10. Kesler, Inc. estimates the cost of its physical inventory at March 31 for use in...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

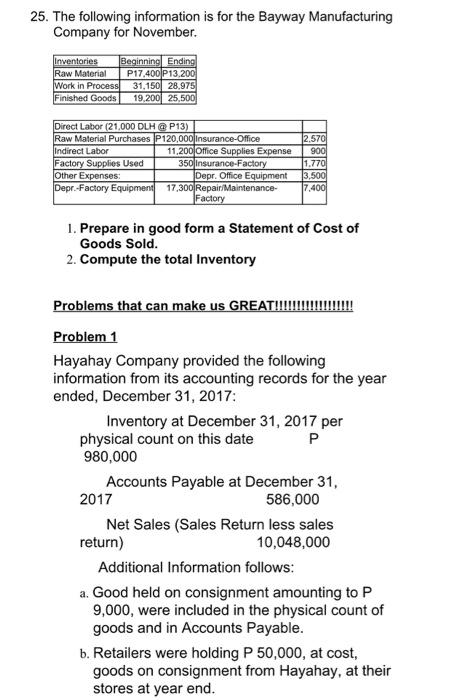

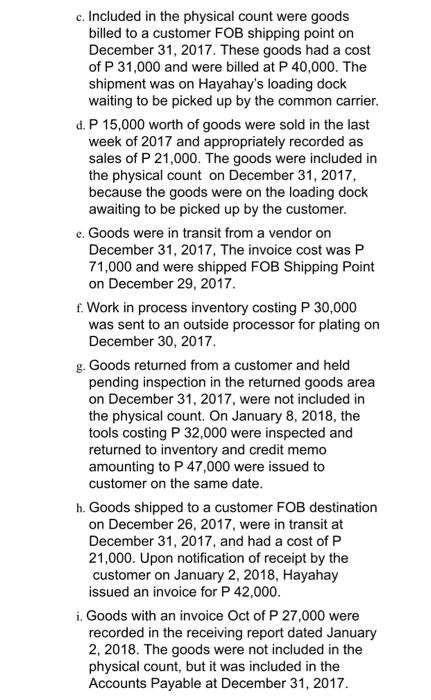

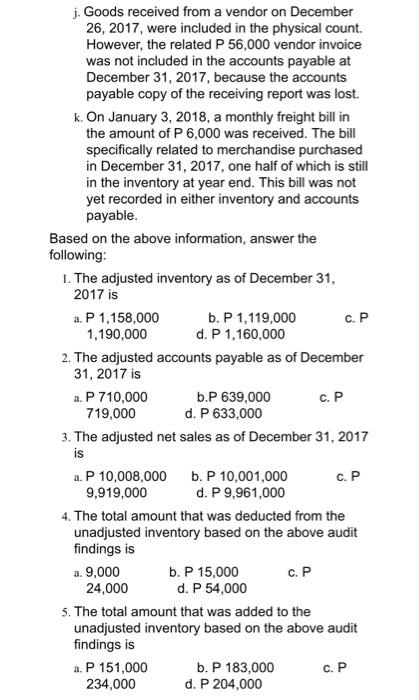

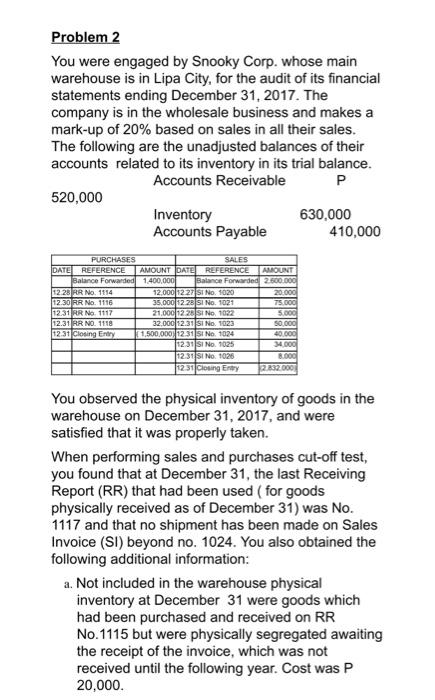

10. Kesler, Inc. estimates the cost of its physical inventory at March 31 for use in an interim financial statement. The rate of markup on cost is 25%. The following account balances are available: P220,000 Inventory, March 1 Purchases Purchase returns 172,000 8,000 Sales during March 300,000 What is the estimate of the cost of inventory at March 31 would be? 11. On January 1, 2010, the merchandise inventory of Glaus, Inc. was P800,000. During 2010 Glaus purchased P1,600,000 of merchandise and recorded sales of P2,000,000. The gross profit rate on these sales was 25%. What is the merchandise inventory of Glaus at December 31, 2010? 12. For 2010, cost of goods available for sale for Tate Corporation was P900,000. The gross profit rate was 20%. Sales for the year were P800,000. What was the amount of the ending inventory? 13. On April 15 of the current year, a fire destroyed the entire uninsured inventory of a retail store. The following data are available: Sales, January 1 through April 15 50,000 Inventory, January 1 Purchases, P300,000 January 1 through April 15 250,000 Markup on cost 25% The amount of the inventory loss is estimated to be 14. The sales price for a product provides a gross profit of 25% of sales price. What is the gross profit as a percentage of cost? 15. Gamma Ray Corp. has annual sales totaling P650,000 and an average gross profit of 20% of cost. What is the peso amount of the gross profit? 16. On August 31, a hurricane destroyed a retail location of Vinny's Clothier including the entire inventory on hand at the location. The inventory on hand as of June 30 totaled P320,000. From June 30 until the time of the hurricane, the company made purchases of P85,000 and had sales of P250,000. Assuming the rate of gross profit to selling price is 40%, what is the approximate value of the inventory that was destroyed? 17. On October 31, a fire destroyed PH Inc.'s entire retail inventory. The inventory on hand as of January 1 totaled P680,000. From January 1 through the time of the fire, the company made purchases of P165,000 and had sales of P360,000. Assuming the rate of gross profit to selling price is 40%, what is the approximate value of the inventory that was destroyed? 18. On March 15, a fire destroyed Interlock Company's entire retail inventory. The inventory on hand as of January 1 totaled P1,650,000. From January 1 through the time of the fire, the company made purchases of P683,000, incurred freight-in of P78,000, and had sales of P1,210,000. Assuming the rate of gross profit to selling price is 30%, what is the approximate value of the inventory that was destroyed? 19. Crane Sales Company uses the retail inventory method to value its merchandise inventory. The following information is available for the current year: Cost Beginning inventory Purchases Freight-in 20. Net markups Net markdowns Employee discounts Sales - 2,500 145,000 Beginning inventory Purchases Freight-in 224,000 6,000 Net markups Net markdowns Sales 205,000 If the ending inventory is to be valued at the lower-of- cost-or-net realizable value, what is the cost to retail ratio? Use the following information for questions 20 through 22. The following data concerning the retail inventory method are taken from the financial records of Welch Company. Cost Retail - Retail - P 30,000 P 50,000 200,000 8,500 10,000 20,000 1,000 P 49,000 P 70,000 320,000 14,000 336,000 What is the ending inventory at retail should be? 21 If the ending inventory is to be valued at approximately the lower of cost or market, the calculation of the cost to retail ratio should be based on what amount of goods available for sale at (1) cost and (2) retail? 19. Crane Sales Company uses the retail inventory method to value its merchandise inventory. The following information is available for the current year: Cost Beginning inventory Purchases Freight-in 20. Net markups Net markdowns Employee discounts Sales - 2,500 145,000 Beginning inventory Purchases Freight-in 224,000 6,000 Net markups Net markdowns Sales 205,000 If the ending inventory is to be valued at the lower-of- cost-or-net realizable value, what is the cost to retail ratio? Use the following information for questions 20 through 22. The following data concerning the retail inventory method are taken from the financial records of Welch Company. Cost Retail - Retail - P 30,000 P 50,000 200,000 8,500 10,000 20,000 1,000 P 49,000 P 70,000 320,000 14,000 336,000 What is the ending inventory at retail should be? 21 If the ending inventory is to be valued at approximately the lower of cost or market, the calculation of the cost to retail ratio should be based on what amount of goods available for sale at (1) cost and (2) retail? 25. The following information is for the Bayway Manufacturing Company for November. Beginning Ending Inventories Raw Material P17,400 P13,200 Work in Process 31,150 28,975 Finished Goods 19,200 25,500 Direct Labor (21,000 DLH @ P13) Raw Material Purchases P120,000 Insurance-Office Indirect Labor Factory Supplies Used Other Expenses: Depr.-Factory Equipment 11,200 Office Supplies Expense 350 Insurance-Factory Depr. Office Equipment 17,300 Repair/Maintenance- Factory 1. Prepare in good form a Statement of Cost of Goods Sold. 2. Compute the total Inventory 2,570 900 Problems that can make us GREAT!!!!! Problem 1 Hayahay Company provided the following information from its accounting records for the year ended, December 31, 2017: physical count on this date 980,000 1,770 3,500 7,400 Inventory at December 31, 2017 per P 2017 Accounts Payable at December 31, 586,000 return) Net Sales (Sales Return less sales 10,048,000 Additional Information follows: a. Good held on consignment amounting to P 9,000, were included in the physical count of goods and in Accounts Payable. b. Retailers were holding P 50,000, at cost, goods on consignment from Hayahay, at their stores at year end. c. Included in the physical count were goods billed to a customer FOB shipping point on December 31, 2017. These goods had a cost of P 31,000 and were billed at P 40,000. The shipment was on Hayahay's loading dock waiting to be picked up by the common carrier. d. P 15,000 worth of goods were sold in the last week of 2017 and appropriately recorded as sales of P 21,000. The goods were included in the physical count on December 31, 2017, because the goods were on the loading dock awaiting to be picked up by the customer. e. Goods were in transit from a vendor on December 31, 2017, The invoice cost was P 71,000 and were shipped FOB Shipping Point on December 29, 2017. f. Work