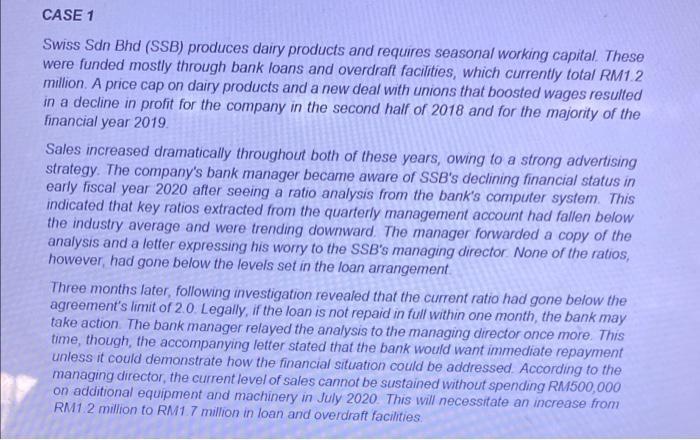

CASE 1 Swiss Sdn Bhd (SSB) produces dairy products and requires seasonal working capital. These were...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

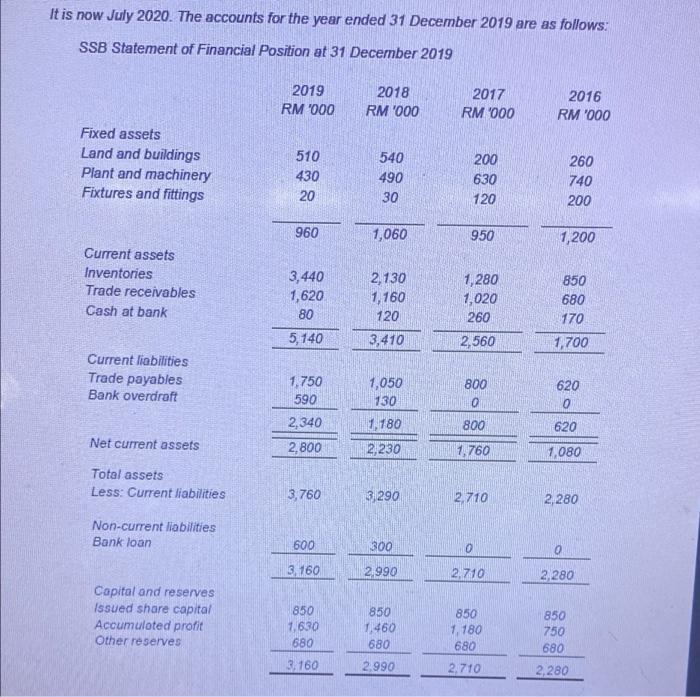

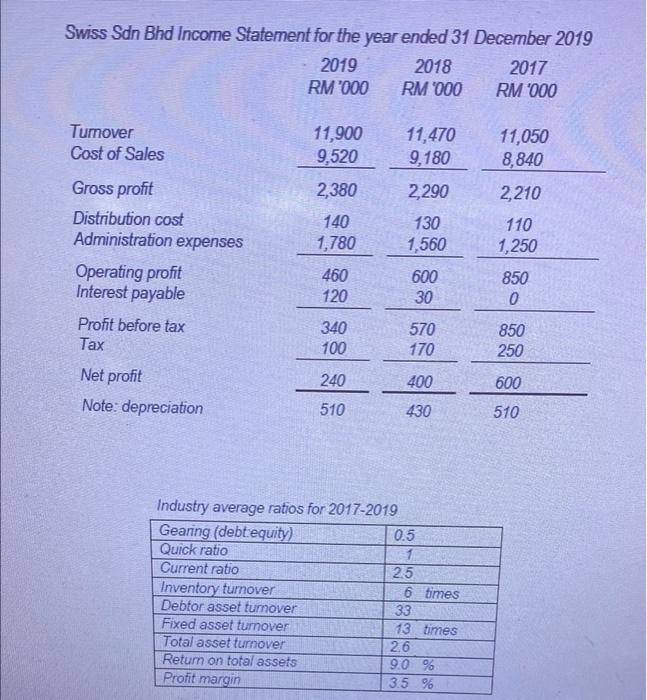

CASE 1 Swiss Sdn Bhd (SSB) produces dairy products and requires seasonal working capital. These were funded mostly through bank loans and overdraft facilities, which currently total RM1.2 million. A price cap on dairy products and a new deal with unions that boosted wages resulted in a decline in profit for the company in the second half of 2018 and for the majority of the financial year 2019. Sales increased dramatically throughout both of these years, owing to a strong advertising strategy. The company's bank manager became aware of SSB's declining financial status in early fiscal year 2020 after seeing a ratio analysis from the bank's computer system. This indicated that key ratios extracted from the quarterly management account had fallen below the industry average and were trending downward. The manager forwarded a copy of the analysis and a letter expressing his worry to the SSB's managing director None of the ratios, however, had gone below the levels set in the loan arrangement Three months later, following investigation revealed that the current ratio had gone below the agreement's limit of 2.0. Legally, if the loan is not repaid in full within one month, the bank may take action. The bank manager relayed the analysis to the managing director once more. This time, though, the accompanying letter stated that the bank would want immediate repayment unless it could demonstrate how the financial situation could be addressed. According to the managing director, the current level of sales cannot be sustained without spending RM500,000 on additional equipment and machinery in July 2020. This will necessitate an increase from RM1.2 million to RM1.7 million in loan and overdraft facilities. It is now July 2020. The accounts for the year ended 31 December 2019 are as follows: SSB Statement of Financial Position at 31 December 2019 Fixed assets Land and buildings Plant and machinery Fixtures and fittings Current assets Inventories Trade receivables Cash at bank Current liabilities Trade payables Bank overdraft Net current assets Total assets Less: Current liabilities Non-current liabilities Bank loan Capital and reserves Issued share capital Accumulated profit Other reserves 2019 RM '000 510 430 20 960 3,440 1,620 80 5,140 1,750 590 2,340 2,800 3,760 600 3,160 850 1,630 680 3,160 2018 RM '000 540 490 30 1,060 2,130 1,160 120 3,410 1,050 130 1,180 2,230 3,290 300 2,990 850 1,460 680 2,990 2017 RM '000 200 630 120 950 1,280 1,020 260 2,560 800 800 1,760 2,710 0 2,710 850 1,180 680 2,710 2016 RM '000 260 740 200 1,200 850 680 170 1,700 620 0 620 1,080 2,280 0 2,280 850 750 680 2,280 Swiss Sdn Bhd Income Statement for the year ended 31 December 2019 2019 2018 RM '000 RM '000 Turnover Cost of Sales Gross profit Distribution cost Administration expenses Operating profit Interest payable Profit before tax Tax Net profit Note: depreciation 11,900 9,520 Return on total assets Profit margin 2,380 140 1,780 460 120 340 100 240 510 Industry average ratios for 2017-2019 Gearing (debt equity) Quick ratio Current ratio Inventory turnover Debtor asset turnover Fixed asset turnover Total asset turnover 11,470 9,180 2,290 130 1,560 600 30 570 170 400 430 0.5 1 2.5 6 times 33 13 times 2.6 9.0 % 3.5 % 2017 RM '000 11,050 8,840 2,210 110 1,250 850 0 850 250 600 510 d. If the bank granted the additional loan, could the company pay off the loan by 31 December 2020? Explain. (8 marks) CASE 1 Swiss Sdn Bhd (SSB) produces dairy products and requires seasonal working capital. These were funded mostly through bank loans and overdraft facilities, which currently total RM1.2 million. A price cap on dairy products and a new deal with unions that boosted wages resulted in a decline in profit for the company in the second half of 2018 and for the majority of the financial year 2019. Sales increased dramatically throughout both of these years, owing to a strong advertising strategy. The company's bank manager became aware of SSB's declining financial status in early fiscal year 2020 after seeing a ratio analysis from the bank's computer system. This indicated that key ratios extracted from the quarterly management account had fallen below the industry average and were trending downward. The manager forwarded a copy of the analysis and a letter expressing his worry to the SSB's managing director None of the ratios, however, had gone below the levels set in the loan arrangement Three months later, following investigation revealed that the current ratio had gone below the agreement's limit of 2.0. Legally, if the loan is not repaid in full within one month, the bank may take action. The bank manager relayed the analysis to the managing director once more. This time, though, the accompanying letter stated that the bank would want immediate repayment unless it could demonstrate how the financial situation could be addressed. According to the managing director, the current level of sales cannot be sustained without spending RM500,000 on additional equipment and machinery in July 2020. This will necessitate an increase from RM1.2 million to RM1.7 million in loan and overdraft facilities. It is now July 2020. The accounts for the year ended 31 December 2019 are as follows: SSB Statement of Financial Position at 31 December 2019 Fixed assets Land and buildings Plant and machinery Fixtures and fittings Current assets Inventories Trade receivables Cash at bank Current liabilities Trade payables Bank overdraft Net current assets Total assets Less: Current liabilities Non-current liabilities Bank loan Capital and reserves Issued share capital Accumulated profit Other reserves 2019 RM '000 510 430 20 960 3,440 1,620 80 5,140 1,750 590 2,340 2,800 3,760 600 3,160 850 1,630 680 3,160 2018 RM '000 540 490 30 1,060 2,130 1,160 120 3,410 1,050 130 1,180 2,230 3,290 300 2,990 850 1,460 680 2,990 2017 RM '000 200 630 120 950 1,280 1,020 260 2,560 800 800 1,760 2,710 0 2,710 850 1,180 680 2,710 2016 RM '000 260 740 200 1,200 850 680 170 1,700 620 0 620 1,080 2,280 0 2,280 850 750 680 2,280 Swiss Sdn Bhd Income Statement for the year ended 31 December 2019 2019 2018 RM '000 RM '000 Turnover Cost of Sales Gross profit Distribution cost Administration expenses Operating profit Interest payable Profit before tax Tax Net profit Note: depreciation 11,900 9,520 Return on total assets Profit margin 2,380 140 1,780 460 120 340 100 240 510 Industry average ratios for 2017-2019 Gearing (debt equity) Quick ratio Current ratio Inventory turnover Debtor asset turnover Fixed asset turnover Total asset turnover 11,470 9,180 2,290 130 1,560 600 30 570 170 400 430 0.5 1 2.5 6 times 33 13 times 2.6 9.0 % 3.5 % 2017 RM '000 11,050 8,840 2,210 110 1,250 850 0 850 250 600 510 d. If the bank granted the additional loan, could the company pay off the loan by 31 December 2020? Explain. (8 marks) CASE 1 Swiss Sdn Bhd (SSB) produces dairy products and requires seasonal working capital. These were funded mostly through bank loans and overdraft facilities, which currently total RM1.2 million. A price cap on dairy products and a new deal with unions that boosted wages resulted in a decline in profit for the company in the second half of 2018 and for the majority of the financial year 2019. Sales increased dramatically throughout both of these years, owing to a strong advertising strategy. The company's bank manager became aware of SSB's declining financial status in early fiscal year 2020 after seeing a ratio analysis from the bank's computer system. This indicated that key ratios extracted from the quarterly management account had fallen below the industry average and were trending downward. The manager forwarded a copy of the analysis and a letter expressing his worry to the SSB's managing director None of the ratios, however, had gone below the levels set in the loan arrangement Three months later, following investigation revealed that the current ratio had gone below the agreement's limit of 2.0. Legally, if the loan is not repaid in full within one month, the bank may take action. The bank manager relayed the analysis to the managing director once more. This time, though, the accompanying letter stated that the bank would want immediate repayment unless it could demonstrate how the financial situation could be addressed. According to the managing director, the current level of sales cannot be sustained without spending RM500,000 on additional equipment and machinery in July 2020. This will necessitate an increase from RM1.2 million to RM1.7 million in loan and overdraft facilities. It is now July 2020. The accounts for the year ended 31 December 2019 are as follows: SSB Statement of Financial Position at 31 December 2019 Fixed assets Land and buildings Plant and machinery Fixtures and fittings Current assets Inventories Trade receivables Cash at bank Current liabilities Trade payables Bank overdraft Net current assets Total assets Less: Current liabilities Non-current liabilities Bank loan Capital and reserves Issued share capital Accumulated profit Other reserves 2019 RM '000 510 430 20 960 3,440 1,620 80 5,140 1,750 590 2,340 2,800 3,760 600 3,160 850 1,630 680 3,160 2018 RM '000 540 490 30 1,060 2,130 1,160 120 3,410 1,050 130 1,180 2,230 3,290 300 2,990 850 1,460 680 2,990 2017 RM '000 200 630 120 950 1,280 1,020 260 2,560 800 800 1,760 2,710 0 2,710 850 1,180 680 2,710 2016 RM '000 260 740 200 1,200 850 680 170 1,700 620 0 620 1,080 2,280 0 2,280 850 750 680 2,280 Swiss Sdn Bhd Income Statement for the year ended 31 December 2019 2019 2018 RM '000 RM '000 Turnover Cost of Sales Gross profit Distribution cost Administration expenses Operating profit Interest payable Profit before tax Tax Net profit Note: depreciation 11,900 9,520 Return on total assets Profit margin 2,380 140 1,780 460 120 340 100 240 510 Industry average ratios for 2017-2019 Gearing (debt equity) Quick ratio Current ratio Inventory turnover Debtor asset turnover Fixed asset turnover Total asset turnover 11,470 9,180 2,290 130 1,560 600 30 570 170 400 430 0.5 1 2.5 6 times 33 13 times 2.6 9.0 % 3.5 % 2017 RM '000 11,050 8,840 2,210 110 1,250 