Gazel Tech Bhd is a manufacturing company specialising in computer department of the company is preparing...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

Gazel Tech Bhd is a manufacturing company specialising in computer department of the company is preparing the financial statements for the year ended 31 December 2018 which will be authorised for issue on 31 March 2019. The trial and technical services. The accounting balance of the company based on the unadjusted account balances is shown below: Gazel Tech Bhd Trial balance as at 31 December 2018 Debit Credit RM RM 13,494,00O Revenue Cost of sales 6,500.000 1.111,500 2,074,800 Distribution costs Administrative costs Investment income Allowance for impairment of trade receivables Accumulated depreciation of plant and equipment as at 1 January 2018 Accumulated depreciation of building as at 1 January 2018 Accounts payable Ordinary shares Retained earnings, 1 January 2018 6% Loan from MMB Bank (taken on 30 June 2018) Tax paid 390,000 180,700 3,640.00O 325,000 1,833.00O 10,400.000 2,243,80O 650.000 910.000 2,444.000 1,300.000 3.104,40O 9.100,000 1.716.00O 884.000 1,873,300 819,000 1,306,50O 13.000 33.156,50o 33,156,50O Inventories, 31 December 2018 Building Freehold land Plant and equipment Investment property Patents Accounts receivable Long term investment Cash & bank balances Interests on loan from MMB Bank Additional information: 1. Information relating to the company's non-current assets during the year is as follows: On 31 December 2018, the freehold land was revalued to RM3,510,000. ii. A land was acquired on 1 April 2018 for undetermined future used for RM715,000. The fair value of the land as at 31 December 2018 was RM845,000. i. A motor vehicle was acquired on 1 March 2018 for RM390,000. iv. Gazel Tech Bhd bought a high-tech equipment from a United Stated company on 1 July 2018 for USD 156,000 and paid for it on 30 September 2018. The related exchange rates were as follows: USD 1=RM 3.20 1 July 2018 30 September 2018 USD 1 RM 3.50 31 December 2018 JUSD 1=RM 3.40 No entries have been made for the acquisition of the above equipment. 2. Gazel Tech Bhd depreciates its non-current assets as follows: Building Plant & Machinery 10% on cost Motor vehicle 10 years, Straight line 40 years, Straight line Depreciation expenses are charged to administrative expenses and on monthly basis. The depreciation charges for the year ended 31 December 2018 have not been made. The investment properties are measured on the fair value model. 3. Information relating to the company's intangible assets is as follows: A copyright was acquired at an initial cost of RM380,000 on 1 July 2018 and is to be amortised over a period of 10 years. i. The patent has an indefinite useful life. i It is the policy of the company to adopt cost model on the subsequent measurement of its intangible i. asset. 4. Gazel Tech Bhd sells computers that include a warranty to make repair or replace any defect in its computers for 120 days. Based on experience, it is probable that there will be some claims under the warranties. Gazel Tech Bhd estimates that such returns usually amount to RM5,200 annually. During the year ended 31 December 2018 a lawsuit as per mentioned by the company's lawyer involved a staff who has sued the company amounting to RM650,000 for failure to provide a safe working environment causing him to lose his right hand. The company's lawyer stated that the company will be held liable. 5. On 1 February 2019, the company entered into a contract with Super Bhd to purchase of building located at Kota Kinabalu area for RM10,000,000. During the year, an employee of the company who has been dismissed for improper conduct has sued the company for unfair dismissal. The company's lawyer is of the opinion that it is unlikely that the employee will win the case. 6. 7. 8. One of the Gazel Tech Bhd's customer who owed the company RM11,700 was declared bankrupt on 1 January 2019. None of the amount is expected to be recovered. 8. One of the Gazel Tech Bhd's customer who owed the company RM11,700 was declared bankrupt on 1 January 2019. None of the amount is expected to be recovered. 9. While preparing the final account for 31 December 2018, the accounts clerk discovered that an amount of RM130,000 payment for credit purchases for year ended 2015 has been wrongly accounted as interest on loan. 10. The revenue figure above excludes a credit sale amounting RM78,000 (cost December 2018 but the delivery was delayed until early January 2019 due to special request from a customer as he is still renovating its building. RM39,000) on 1 On 1 January 2018, Gazel Tech Bhd signed a contract with a customer to sell a computer as well as a 12-month technical support for RM840,000. Gazel Tech Bhd delivered 100 units computers and transferred its legal title to the customer on 30 January 2018. The customer paid the full amount on the same date. The standalone price of the computer and the technical support for each computer are RM8,000 and RM1,000 respectively. This entry has been omitted from the business books for the year ended 31 December 2018. 11. 12. The following information also available as at the financial year end: The tax expense for the year is estimated to be RM650,000. ii. The net realisable value of the closing inventory was RM2,340,000. iii. The interest on loan for November and December 2018 still owing. i. Required: Prepare the following statements for the company in compliance with the Companies Act 2016 (amended) and the relevant financial reporting standards: a. Statement of Profit or Loss and Other Comprehensive Income for the year ended 31 December 2018; b. Statement of Financial Position as at 31 December 2018; c. Statement of Changes in Equity for the year ended 31 December 2018; d. The Notes to the Financial Statements for property, plant and equipment and non-adjusting event after reporting period (if any). Gazel Tech Bhd is a manufacturing company specialising in computer department of the company is preparing the financial statements for the year ended 31 December 2018 which will be authorised for issue on 31 March 2019. The trial and technical services. The accounting balance of the company based on the unadjusted account balances is shown below: Gazel Tech Bhd Trial balance as at 31 December 2018 Debit Credit RM RM 13,494,00O Revenue Cost of sales 6,500.000 1.111,500 2,074,800 Distribution costs Administrative costs Investment income Allowance for impairment of trade receivables Accumulated depreciation of plant and equipment as at 1 January 2018 Accumulated depreciation of building as at 1 January 2018 Accounts payable Ordinary shares Retained earnings, 1 January 2018 6% Loan from MMB Bank (taken on 30 June 2018) Tax paid 390,000 180,700 3,640.00O 325,000 1,833.00O 10,400.000 2,243,80O 650.000 910.000 2,444.000 1,300.000 3.104,40O 9.100,000 1.716.00O 884.000 1,873,300 819,000 1,306,50O 13.000 33.156,50o 33,156,50O Inventories, 31 December 2018 Building Freehold land Plant and equipment Investment property Patents Accounts receivable Long term investment Cash & bank balances Interests on loan from MMB Bank Additional information: 1. Information relating to the company's non-current assets during the year is as follows: On 31 December 2018, the freehold land was revalued to RM3,510,000. ii. A land was acquired on 1 April 2018 for undetermined future used for RM715,000. The fair value of the land as at 31 December 2018 was RM845,000. i. A motor vehicle was acquired on 1 March 2018 for RM390,000. iv. Gazel Tech Bhd bought a high-tech equipment from a United Stated company on 1 July 2018 for USD 156,000 and paid for it on 30 September 2018. The related exchange rates were as follows: USD 1=RM 3.20 1 July 2018 30 September 2018 USD 1 RM 3.50 31 December 2018 JUSD 1=RM 3.40 No entries have been made for the acquisition of the above equipment. 2. Gazel Tech Bhd depreciates its non-current assets as follows: Building Plant & Machinery 10% on cost Motor vehicle 10 years, Straight line 40 years, Straight line Depreciation expenses are charged to administrative expenses and on monthly basis. The depreciation charges for the year ended 31 December 2018 have not been made. The investment properties are measured on the fair value model. 3. Information relating to the company's intangible assets is as follows: A copyright was acquired at an initial cost of RM380,000 on 1 July 2018 and is to be amortised over a period of 10 years. i. The patent has an indefinite useful life. i It is the policy of the company to adopt cost model on the subsequent measurement of its intangible i. asset. 4. Gazel Tech Bhd sells computers that include a warranty to make repair or replace any defect in its computers for 120 days. Based on experience, it is probable that there will be some claims under the warranties. Gazel Tech Bhd estimates that such returns usually amount to RM5,200 annually. During the year ended 31 December 2018 a lawsuit as per mentioned by the company's lawyer involved a staff who has sued the company amounting to RM650,000 for failure to provide a safe working environment causing him to lose his right hand. The company's lawyer stated that the company will be held liable. 5. On 1 February 2019, the company entered into a contract with Super Bhd to purchase of building located at Kota Kinabalu area for RM10,000,000. During the year, an employee of the company who has been dismissed for improper conduct has sued the company for unfair dismissal. The company's lawyer is of the opinion that it is unlikely that the employee will win the case. 6. 7. 8. One of the Gazel Tech Bhd's customer who owed the company RM11,700 was declared bankrupt on 1 January 2019. None of the amount is expected to be recovered. 8. One of the Gazel Tech Bhd's customer who owed the company RM11,700 was declared bankrupt on 1 January 2019. None of the amount is expected to be recovered. 9. While preparing the final account for 31 December 2018, the accounts clerk discovered that an amount of RM130,000 payment for credit purchases for year ended 2015 has been wrongly accounted as interest on loan. 10. The revenue figure above excludes a credit sale amounting RM78,000 (cost December 2018 but the delivery was delayed until early January 2019 due to special request from a customer as he is still renovating its building. RM39,000) on 1 On 1 January 2018, Gazel Tech Bhd signed a contract with a customer to sell a computer as well as a 12-month technical support for RM840,000. Gazel Tech Bhd delivered 100 units computers and transferred its legal title to the customer on 30 January 2018. The customer paid the full amount on the same date. The standalone price of the computer and the technical support for each computer are RM8,000 and RM1,000 respectively. This entry has been omitted from the business books for the year ended 31 December 2018. 11. 12. The following information also available as at the financial year end: The tax expense for the year is estimated to be RM650,000. ii. The net realisable value of the closing inventory was RM2,340,000. iii. The interest on loan for November and December 2018 still owing. i. Required: Prepare the following statements for the company in compliance with the Companies Act 2016 (amended) and the relevant financial reporting standards: a. Statement of Profit or Loss and Other Comprehensive Income for the year ended 31 December 2018; b. Statement of Financial Position as at 31 December 2018; c. Statement of Changes in Equity for the year ended 31 December 2018; d. The Notes to the Financial Statements for property, plant and equipment and non-adjusting event after reporting period (if any).

Expert Answer:

Answer rating: 100% (QA)

SOLUTION A STATEMENT OF PROFIT LOSS ACCOUNT REVENUE 14326222 LESS COST OF SALES INCLUDING IMPAIRMENT ON INVENTORIES WARRANTIES EXPENSE 6609200 GROSS PROFIT 7717022 DISTRIBUTION COSTS 1111500 ADMINISTR... View the full answer

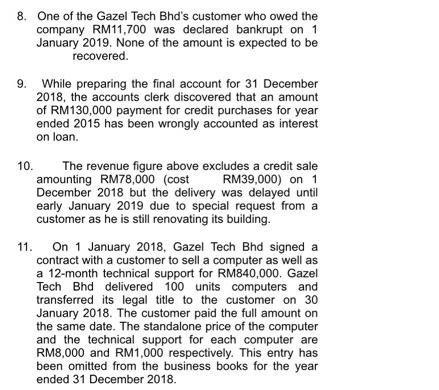

Related Book For

Fundamentals of corporate finance

ISBN: 978-0470876442

2nd Edition

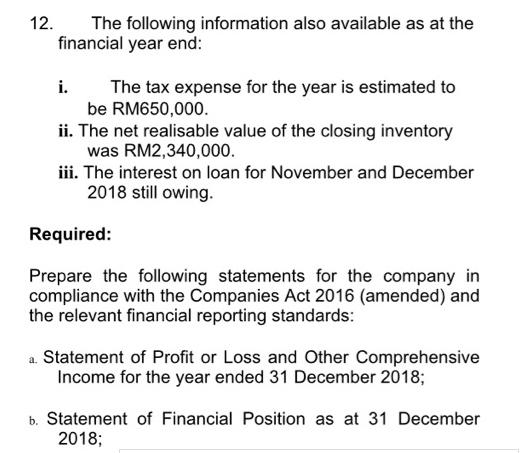

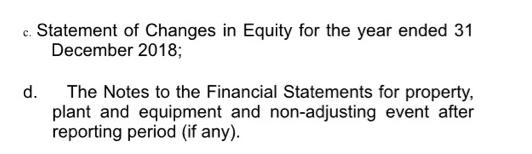

Authors: Robert Parrino, David S. Kidwell, Thomas W. Bates

Posted Date:

Students also viewed these accounting questions

-

DATE REPORTED or CONFIRMED 07 SA T 07 9A R 07 9A T 07 9A R 07 9A T 6 9A T 07 9A R 06 9A T 06 9A R 07 9A T 07 9A T SOURCE RFFDD Following is the credit history information on Peter and Penny...

-

The summarized statements for the year ended 31 December 2007 for Mat, Rug and P entities are as follows: Statements of comprehensive income for the year ended 31 December 2007 The following...

-

In preparing the financial statements for the year ended 31 December 20X5 Alpha plc discovers the following, all of which are material in the context of the company's results: Development...

-

Not sure if this note is applicable to the problem? (A2) Prove there is a bijection between any two countably infinite sets.

-

You are a project supervisor with SDR, Inc., a data analysis and consulting firm based in Atlanta. You are supervising the data preparation process for a large survey conducted for a leading...

-

This video from the USDA discusses how to identify and avoid conflicts of interest. After students have watched the video, conduct an instructor-led debrief using the questions provided. a. What is a...

-

Financial Statement Analysis Limitations Which of the following is not considered a limitation of financial statement analysis? a. Firms may use different accounting methods. b. Firms may be audited...

-

In March 2004, White was stopped in her van when Berkenheuer, driving a Penske truck in the course of his job with Taylor Distributing Company hit her, causing her serious injury. White settled a...

-

2)(50 puan) f(x) = sin (x) ve g(x) = cos (x) olmak zere (a) y = f(x) ve y = g(x) fonksiyonlarnn x E [-2, 2] iin artan ve azalan olduu aralklar belirleyiniz. Yerel ekstremum noktalarnn apsislerini ve...

-

Consider the three-variable linear programming problem shown in Fig. 5.2. (a) Construct a table like Table 5.4, giving the indicating variable for each constraint boundary equation and original...

-

ssa Tony and Suzie graduate from college in May 2021 and begin developing their new business. They begin by offering clinics for basic outdoor activities such as mountain biking or kayaking. Upon...

-

Which of the following is a systems flowchart? a. A description of the sequence of operations and logic in a computer program. b. A description of the sequence of major processing operations and the...

-

What are some inquiries an auditor can make when examining the long-term debt account to add value to the audit?

-

Which of the following questions would an auditor ask while auditing accounts receivable to add value to an audit? a. Are accounts receivable pledged? b. Are customers satisfied with your billing...

-

Which of the following is not a batch control? a. Control total. b. Hash total. c. Record count. d. Parity check.

-

Which of the following procedures would not improve internal control in a computer system? a. One computer operator running all programs. b. Limited access to computer programs. c. Programmers not...

-

Monique works for Rapid Solutions in Qubec and her 2023 year-to- date payroll totals are regular earnings of $65,725.00. regular commission payments $12,320.00, employer-provided automobile taxable...

-

Refrigerant-134a enters an adiabatic compressor as saturated vapor at 120 kPa at a rate of 0.3 m3/min and exits at 1-MPa pressure. If the isentropic efficiency of the compressor is 80 percent,...

-

One way to extend the binomial pricing model is by including multiple time periods. Suppose Splittime, Inc., is currently trading for $100 per share. In one month, the price will either increase by...

-

Currently, dividends are taxed at a maximum rate of 15 percent. Unless Congress acts by 2012, this favorable tax treatment will lapse and the rate will increase. What would you expect to happen to...

-

Freisinger, Inc., is expecting a new project to start paying off , beginning at the end of next year. It expects cash flows to be as follows: If Freisinger can reinvest these cash flows to earn a...

-

Full IFRS and IFRS for SMEs do not permit recognition on the income statement of extraordinary items. What are the rules in the United States for extraordinary items? Evaluate the pros and cons of...

-

IFRS for SMEs has been referred to as IFRS lite. One of the differences between full IFRS and IFRS for SMEs is that full IFRS allows for judgment in making choices about proper accounting, whereas...

-

The 2009 European fraud survey cautions against the manipulation of asset impairment writedowns due to the subjective factors used and judgment needed to draw conclusions about the proper amount of...

Study smarter with the SolutionInn App