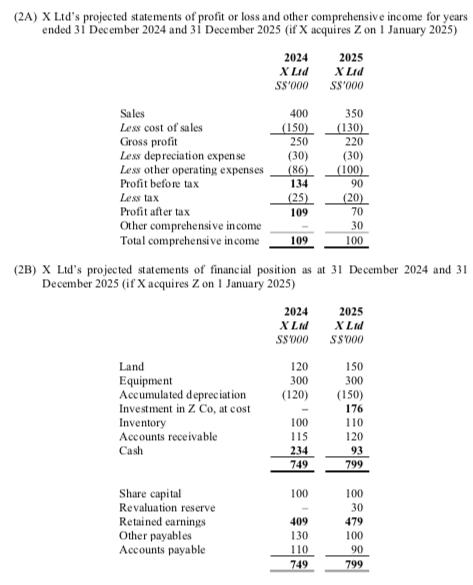

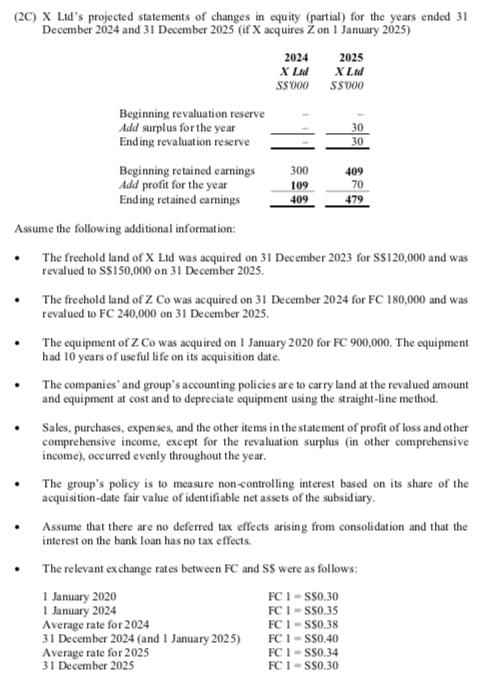

(a) For Scenario 1 (X acquires Z on 1 January 2024), apply the appropriate accounting rules in SFRS(I) 1-21 to translate Z Co’s individual financial statements (statement of profit or loss and other comprehensive income, statement of financial position, and statement of change in equity (partial)) for the year ended 31 December 2024 into X Ltd’s presentation currency of S$. In your answer, include your workings for the calculation of translation difference for the year.

(b) For Scenario 1 (X acquires Z on 1 January 2024), apply the appropriate accounting rules in SFRS(I) 1-21 to translate Z Co’s individual financial statements (statement of profit or loss and other comprehensive income, statement of financial position, and statement of change in equity (partial)) for the subsequent year ended 31 December 2025 into X Ltd’s presentation currency of S$. In your answer, include your workings for the calculation of translation difference for the year.

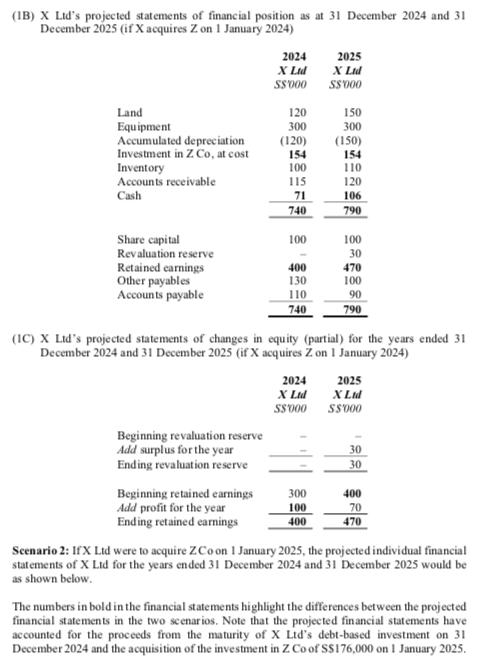

(c) For Scenario 1 (X acquires Z on 1 January 2024), prepare the consolidation journal entries and the projected consolidated financial statements (consolidated statement of profit or loss and other comprehensive income, consolidated statement of financial position, and consolidated statement of change in equity (partial)) of X Ltd and its subsidiary for the year ended 31 December 2024.

(d) For Scenario 1 (X acquires Z on 1 January 2024), prepare the consolidation journal entries and the projected consolidated financial statements (consolidated statement of profit or loss and other comprehensive income, consolidated statement of financial position, and consolidated statement of change in equity (partial)) of X Ltd and its subsidiary for the subsequent year ended 31 December 2025.

(e) Ignore Parts (a) to (d) above. For Scenario 2 (X acquires Z on 1 January 2025), apply the appropriate accounting rules in SFRS(I) 1-21 to translate Z Co’s individual financial statements (statement of profit or loss and other comprehensive income, statement of financial position, and statement of change in equity (partial)) for the year ended 31 December 2025 into X Ltd’s presentation currency of S$. In your answer, include your workings for the calculation of translation difference for the year.

(f) Ignore Parts (a) to (d) above. For Scenario 2 (X acquires Z on 1 January 2025), prepare the consolidation journal entries and the projected consolidated financial statements (consolidated statement of profit or loss and other comprehensive income, consolidated statement of financial position, and consolidated statement of change in equity (partial)) of X Ltd and its subsidiary for the year ended 31 December 2025.

(g) Based on your answers in Parts (a) to (f) and the information given in the question, recommend whether X Ltd should acquire 60% of the shares of Z Co on 1 January 2024 (Scenario 1) or on 1 January 2025 (Scenario 2). Remember to provide justifications or explanations for your recommendation.

Expert Answer:

Based on the information provided heres the analysis for both scenarios Scenario 1 Acquisition on 1 ... View the full answer

Financial Accounting and Reporting

ISBN: 978-1292162409

18th edition

Authors: Barry Elliott, Jamie Elliott