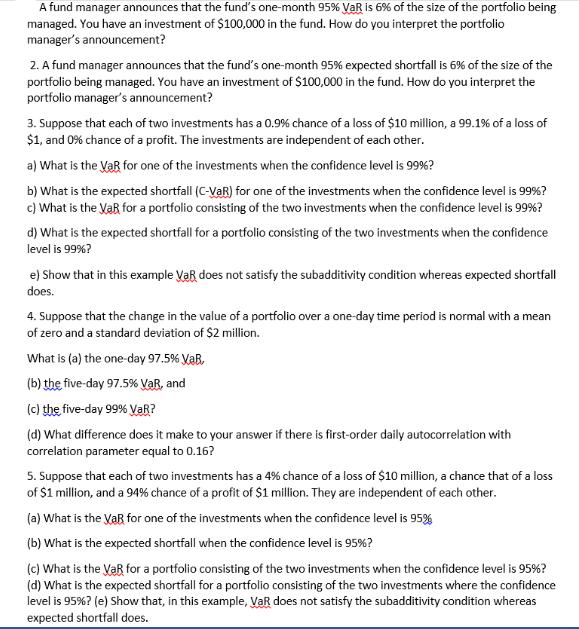

A fund manager announces that the fund's one-month 95% VaR is 6% of the size of...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

1 When the fund manager announces that the funds onemonth 95 Value at Risk VaR is 6 of the size of the portfolio being managed it means that there is a 95 confidence level that the maximum potential l... View the full answer

Related Book For

Posted Date: