ABC Ltd is listed on the JSE Limited with a 28 February year end. The ABC...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

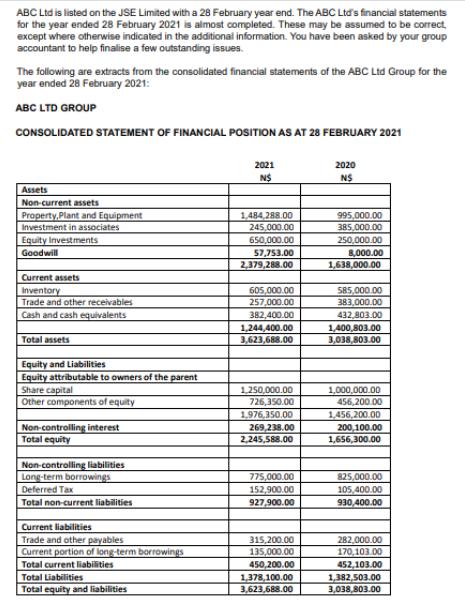

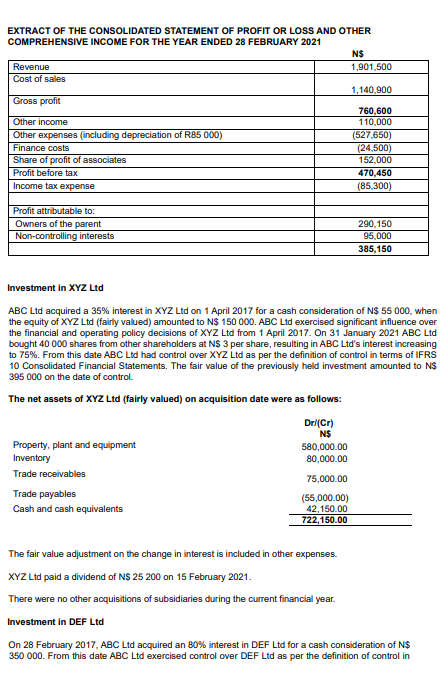

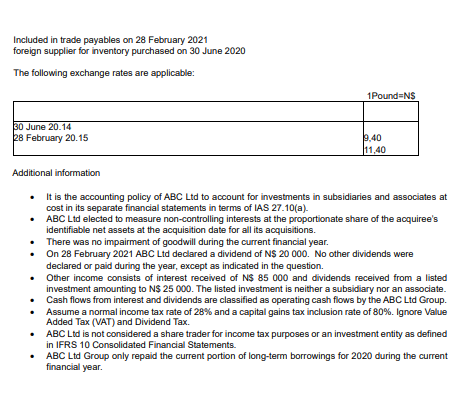

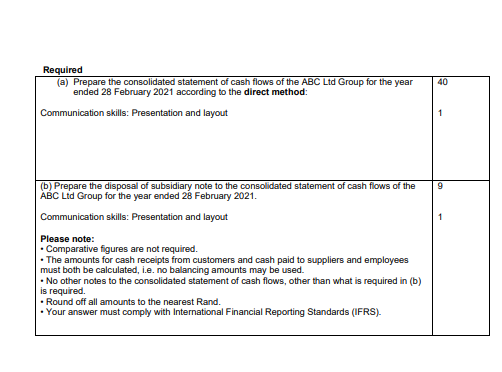

ABC Ltd is listed on the JSE Limited with a 28 February year end. The ABC Ltd's financial statements for the year ended 28 February 2021 is almost completed. These may be assumed to be correct, except where otherwise indicated in the additional information. You have been asked by your group accountant to help finalise a few outstanding issues. The following are extracts from the consolidated financial statements of the ABC Ltd Group for the year ended 28 February 2021: ABC LTD GROUP CONSOLIDATED STATEMENT OF FINANCIAL POSITION AS AT 28 FEBRUARY 2021 Assets Non-current assets Property Plant and Equipment Investment in associates Equity Investments Goodwill Current assets Inventory Trade and other receivables Cash and cash equivalents Total assets Equity and Liabilities Equity attributable to owners of the parent Share capital Other components of equity Non-controlling interest Total equity Non-controlling liabilities Long-term borrowings Deferred Tax Total non-current liabilities Current liabilities Trade and other payables Current portion of long-term borrowings Total current liabilities Total Liabilities Total equity and liabilities 2021 N$ 1,484,288.00 245,000.00 650,000.00 57,753.00 2,379,288.00 605,000.00 257,000.00 382,400.00 1,244,400.00 3,623,688.00 1,250,000.00 726,350.00 1,976,350.00 269,238.00 2,245,588.00 775,000.00 152,900.00 927,900.00 315,200.00 135,000.00 450,200.00 1,378,100.00 3,623,688.00 2020 NS 995,000.00 385,000.00 250,000.00 8,000.00 1,638,000.00 585,000.00 383,000.00 432,803.00 1,400,803.00 3,038,803.00 1,000,000.00 456,200.00 1,456,200.00 200,100.00 1,656,300.00 825,000.00 105,400.00 930,400.00 282,000.00 170,103.00 452,103.00 1,382,503.00 3,038,803.00 EXTRACT OF THE CONSOLIDATED STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME FOR THE YEAR ENDED 28 FEBRUARY 2021 Revenue Cost of sales Gross profit Other income Other expenses (including depreciation of R85 000) Finance costs Share of profit of associates Profit before tax Income tax expense Profit attributable to: Owners of the parent Non-controlling interests Property, plant and equipment Inventory Trade receivables Trade payables Cash and cash equivalents Dri(Cr) N$ 580,000.00 80,000.00 75,000.00 (55,000.00) 42,150.00 722,150.00 N$ 1,901,500 Investment in XYZ Ltd ABC Ltd acquired a 35% interest in XYZ Ltd on 1 April 2017 for a cash consideration of N$ 55 000, when the equity of XYZ Ltd (fairly valued) amounted to N$ 150 000. ABC Ltd exercised significant influence over the financial and operating policy decisions of XYZ Ltd from 1 April 2017. On 31 January 2021 ABC Ltd bought 40 000 shares from other shareholders at N$ 3 per share, resulting in ABC Ltd's interest increasing to 75%. From this date ABC Ltd had control over XYZ Ltd as per the definition of control in terms of IFRS 10 Consolidated Financial Statements. The fair value of the previously held investment amounted to N$ 395 000 on the date of control. The net assets of XYZ Ltd (fairly valued) on acquisition date were as follows: The fair value adjustment on the change in interest is included in other expenses. XYZ Ltd paid a dividend of N$ 25 200 on 15 February 2021. There were no other acquisitions of subsidiaries during the current financial year. Investment in DEF Ltd 1,140,900 760,600 110,000 (527,650) (24,500) 152,000 470,450 (85,300) 290,150 95,000 385,150 On 28 February 2017, ABC Ltd acquired an 80% interest in DEF Ltd for a cash consideration of N$ 350 000. From this date ABC Ltd exercised control over DEF Ltd as per the definition of control in Included in trade payables on 28 February 2021 foreign supplier for inventory purchased on 30 June 2020 The following exchange rates are applicable: 30 June 20.14 