in process inventory costing P 30,000 was sent to an outside processor for plating on December 30, 2017. g. Goods returned from a customer and held pending inspection in the returned goods area on December 31, 2017, were not included in the physical count. On January 8, 2018, the tools costing P 32,000 were inspected and returned to inventory and credit memo amounting to P 47,000 were issued to customer on the same date. h. Goods shipped to a customer FOB destination on December 26, 2017, were in transit at December 31, 2017, and had a cost of P 21,000. Upon notification of receipt by the customer on January 2, 2018, Hayahay issued an invoice for P 42,000. i. Goods with an invoice Oct of P 27,000 were recorded in the receiving report dated January 2, 2018. The goods were not included in the physical count, but it was included in the Accounts Payable at December 31, 2017. j. Goods received from a vendor on December 26, 2017, were included in the physical count. However, the related P 56,000 vendor invoice was not included in the accounts payable at December 31, 2017, because the accounts payable copy of the receiving report was lost. k. On January 3, 2018, a monthly freight bill in the amount of P 6,000 was received. The bill specifically related to merchandise purchased in December 31, 2017, one half of which is still in the inventory at year end. This bill was not yet recorded in either inventory and accounts payable. Based on the above information, answer the following: 1. The adjusted inventory as of December 31, 2017 is a. P 1,158,000 1,190,000 a. P 710,000 719,000 2. The adjusted accounts payable as of December 31, 2017 is a. 9,000 b. P 1,119,000 24,000 d. P 1,160,000 a. P 151,000 234,000 b.P 639,000 d. P 633,000 3. The adjusted net sales as of December 31, 2017 is a. P 10,008,000 9,919,000 4. The total amount that was deducted from the unadjusted inventory based on the above audit findings is b. P 10,001,000 d. P 9,961,000 b. P 15,000 d. P 54,000 b. P 183,000 c. P c. P c. P d. P 204,000 5. The total amount that was added to the unadjusted inventory based on the above audit findings is c. P c. P Problem 2 You were engaged by Snooky Corp. whose main warehouse is in Lipa City, for the audit of its financial statements ending December 31, 2017. The company is in the wholesale business and makes a mark-up of 20% based on sales in all their sales. The following are the unadjusted balances of their accounts related to its inventory in its trial balance. Accounts Receivable P 520,000 PURCHASES DATE REFERENCE Balance Forwarded 12.28 RR No. 1114 12.30 RR No. 1116 12.31 RR No. 1117 12.31 RR NO. 1118 12.31 Closing Entry Inventory Accounts Payable SALES AMOUNT DATE REFERENCE AMOUNT 1,400,000 Balance Forwarded 2.600.000 12.000 12.27 SI No. 1020 35,000 12.28 SI No. 1021 21,000 12 28 SI No. 1022 32.000 12.31 SI No. 1023 (1,500,000 12.31 SI No. 1024 12.31 SI No. 1025 12.31 SI No: 1026 12.31 Closing Entry 20.000 75.000 5,000 50,000 40,000 34,000 8.000 2.832.000 630,000 410,000 You observed the physical inventory of goods in the warehouse on December 31, 2017, and were satisfied that it was properly taken. When performing sales and purchases cut-off test, you found that at December 31, the last Receiving Report (RR) that had been used (for goods physically received as of December 31) was No. 1117 and that no shipment has been made on Sales Invoice (SI) beyond no. 1024. You also obtained the following additional information: a. Not included in the warehouse physical inventory at December 31 were goods which had been purchased and received on RR No.1115 but were physically segregated awaiting the receipt of the invoice, which was not received until the following year. Cost was P 20,000. b. On the evening of December 31, there were two trucks in the company's warehouse. Goods inside the trucks were not included in the physical count as of December 31: 1. Truck No. APC 321 was unloaded on January 2 of the following year and received on RR. No. 1117. The goods were shipped FOB Destination. 2. Truck No. ULI 341 was loaded and sealed on December 31 but left the company premises only on January 2. This order was sold per Sales Invoice No. 1024. The goods were shipped FOB Shipping Point. c. Sales Invoice no. 1021 pertains to a shipment which was temporarily stranded at December 31 enroute to a client's customer. The client's customer received the goods which were shipped FOB Lipa. d. Enroute to the client on December 31 was a truckload of goods from supplier in Batangas were received on RR No. 1119. The goods were shipped FOB Batangas, and freight of P 2,000 was prepaid by the said supplier. Invocie price excluding freight amounted to P 54,000. 1. The correct amount of sales for the year ended, December 31, 2017 is a. P 2,750,000 P 2,675,000 b. P 2,742,000 d. P 2,667,000 a. P 1,488,000 P 1,522,000 2. The correct amount of purchases for the year ended, December 31, 2017 is C. b. P 1,542,000 d. P 1,574,000 C. 3. The correct inventory balance as of December 31, 2017 is a. P 737,000 757,000 a. P 446,000 363,000 b. P 739,000 d. P 759,000 4. The correct Accounts Receivable balance as of December 31, 2017 is a. P 454,000 452,000 b. P 478,000 d. P 438,000 c. P 5. The correct Accounts Payable balance as of December 31, 2017 is b. P 434,000 d. P 432,000 c. P c. P 10. Kesler, Inc. estimates the cost of its physical inventory at March 31 for use in an interim financial statement. The rate of markup on cost is 25%. The following account balances are available: P220,000 Inventory, March 1 Purchases Purchase returns 172,000 8,000 Sales during March 300,000 What is the estimate of the cost of inventory at March 31 would be? 11. On January 1, 2010, the merchandise inventory of Glaus, Inc. was P800,000. During 2010 Glaus purchased P1,600,000 of merchandise and recorded sales of P2,000,000. The gross profit rate on these sales was 25%. What is the merchandise inventory of Glaus at December 31, 2010? 12. For 2010, cost of goods available for sale for Tate Corporation was P900,000. The gross profit rate was 20%. Sales for the year were P800,000. What was the amount of the ending inventory? 13. On April 15 of the current year, a fire destroyed the entire uninsured inventory of a retail store. The following data are available: Sales, January 1 through April 15 50,000 Inventory, January 1 Purchases, P300,000 January 1 through April 15 250,000 Markup on cost 25% The amount of the inventory loss is estimated to be 14. The sales price for a product provides a gross profit of 25% of sales price. What is the gross profit as a percentage of cost? 15. Gamma Ray Corp. has annual sales totaling P650,000 and an average gross profit of 20% of cost. What is the peso amount of the gross profit? 