850 0 850 250 600 510 d. If the bank granted the additional loan, could the company pay off the loan by 31 December 2020? Explain. (8 marks) CASE 1 Swiss Sdn Bhd (SSB) produces dairy products and requires seasonal working capital. These were funded mostly through bank loans and overdraft facilities, which currently total RM1.2 million. A price cap on dairy products and a new deal with unions that boosted wages resulted in a decline in profit for the company in the second half of 2018 and for the majority of the financial year 2019. Sales increased dramatically throughout both of these years, owing to a strong advertising strategy. The company's bank manager became aware of SSB's declining financial status in early fiscal year 2020 after seeing a ratio analysis from the bank's computer system. This indicated that key ratios extracted from the quarterly management account had fallen below the industry average and were trending downward. The manager forwarded a copy of the analysis and a letter expressing his worry to the SSB's managing director None of the ratios, however, had gone below the levels set in the loan arrangement Three months later, following investigation revealed that the current ratio had gone below the agreement's limit of 2.0. Legally, if the loan is not repaid in full within one month, the bank may take action. The bank manager relayed the analysis to the managing director once more. This time, though, the accompanying letter stated that the bank would want immediate repayment unless it could demonstrate how the financial situation could be addressed. According to the managing director, the current level of sales cannot be sustained without spending RM500,000 on additional equipment and machinery in July 2020. This will necessitate an increase from RM1.2 million to RM1.7 million in loan and overdraft facilities. It is now July 2020. The accounts for the year ended 31 December 2019 are as follows: SSB Statement of Financial Position at 31 December 2019 Fixed assets Land and buildings Plant and machinery Fixtures and fittings Current assets Inventories Trade receivables Cash at bank Current liabilities Trade payables Bank overdraft Net current assets Total assets Less: Current liabilities Non-current liabilities Bank loan Capital and reserves Issued share capital Accumulated profit Other reserves 2019 RM '000 510 430 20 960 3,440 1,620 80 5,140 1,750 590 2,340 2,800 3,760 600 3,160 850 1,630 680 3,160 2018 RM '000 540 490 30 1,060 2,130 1,160 120 3,410 1,050 130 1,180 2,230 3,290 300 2,990 850 1,460 680 2,990 2017 RM '000 200 630 120 950 1,280 1,020 260 2,560 800 800 1,760 2,710 0 2,710 850 1,180 680 2,710 2016 RM '000 260 740 200 1,200 850 680 170 1,700 620 0 620 1,080 2,280 0 2,280 850 750 680 2,280 Swiss Sdn Bhd Income Statement for the year ended 31 December 2019 2019 2018 RM '000 RM '000 Turnover Cost of Sales Gross profit Distribution cost Administration expenses Operating profit Interest payable Profit before tax Tax Net profit Note: depreciation 11,900 9,520 Return on total assets Profit margin 2,380 140 1,780 460 120 340 100 240 510 Industry average ratios for 2017-2019 Gearing (debt equity) Quick ratio Current ratio Inventory turnover Debtor asset turnover Fixed asset turnover Total asset turnover 11,470 9,180 2,290 130 1,560 600 30 570 170 400 430 0.5 1 2.5 6 times 33 13 times 2.6 9.0 % 3.5 % 2017 RM '000 11,050 8,840 2,210 110 1,250 850 0 850 250 600 510 d. If the bank granted the additional loan, could the company pay off the loan by 31 December 2020? Explain. (8 marks) CASE 1 Swiss Sdn Bhd (SSB) produces dairy products and requires seasonal working capital. These were funded mostly through bank loans and overdraft facilities, which currently total RM1.2 million. A price cap on dairy products and a new deal with unions that boosted wages resulted in a decline in profit for the company in the second half of 2018 and for the majority of the financial year 2019. Sales increased dramatically throughout both of these years, owing to a strong advertising strategy. The company's bank manager became aware of SSB's declining financial status in early fiscal year 2020 after seeing a ratio analysis from the bank's computer system. This indicated that key ratios extracted from the quarterly management account had fallen below the industry average and were trending downward. The manager forwarded a copy of the analysis and a letter expressing his worry to the SSB's managing director None of the ratios, however, had gone below the levels set in the loan arrangement Three months later, following investigation revealed that the current ratio had gone below the agreement's limit of 2.0. Legally, if the loan is not repaid in full within one month, the bank may take action. The bank manager relayed the analysis to the managing director once more. This time, though, the accompanying letter stated that the bank would want immediate repayment unless it could demonstrate how the financial situation could be addressed. According to the managing director, the current level of sales cannot be sustained without spending RM500,000 on additional equipment and machinery in July 2020. This will necessitate an increase from RM1.2 million to RM1.7 million in loan and overdraft facilities. It is now July 2020. The accounts for the year ended 31 December 2019 are as follows: SSB Statement of Financial Position at 31 December 2019 Fixed assets Land and buildings Plant and machinery Fixtures and fittings Current assets Inventories Trade receivables Cash at bank Current liabilities Trade payables Bank overdraft Net current assets Total assets Less: Current liabilities Non-current liabilities Bank loan Capital and reserves Issued share capital Accumulated profit Other reserves 2019 RM '000 510 430 20 960 3,440 1,620 80 5,140 1,750 590 2,340 2,800 3,760 600 3,160 850 1,630 680 3,160 2018 RM '000 540 490 30 1,060 2,130 1,160 120 3,410 1,050 130 1,180 2,230 3,290 300 2,990 850 1,460 680 2,990 2017 RM '000 200 630 120 950 1,280 1,020 260 2,560 800 800 1,760 2,710 0 2,710 850 1,180 680 2,710 2016 RM '000 260 740 200 1,200 850 680 170 1,700 620 0 620 1,080 2,280 0 2,280 850 750 680 2,280 Swiss Sdn Bhd Income Statement for the year ended 31 December 2019 2019 2018 RM '000 RM '000 Turnover Cost of Sales Gross profit Distribution cost Administration expenses Operating profit Interest payable Profit before tax Tax Net profit Note: depreciation 11,900 9,520 Return on total assets Profit margin 2,380 140 1,780 460 120 340 100 240 510 Industry average ratios for 2017-2019 Gearing (debt equity) Quick ratio Current ratio Inventory turnover Debtor asset turnover Fixed asset turnover Total asset turnover 11,470 9,180 2,290 130 1,560 600 30 570 170 400 430 0.5 1 2.5 6 times 33 13 times 2.6 9.0 % 3.5 % 2017 RM '000 11,050 8,840 2,210 110 1,250 850 0 850 250 600 510 d. If the bank granted the additional loan, could the company pay off the loan by 31 December 2020? Explain. (8 marks) CASE 1 Swiss Sdn Bhd (SSB) produces dairy products and requires seasonal working capital. These were funded mostly through bank loans and overdraft facilities, which currently total RM1.2 million. A price cap on dairy products and a new deal with unions that boosted wages resulted in a decline in profit for the company in the second half of 2018 and for the majority of the financial year 2019. Sales increased dramatically throughout both of these years, owing to a strong advertising strategy. The company's bank manager became aware of SSB's declining financial status in early fiscal year 2020 after seeing a ratio analysis from the bank's computer system. This indicated that key ratios extracted from the quarterly management account had fallen below the industry average and were trending downward. The manager forwarded a copy of the analysis and a letter expressing his worry to the SSB's managing director None of the ratios, however, had gone below the levels set in the loan arrangement Three months later, following investigation revealed that the current ratio had gone below the agreement's limit of 2.0. Legally, if the loan is not repaid in full within one month, the bank may take action. The bank manager relayed the analysis to the managing director once more. This time, though, the accompanying letter stated that the bank would want immediate repayment unless it could demonstrate how the financial situation could be addressed. According to the managing director, the current level of sales cannot be sustained without spending RM500,000 on additional equipment and machinery in July 2020. This will necessitate an increase from RM1.2 million to RM1.7 million in loan and overdraft facilities. It is now July 2020. The accounts for the year ended 31 December 2019 are as follows: SSB Statement of Financial Position at 31 December 2019 Fixed assets Land and buildings Plant and machinery Fixtures and fittings Current assets Inventories Trade receivables Cash at bank Current liabilities Trade payables Bank overdraft Net current assets Total assets Less: Current liabilities Non-current liabilities Bank loan Capital and reserves Issued share capital Accumulated profit Other reserves 2019 RM '000 510 430 20 960 3,440 1,620 80 5,140 1,750 590 2,340 2,800 3,760 600 3,160 850 1,630 680 3,160 2018 RM '000 540 490 30 1,060 2,130 1,160 120 3,410 1,050 130 1,180 2,230 3,290 300 2,990 850 1,460 680 2,990 2017 RM '000 200 630 120 950 1,280 1,020 260 2,560 800 800 1,760 2,710 0 2,710 850 1,180 680 2,710 2016 RM '000 260 740 200 1,200 850 680 170 1,700 620 0 620 1,080 2,280 0 2,280 850 750 680 2,280 Swiss Sdn Bhd Income Statement for the year ended 31 December 2019 2019 2018 RM '000 RM '000 Turnover Cost of Sales Gross profit Distribution cost Administration expenses Operating profit Interest payable Profit before tax Tax Net profit Note: depreciation 11,900 9,520 Return on total assets Profit margin 2,380 140 1,780 460 120 340 100 240 510 Industry average ratios for 2017-2019 Gearing (debt equity) Quick ratio Current ratio Inventory turnover Debtor asset turnover Fixed asset turnover Total asset turnover 11,470 9,180 2,290 130 1,560 600 30 570 170 400 430 0.5 1 2.5 6 times 33 13 times 2.6 9.0 % 3.5 % 2017 RM '000 11,050 8,840 2,210 110 1,250 850 0 850 250 600 510 d. If the bank granted the additional loan, could the company pay off the loan by 31 December 2020? Explain. (8 marks)