28 February 20.15 1Pound=N$ 9,40 11,40 Additional information • It is the accounting policy of ABC Ltd to account for investments in subsidiaries and associates at cost in its separate financial statements in terms of IAS 27.10(a). ABC Ltd elected to measure non-controlling interests at the proportionate share of the acquiree's identifiable net assets at the acquisition date for all its acquisitions. There was no impairment of goodwill during the current financial year. On 28 February 2021 ABC Ltd declared a dividend of N$ 20 000. No other dividends were declared or paid during the year, except as indicated in the question. Other income consists of interest received of N$ 85 000 and dividends received from a listed investment amounting to N$ 25 000. The listed investment is neither a subsidiary nor an associate. Cash flows from interest and dividends are classified as operating cash flows by the ABC Ltd Group. Assume a normal income tax rate of 28% and a capital gains tax inclusion rate of 80%. Ignore Value Added Tax (VAT) and Dividend Tax. ABC Ltd is not considered a share trader for income tax purposes or an investment entity as defined in IFRS 10 Consolidated Financial Statements. • ABC Ltd Group only repaid the current portion of long-term borrowings for 2020 during the current financial year. Required (a) Prepare the consolidated statement of cash flows of the ABC Ltd Group for the year ended 28 February 2021 according to the direct method: Communication skills: Presentation and layout (b) Prepare the disposal of subsidiary note to the consolidated statement of cash flows of the ABC Ltd Group for the year ended 28 February 2021. Communication skills: Presentation and layout Please note: • Comparative figures are not required. • The amounts for cash receipts from customers and cash paid to suppliers and employees must both be calculated, i.e. no balancing amounts may be used. • No other notes to the consolidated statement of cash flows, other than what is required in (b) is required. • Round off all amounts to the nearest Rand. • Your answer must comply with International Financial Reporting Standards (IFRS). 40 9 ABC Ltd is listed on the JSE Limited with a 28 February year end. The ABC Ltd's financial statements for the year ended 28 February 2021 is almost completed. These may be assumed to be correct, except where otherwise indicated in the additional information. You have been asked by your group accountant to help finalise a few outstanding issues. The following are extracts from the consolidated financial statements of the ABC Ltd Group for the year ended 28 February 2021: ABC LTD GROUP CONSOLIDATED STATEMENT OF FINANCIAL POSITION AS AT 28 FEBRUARY 2021 Assets Non-current assets Property Plant and Equipment Investment in associates Equity Investments Goodwill Current assets Inventory Trade and other receivables Cash and cash equivalents Total assets Equity and Liabilities Equity attributable to owners of the parent Share capital Other components of equity Non-controlling interest Total equity Non-controlling liabilities Long-term borrowings Deferred Tax Total non-current liabilities Current liabilities Trade and other payables Current portion of long-term borrowings Total current liabilities Total Liabilities Total equity and liabilities 2021 N$ 1,484,288.00 245,000.00 650,000.00 57,753.00 2,379,288.00 605,000.00 257,000.00 382,400.00 1,244,400.00 3,623,688.00 1,250,000.00 726,350.00 1,976,350.00 269,238.00 2,245,588.00 775,000.00 152,900.00 927,900.00 315,200.00 135,000.00 450,200.00 1,378,100.00 3,623,688.00 2020 NS 995,000.00 385,000.00 250,000.00 8,000.00 1,638,000.00 585,000.00 383,000.00 432,803.00 1,400,803.00 3,038,803.00 1,000,000.00 456,200.00 1,456,200.00 200,100.00 1,656,300.00 825,000.00 105,400.00 930,400.00 282,000.00 170,103.00 452,103.00 1,382,503.00 3,038,803.00 EXTRACT OF THE CONSOLIDATED STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME FOR THE YEAR ENDED 28 FEBRUARY 2021 Revenue Cost of sales Gross profit Other income Other expenses (including depreciation of R85 000) Finance costs Share of profit of associates Profit before tax Income tax expense Profit attributable to: Owners of the parent Non-controlling interests Property, plant and equipment Inventory Trade receivables Trade payables Cash and cash equivalents Dri(Cr) N$ 580,000.00 80,000.00 75,000.00 (55,000.00) 42,150.00 722,150.00 N$ 1,901,500 Investment in XYZ Ltd ABC Ltd acquired a 35% interest in XYZ Ltd on 1 April 2017 for a cash consideration of N$ 55 000, when the equity of XYZ Ltd (fairly valued) amounted to N$ 150 000. ABC Ltd exercised significant influence over the financial and operating policy decisions of XYZ Ltd from 1 April 2017. On 31 January 2021 ABC Ltd bought 40 000 shares from other shareholders at N$ 3 per share, resulting in ABC Ltd's interest increasing to 75%. From this date ABC Ltd had control over XYZ Ltd as per the definition of control in terms of IFRS 10 Consolidated Financial Statements. The fair value of the previously held investment amounted to N$ 395 000 on the date of control. The net assets of XYZ Ltd (fairly valued) on acquisition date were as follows: The fair value adjustment on the change in interest is included in other expenses. XYZ Ltd paid a dividend of N$ 25 200 on 15 February 2021. There were no other acquisitions of subsidiaries during the current financial year. Investment in DEF Ltd 1,140,900 760,600 110,000 (527,650) (24,500) 152,000 470,450 (85,300) 290,150 95,000 385,150 On 28 February 2017, ABC Ltd acquired an 80% interest in DEF Ltd for a cash consideration of N$ 350 000. From this date ABC Ltd exercised control over DEF Ltd as per the definition of control in Included in trade payables on 28 February 2021 foreign supplier for inventory purchased on 30 June 2020 The following exchange rates are applicable: 30 June 20.14 28 February 20.15 1Pound=N$ 9,40 11,40 Additional information • It is the accounting policy of ABC Ltd to account for investments in subsidiaries and associates at cost in its separate financial statements in terms of IAS 27.10(a). ABC Ltd elected to measure non-controlling interests at the proportionate share of the acquiree's identifiable net assets at the acquisition date for all its acquisitions. There was no impairment of goodwill during the current financial year. On 28 February 2021 ABC Ltd declared a dividend of N$ 20 000. No other dividends were declared or paid during the year, except as indicated in the question. Other income consists of interest received of N$ 85 000 and dividends received from a listed investment amounting to N$ 25 000. The listed investment is neither a subsidiary nor an associate. Cash flows from interest and dividends are classified as operating cash flows by the ABC Ltd Group. Assume a normal income tax rate of 28% and a capital gains tax inclusion rate of 80%. Ignore Value Added Tax (VAT) and Dividend Tax. ABC Ltd is not considered a share trader for income tax purposes or an investment entity as defined in IFRS 10 Consolidated Financial Statements. • ABC Ltd Group only repaid the current portion of long-term borrowings for 2020 during the current financial year. Required (a) Prepare the consolidated statement of cash flows of the ABC Ltd Group for the year ended 28 February 2021 according to the direct method: Communication skills: Presentation and layout (b) Prepare the disposal of subsidiary note to the consolidated statement of cash flows of the ABC Ltd Group for the year ended 28 February 2021. Communication skills: Presentation and layout Please note: • Comparative figures are not required. • The amounts for cash receipts from customers and cash paid to suppliers and employees must both be calculated, i.e. no balancing amounts may be used. • No other notes to the consolidated statement of cash flows, other than what is required in (b) is required. • Round off all amounts to the nearest Rand. • Your answer must comply with International Financial Reporting Standards (IFRS). 40 9