16. On August 31, a hurricane destroyed a retail location of Vinny's Clothier including the entire inventory on hand at the location. The inventory on hand as of June 30 totaled P320,000. From June 30 until the time of the hurricane, the company made purchases of P85,000 and had sales of P250,000. Assuming the rate of gross profit to selling price is 40%, what is the approximate value of the inventory that was destroyed? 17. On October 31, a fire destroyed PH Inc.'s entire retail inventory. The inventory on hand as of January 1 totaled P680,000. From January 1 through the time of the fire, the company made purchases of P165,000 and had sales of P360,000. Assuming the rate of gross profit to selling price is 40%, what is the approximate value of the inventory that was destroyed? 18. On March 15, a fire destroyed Interlock Company's entire retail inventory. The inventory on hand as of January 1 totaled P1,650,000. From January 1 through the time of the fire, the company made purchases of P683,000, incurred freight-in of P78,000, and had sales of P1,210,000. Assuming the rate of gross profit to selling price is 30%, what is the approximate value of the inventory that was destroyed? 19. Crane Sales Company uses the retail inventory method to value its merchandise inventory. The following information is available for the current year: Cost Beginning inventory Purchases Freight-in 20. Net markups Net markdowns Employee discounts Sales - 2,500 145,000 Beginning inventory Purchases Freight-in 224,000 6,000 Net markups Net markdowns Sales 205,000 If the ending inventory is to be valued at the lower-of- cost-or-net realizable value, what is the cost to retail ratio? Use the following information for questions 20 through 22. The following data concerning the retail inventory method are taken from the financial records of Welch Company. Cost Retail - Retail - P 30,000 P 50,000 200,000 8,500 10,000 20,000 1,000 P 49,000 P 70,000 320,000 14,000 336,000 What is the ending inventory at retail should be? 21 If the ending inventory is to be valued at approximately the lower of cost or market, the calculation of the cost to retail ratio should be based on what amount of goods available for sale at (1) cost and (2) retail? 19. Crane Sales Company uses the retail inventory method to value its merchandise inventory. The following information is available for the current year: Cost Beginning inventory Purchases Freight-in 20. Net markups Net markdowns Employee discounts Sales - 2,500 145,000 Beginning inventory Purchases Freight-in 224,000 6,000 Net markups Net markdowns Sales 205,000 If the ending inventory is to be valued at the lower-of- cost-or-net realizable value, what is the cost to retail ratio? Use the following information for questions 20 through 22. The following data concerning the retail inventory method are taken from the financial records of Welch Company. Cost Retail - Retail - P 30,000 P 50,000 200,000 8,500 10,000 20,000 1,000 P 49,000 P 70,000 320,000 14,000 336,000 What is the ending inventory at retail should be? 21 If the ending inventory is to be valued at approximately the lower of cost or market, the calculation of the cost to retail ratio should be based on what amount of goods available for sale at (1) cost and (2) retail? 25. The following information is for the Bayway Manufacturing Company for November. Beginning Ending Inventories Raw Material P17,400 P13,200 Work in Process 31,150 28,975 Finished Goods 19,200 25,500 Direct Labor (21,000 DLH @ P13) Raw Material Purchases P120,000 Insurance-Office Indirect Labor Factory Supplies Used Other Expenses: Depr.