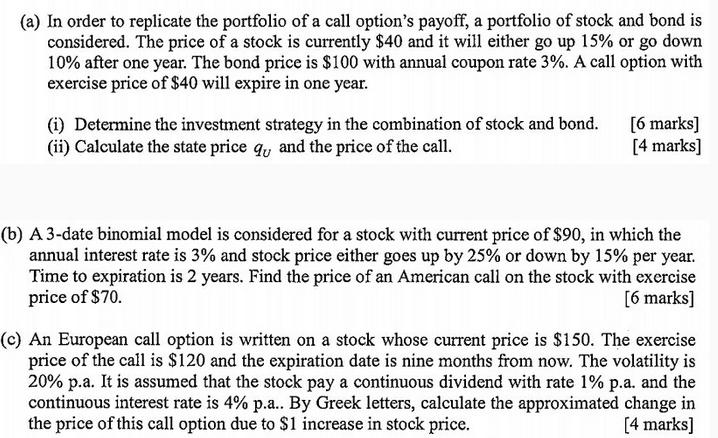

(a) In order to replicate the portfolio of a call option's payoff, a portfolio of stock...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

a i The investment strategy to replicate the portfolio of a call options payoff involves creating a ... View the full answer

Related Book For

Intermediate Financial Management

ISBN: 978-1111530266

11th edition

Authors: Eugene F. Brigham, Phillip R. Daves

Posted Date: