Interpreting Non-GAAP Disclosures The Boeing Company reported the following information in its MD&A section of a...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

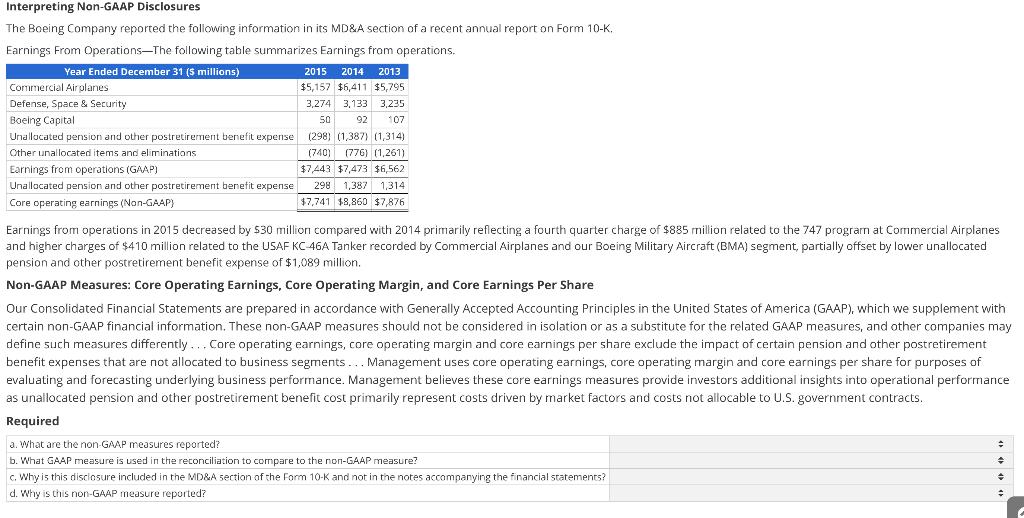

Interpreting Non-GAAP Disclosures The Boeing Company reported the following information in its MD&A section of a recent annual report on Form 10-K. Earnings From Operations-The following table summarizes Earnings from operations. Year Ended December 31 ($ millions) Commercial Airplanes Defense, Space & Security Boeing Capital Unallocated pension and other postretirement benefit expense Other unallocated items and eliminations. Earnings from operations (GAAP) Unallocated pension and other postretirement benefit expense Core operating earnings (Non-GAAP) 2015 2014 2013 $5,157 $6,411 $5,795 3,274 3,133 3,235 50 92 107 (298) (1,387) (1,314) (740) (776) (1,261) $7,443 $7,473 $6,562 298 1,387 1,314 $7,741 $8,860 $7,876 Earnings from operations in 2015 decreased by $30 million compared with 2014 primarily reflecting a fourth quarter charge of $885 million related to the 747 program at Commercial Airplanes. and higher charges of $410 million related to the USAF KC-46A Tanker recorded by Commercial Airplanes and our Boeing Military Aircraft (BMA) segment, partially offset by lower unallocated pension and other postretirement benefit expense of $1,089 million. Non-GAAP Measures: Core Operating Earnings, Core Operating Margin, and Core Earnings Per Share Our Consolidated Financial Statements are prepared in accordance with Generally Accepted Accounting Principles in the United States of America (GAAP), which we supplement with certain non-GAAP financial information. These non-GAAP measures should not be considered in isolation or as a substitute for the related GAAP measures, and other companies may define such measures differently... Core operating earnings, core operating margin and core earnings per share exclude the impact of certain pension and other postretirement benefit expenses that are not allocated to business segments... Management uses core operating earnings, core operating margin and core earnings per share for purposes of evaluating and forecasting underlying business performance. Management believes these core earnings measures provide investors additional insights into operational performance as unallocated pension and other postretirement benefit cost primarily represent costs driven by market factors and costs not allocable to U.S. government contracts. Required a. What are the non-GAAP measures reported? b. What GAAP measure is used in the reconciliation to compare to the non-GAAP measure? c. Why is this disclosure included in the MD&A section of the Form 10-K and not in the notes accompanying the financial statements? d. Why is this non-GAAP measure reported? = + ÷ Non-GAAP Measures: Core Operating Earnings, Core Operating Margin, and Core Earnings Per Share Our Consolidated Financial Statements are prepared in accordance with Generally Accepted Accounting Principles in the United States of America (GAAP), which we supplement with certain non-GAAP financial information. These non-GAAP measures should not be considered in isolation or as a substitute for the related GAAP measures, and other companies may define such measures differently... Core operating earnings, core operating margin and core earnings per share exclude the impact of certain pension and other postretirement benefit expenses that are not allocated to business segments... Management uses core operating ea evaluating and forecasting underlying business performance. Management believes these core earnin as unallocated pension and other postretirement benefit cost primarily represent costs driven by mar Required a. What are the non-GAAP measures reported? b. What GAAP measure is used in the reconciliation to compare to the non-GAAP measure? c. Why is this disclosure included in the MD&A section of the Form 10-K and not in the notes accompanying the financial stat d. Why is this non-GAAP measure reported? Net assets Net income Non-GAAP measures are a required component of the MD&A section Non-GAAP measures may be explained in the notes to financial statements