-Factory Equipment 11,200 Office Supplies Expense 350 Insurance-Factory Depr. Office Equipment 17,300 Repair/Maintenance- Factory 1. Prepare in good form a Statement of Cost of Goods Sold. 2. Compute the total Inventory 2,570 900 Problems that can make us GREAT!!!!! Problem 1 Hayahay Company provided the following information from its accounting records for the year ended, December 31, 2017: physical count on this date 980,000 1,770 3,500 7,400 Inventory at December 31, 2017 per P 2017 Accounts Payable at December 31, 586,000 return) Net Sales (Sales Return less sales 10,048,000 Additional Information follows: a. Good held on consignment amounting to P 9,000, were included in the physical count of goods and in Accounts Payable. b. Retailers were holding P 50,000, at cost, goods on consignment from Hayahay, at their stores at year end. c. Included in the physical count were goods billed to a customer FOB shipping point on December 31, 2017. These goods had a cost of P 31,000 and were billed at P 40,000. The shipment was on Hayahay's loading dock waiting to be picked up by the common carrier. d. P 15,000 worth of goods were sold in the last week of 2017 and appropriately recorded as sales of P 21,000. The goods were included in the physical count on December 31, 2017, because the goods were on the loading dock awaiting to be picked up by the customer. e. Goods were in transit from a vendor on December 31, 2017, The invoice cost was P 71,000 and were shipped FOB Shipping Point on December 29, 2017. f. Work in process inventory costing P 30,000 was sent to an outside processor for plating on December 30, 2017. g. Goods returned from a customer and held pending inspection in the returned goods area on December 31, 2017, were not included in the physical count. On January 8, 2018, the tools costing P 32,000 were inspected and returned to inventory and credit memo amounting to P 47,000 were issued to customer on the same date. h. Goods shipped to a customer FOB destination on December 26, 2017, were in transit at December 31, 2017, and had a cost of P 21,000. Upon notification of receipt by the customer on January 2, 2018, Hayahay issued an invoice for P 42,000. i. Goods with an invoice Oct of P 27,000 were recorded in the receiving report dated January 2, 2018. The goods were not included in the physical count, but it was included in the Accounts Payable at December 31, 2017. j. Goods received from a vendor on December 26, 2017, were included in the physical count. However, the related P 56,000 vendor invoice was not included in the accounts payable at December 31, 2017, because the accounts payable copy of the receiving report was lost. k. On January 3, 2018, a monthly freight bill in the amount of P 6,000 was received. The bill specifically related to merchandise purchased in December 31, 2017, one half of which is still in the inventory at year end. This bill was not yet recorded in either inventory and accounts payable. Based on the above information, answer the following: 1. The adjusted inventory as of December 31, 2017 is a. P 1,158,000 1,190,000 a. P 710,000 719,000 2. The adjusted accounts payable as of December 31, 2017 is a. 9,000 b. P 1,119,000 24,000 d. P 1,160,000 a. P 151,000 234,000 b.P 639,000 d. P 633,000 3. The adjusted net sales as of December 31, 2017 is a. P 10,008,000 9,919,000 4. The total amount that was deducted from the unadjusted