Expert Answer:

Answer rating: 100% (QA)

Solution As per managing director by giving entre loan the company able to maintai... View the full answer

Related Book For

Posted Date:

Students also viewed these finance questions

-

Consider the following events related Mr. Masood, the owner of a retail shop in Ibri. 1 Masood gifted a watch to his staff Ms. Zainab on the occasion of her marriage. 2 Paid rent for the staff...

-

Office supplies were sold by Janer's cleaning service at cost to another repair shop, with cash received. Which of the following entries for Janer's Cleaning Service records this transaction? 1.Dr...

-

a Retired bonds payable at maturity date by issuing common shares 143000 b Sold the longterm investments for cash c Sold plant assets for cash cost 554400 twothirds depreciated d Purchased plant...

-

Suppose that In Example 18.6 the electrical firm does not have enough prior information regarding the population mean length of life to be able to assume a normal distribution for p. The firm...

-

At the end of the spring semester, the Dean of Students sent a survey to the entire freshman class. One question asked the students how much weight they had gained or lost since the beginning of the...

-

The working papers pertaining to the auditor's study of internal accounting control include the following preliminary evaluation: Up to the point at which the prenumbered sales invoices are prepared,...

-

The Buffalo Insurance Agency received the following notes during 2010: Requirements 1. Identifying each note by number, compute interest using a 360-day year, and determine the due date and maturity...

-

Use the data in the following table to a. Prepare a frequency distribution of the respondents ages b. Cross-tabulate the respondents genders with cola preference c. Identify anyoutliers Weekly Unit...

-

Let f(x)=-3x ln x f'(x) = '(e) =

-

Consider the two processes shown in Table 8E.1 (the sample size n = 5). Specifications are at 100 ± 10. Calculate Cp, Cpk, and Cpm and interpret these ratios. Which process would you prefer to...

-

Al's Aluminum Company sells $1 million worth of aluminum to Shiny Foil Company, which uses the aluminum to make aluminum foil. Shiny Foil Company sells $3 million worth of aluminum foil as a final...

-

The points (-9, -1) and (7,7) are the endpoints of the diameter of a circle. Find the length of the radius of the circle. The length of the radius is (Round to the nearest hundredth as needed.)

-

Apollo Data Systems is considering a promotional campaign that will increase annual credit sales by $684,000. The company has a 60% cost of goods sold and will require investments in accounts...

-

Paul Dargis has analyzed five stocks and estimated the dividends they will pay next year as well as their prices at the end of the year. His projections are shown below. Projected Stock Stock Current...

-

Use the following selected account balances of Delray Manufacturing for the year ended December 31. Sales Raw materials inventory, beginning Work in process inventory, beginning Finished goods...

-

A disoriented physics professor drives 3.18 km north, then 4.72 km west, and then 1.61 km south. Find the magnitude of the resultant displacement of this professor. Express your answer in kilometers....

-

During the initial try-in of a three-unit fixed dental prosthesis (bridge), the prosthesis fits the prepared teeth perfectly and appears to be retained on the teeth so tenaciously that removal...

-

Consider the sections of two circuits illustrated above. Select True or False for all statements.After connecting a and b to a battery, the voltage across R1 always equals the voltage across R2.Rcd...

-

A manager at an airline raised concerns about the airlines pay practices. She also complained that the performance appraisal process discriminated against female employees. After a number of run-ins...

-

A fifty-three-year old director of an assisted living facility was terminated. Top managers regularly made statements such as Silver Oak should be a youth oriented company, there was no room for dead...

-

The married owner of a company touched and kissed a female salesperson at work, made comments about oral sex, and suggested that they be alone together. A few months later the woman began making...

-

The state of stress stress at a critical point on a thin steel shell is shown. Determine if yielding has occurred using the maximum distortion energy theory. The yield stress for the steel is...

-

The state of strain at the point on the bracket has components of \(\epsilon_{x}=350\left(10^{-6} ight), \quad \epsilon_{y}=-860\left(10^{-6} ight)\), \(\gamma_{x y}=250\left(10^{-6} ight)\). Use the...

-

The state of strain at the point on the bracket has components of \(\epsilon_{x}=-130\left(10^{-6} ight), \quad \epsilon_{y}=280\left(10^{-6} ight)\), \(\gamma_{x y}=75\left(10^{-6} ight)\). Use the...

Study smarter with the SolutionInn App