Expert Answer:

Answer rating: 100% (QA)

Sure Lets go through the calculations step by step 1 Calculate the fair value adjustment for the cha... View the full answer

Related Book For

Modern Advanced Accounting in Canada

ISBN: 978-1259087554

8th edition

Authors: Hilton Murray, Herauf Darrell

Posted Date:

Students also viewed these accounting questions

-

What are the ethical considerations surrounding pharmacological interventions for stress management, and how can interdisciplinary collaboration facilitate responsible prescribing practices?

-

You are an investment analyst. A client of yours, Mr A, owns 3.5% of the share capital of Price. Price is a listed company and prepares financial statements in accordance with International...

-

The financial statements of JJ Ltd and KK Ltd for the year to 30 June 2018 are shown below: Statements of comprehensive income for the year to 30 June 2018. Statements of financial position as at 30...

-

Determine the real roots of (x) = - 1 + 5.5x 4x2 + 0.5x3: (a) Graphically and (b) Using the Newton-Raphson method to within s = 0.01%.

-

Let l = ∫4 f(x) dx, where is the function whose graph is shown. (a) Use the graph to find L2, R2 and M2. (b) Are these underestimates or overestimates of l? (c) Use the graph to find T2. How does...

-

Describe and differentiate between planning, control, and decision - making functions.

-

Differentiate technology from methodology and from method. Can you come up with an example that differentiates these concepts in a specific context, perhaps software development?

-

Pike Seafood Company purchases lobsters and processes them into tails and flakes. It sells the lobster tails for $20 per pound and the flakes for $15 per pound. On average, 100 pounds of lobster are...

-

Superior Company provided the following data for the year ended December 31 (all raw materials are used in production as direct materials): Selling expenses Purchases of raw materials Direct labor...

-

Jennifer's condo is worth $400,000. She owes $300,000 on her 6% fixed-rate mortgage compounds semiannually that have three years remaining in their term. Jennifer pays $2,245 per month towards it....

-

On July 25 the company paid the secretary. Her deductions are the same for each payroll. Her deductions include OASDI, HI and FIT of $105. The company FUTA rate is 0.8% (and the secretary has met the...

-

In ABC, what are the trade-offs made in choosing among transaction, duration and intensity activity cost drivers.

-

What if the counseling needed for a student to benefit from education is provided in the residential setting by a psychiatrist? Is this a medical expense to be paid by the parents?

-

How are cost driver rates selected in activity-based costing system?

-

How do activity-based costing systems avoid distortions in tracing costs to products?

-

Emily is 15. Until recently, she had no apparent serious problems. Last year, however, her parents got divorced, she broke up with her boyfriend, and her grades began to suffer. Emily lives with her...

-

After months of weighing their options, the management team has decided to increase all park employee wages from the currently blended rate of $11.50 per hour to $15 per hour, regardless of their...

-

Is that Yelp review real or fake? The article A Framework for Fake Review Detection in Online Consumer Electronics Retailers (Information Processing and Management 2019: 12341244) tested five...

-

What guidelines does the Handbook provide for pledges received by an NFPO?

-

You, the CPA, an audit senior at Grey & Co., Chartered Professional Accountants, are in charge of this year's audit of Plex-Fame Corporation (PFC). PFC is a rapidly expanding, diversified, and...

-

Explain how the definitions of assets and liabilities can be used to support the consolidation of special-purpose entities.

-

You have two regions, A and B, of differently doped silicon, with the regions joined together to make a continuous silicon crystal. When the positive terminal of a battery is connected to region...

-

In Figure P32.33, what combinations of positive bias (input signals) A, B, C, D allow the light bulb to light up? Data from Figure P32.33 A B OR JOR AND D

-

Suppose a transistor consists of a very narrow \(p\)-type material sandwiched between two very wide regions of \(n\)-type material. (a) Is the charge on the \(p\)-type region positive or negative,...

Study smarter with the SolutionInn App