inventory based on the above audit findings is b. P 10,001,000 d. P 9,961,000 b. P 15,000 d. P 54,000 b. P 183,000 c. P c. P c. P d. P 204,000 5. The total amount that was added to the unadjusted inventory based on the above audit findings is c. P c. P Problem 2 You were engaged by Snooky Corp. whose main warehouse is in Lipa City, for the audit of its financial statements ending December 31, 2017. The company is in the wholesale business and makes a mark-up of 20% based on sales in all their sales. The following are the unadjusted balances of their accounts related to its inventory in its trial balance. Accounts Receivable P 520,000 PURCHASES DATE REFERENCE Balance Forwarded 12.28 RR No. 1114 12.30 RR No. 1116 12.31 RR No. 1117 12.31 RR NO. 1118 12.31 Closing Entry Inventory Accounts Payable SALES AMOUNT DATE REFERENCE AMOUNT 1,400,000 Balance Forwarded 2.600.000 12.000 12.27 SI No. 1020 35,000 12.28 SI No. 1021 21,000 12 28 SI No. 1022 32.000 12.31 SI No. 1023 (1,500,000 12.31 SI No. 1024 12.31 SI No. 1025 12.31 SI No: 1026 12.31 Closing Entry 20.000 75.000 5,000 50,000 40,000 34,000 8.000 2.832.000 630,000 410,000 You observed the physical inventory of goods in the warehouse on December 31, 2017, and were satisfied that it was properly taken. When performing sales and purchases cut-off test, you found that at December 31, the last Receiving Report (RR) that had been used (for goods physically received as of December 31) was No. 1117 and that no shipment has been made on Sales Invoice (SI) beyond no. 1024. You also obtained the following additional information: a. Not included in the warehouse physical inventory at December 31 were goods which had been purchased and received on RR No.1115 but were physically segregated awaiting the receipt of the invoice, which was not received until the following year. Cost was P 20,000. b. On the evening of December 31, there were two trucks in the company's warehouse. Goods inside the trucks were not included in the physical count as of December 31: 1. Truck No. APC 321 was unloaded on January 2 of the following year and received on RR. No. 1117. The goods were shipped FOB Destination. 2. Truck No. ULI 341 was loaded and sealed on December 31 but left the company premises only on January 2. This order was sold per Sales Invoice No. 1024. The goods were shipped FOB Shipping Point. c. Sales Invoice no. 1021 pertains to a shipment which was temporarily stranded at December 31 enroute to a client's customer. The client's customer received the goods which were shipped FOB Lipa. d. Enroute to the client on December 31 was a truckload of goods from supplier in Batangas were received on RR No. 1119. The goods were shipped FOB Batangas, and freight of P 2,000 was prepaid by the said supplier. Invocie price excluding freight amounted to P 54,000. 1. The correct amount of sales for the year ended, December 31, 2017 is a. P 2,750,000 P 2,675,000 b. P 2,742,000 d. P 2,667,000 a. P 1,488,000 P 1,522,000 2. The correct amount of purchases for the year ended, December 31, 2017 is C. b. P 1,542,000 d. P 1,574,000 C. 3. The correct inventory balance as of December 31, 2017 is a. P 737,000 757,000 a. P 446,000 363,000 b. P 739,000 d. P 759,000 4. The correct Accounts Receivable balance as of December 31, 2017 is a. P 454,000 452,000 b. P 478,000 d. P 438,000 c. P 5. The correct Accounts Payable balance as of December 31, 2017 is b. P 434,000 d. P 432,000 c. P c. P

Expert Answer:

Answer rating: 100% (QA)

10 To estimate the cost of inventory at March 31 we need to calculate the net purchases and deduct any purchase returns Net Purchases Purchases Purchase Returns Net Purchases P172000 P8000 P164000 Cos... View the full answer

Related Book For

Accounting

ISBN: 978-0324401844

22nd Edition

Authors: Carl S. Warren, James M. Reeve, Jonathan E. Duchac

Posted Date:

Students also viewed these accounting questions

-

The Hughes Supply Company uses an inventory management method to determine the monthly demands for various products. The demand values for the last 12 months of each product have been recorded and...

-

If an SEC-registered company uses the gross profit method to determine cost of goods sold for interim periods, would it be acceptable for the company to state that its not practicable to determine...

-

The Rider Company uses the gross profit method to estimate ending inventory and cost of goods sold. The cost percentage is determined based on historical data. What factors could cause the estimate...

-

A 0.500-kg block, attached to a spring with length 0.60 m and force constant 40.0 N/m, is at rest with the back of the block at point A on a frictionless, horizontal air table (Fig. 7.44). The mass...

-

Assume that the annual precipitation in a student's hometown is normally distributed, with expected value x = 36.3 inches and variance 2X = 8.41. A rare species of frog lives in the town. This rare...

-

7 years ago Alfa Bank invested $1,000,000 at a 5 percent annual interest rate. If the bank invests an additional $20,000 a year for 15 years, at the beginning of each year, at a 5 percent annual...

-

In a random sample of 400 industrial accidents, it was found that 231 were due at least partially to unsafe working conditions. Construct a \(99 \%\) confidence interval for the corresponding true...

-

The optical disk project team has started gathering the information necessary to develop the project networkpredecessor activities and activity times in weeks. The results of their meeting are found...

-

In the absence of air resistance, a projectile that lands at the elevation from which it was launched achieves maximum range when launched at a 45 angle. Suppose a projectile of mass m is launched...

-

Mr. Juan Dela Cruz is a self-employed professional based in the Philippines. He provides consulting services in the field of information technology. As a resident Filipino citizen, Mr. Dela Cruz is...

-

The lottery; 30 annual payments over 29 years Prize of: $372,011,000 If interest rate is 8.1% how large is used to determine a lump sum prize how large is the cash value option for the winners?

-

Provide your opinion as to how information technology can be very helpful to, but also can detract from, operational performance and efficiency. propose at least two examples of efforts that should...

-

1. What are some of the messages you received during your childhood about being/becoming a boy/man or a girl/woman in a Mexican household? 2. What were some of the positive aspects of getting those...

-

The circuit shown in Figure 1 is a 4-input inverting adder circuit, which is similar to the example that we covered in lecture. Answer the following questions: a) Using the "Golden Rules" and KCL,...

-

According to the Privacy Act 1988 and the Information Privacy Principles (IPPs), a person is entitled to have personal information protected. Explain how the legislation and IPPs apply to the...

-

1. What can charisma do for you? 2. What are the characteristics of charisma? 3. What are the clues of power? 4. What inhibits power? 5. How do you dismantle the 'imposter' syndrome? 6. Why are the...

-

2. A SUN has a par value of IDR. 450,000,000 with a 10% pa coupon and pays interest every May 1 and November 1. If on September 17 2021 the bond is offered at 98, how much must the buyer pay?

-

Whats the difference between an ordinary annuity and an annuity due? What type of annuity is shown below? How would you change the time line to show the other type of annuity?

-

The supplies account had a beginning balance of $1,245 and was debited for $2,860 for supplies purchased during the year. Journalize the adjusting entry required at the end of the year assuming the...

-

During November, Taylor Company incurred factory overhead costs as follows: indirect materials, $6,500; indirect labor, $8,000; utilities cost, $3,500; and depreciation, $2,800. Journalize the entry...

-

Iberian Carpet has the following unadjusted trial balance as of March 31, 2008. The debit and credit totals are not equal as a result of the following errors: a. The balance of cash was understated...

-

Which of the three types of government policiesantitrust, social regulation, and economic regulationis the basis for each of the following? a. Beautician education standards b. Certified Public...

-

Some airline executives have called for reregulation. Why might an executive of an airline prefer to operate in a regulated environment?

-

Suppose the Herfindahl index for domestic production of televisions is 5,000. Does this imply a very competitive or a noncompetitive environment?

Study smarter with the SolutionInn App