Non-GAAP measures must be explained in the notes to financial statements The reporting affirms the computation of a measure widely and consistently used across companies The reporting of non-GAAP measures is a required industry practice Total assets Core operating earnings, core operating margin, core earnings per share Disclosure is not based on a GAAP standard Earnings from operations Voluntary decision made by management Interpreting Non-GAAP Disclosures The Boeing Company reported the following information in its MD&A section of a recent annual report on Form 10-K. Earnings From Operations-The following table summarizes Earnings from operations. Year Ended December 31 ($ millions) Commercial Airplanes Defense, Space & Security Boeing Capital Unallocated pension and other postretirement benefit expense Other unallocated items and eliminations. Earnings from operations (GAAP) Unallocated pension and other postretirement benefit expense Core operating earnings (Non-GAAP) 2015 2014 2013 $5,157 $6,411 $5,795 3,274 3,133 3,235 50 92 107 (298) (1,387) (1,314) (740) (776) (1,261) $7,443 $7,473 $6,562 298 1,387 1,314 $7,741 $8,860 $7,876 Earnings from operations in 2015 decreased by $30 million compared with 2014 primarily reflecting a fourth quarter charge of $885 million related to the 747 program at Commercial Airplanes. and higher charges of $410 million related to the USAF KC-46A Tanker recorded by Commercial Airplanes and our Boeing Military Aircraft (BMA) segment, partially offset by lower unallocated pension and other postretirement benefit expense of $1,089 million. Non-GAAP Measures: Core Operating Earnings, Core Operating Margin, and Core Earnings Per Share Our Consolidated Financial Statements are prepared in accordance with Generally Accepted Accounting Principles in the United States of America (GAAP), which we supplement with certain non-GAAP financial information. These non-GAAP measures should not be considered in isolation or as a substitute for the related GAAP measures, and other companies may define such measures differently... Core operating earnings, core operating margin and core earnings per share exclude the impact of certain pension and other postretirement benefit expenses that are not allocated to business segments... Management uses core operating earnings, core operating margin and core earnings per share for purposes of evaluating and forecasting underlying business performance. Management believes these core earnings measures provide investors additional insights into operational performance as unallocated pension and other postretirement benefit cost primarily represent costs driven by market factors and costs not allocable to U.S. government contracts. Required a. What are the non-GAAP measures reported? b. What GAAP measure is used in the reconciliation to compare to the non-GAAP measure? c. Why is this disclosure included in the MD&A section of the Form 10-K and not in the notes accompanying the financial statements? d. Why is this non-GAAP measure reported? = + ÷ Non-GAAP Measures: Core Operating Earnings, Core Operating Margin, and Core Earnings Per Share Our Consolidated Financial Statements are prepared in accordance with Generally Accepted Accounting Principles in the United States of America (GAAP), which we supplement with certain non-GAAP financial information. These non-GAAP measures should not be considered in isolation or as a substitute for the related GAAP measures, and other companies may define such measures differently... Core operating earnings, core operating margin and core earnings per share exclude the impact of certain pension and other postretirement benefit expenses that are not allocated to business segments... Management uses core operating ea evaluating and forecasting underlying business performance. Management believes these core earnin as unallocated pension and other postretirement benefit cost primarily represent costs driven by mar Required a. What are the non-GAAP measures reported? b. What GAAP measure is used in the reconciliation to compare to the non-GAAP measure? c. Why is this disclosure included in the MD&A section of the Form 10-K and not in the notes accompanying the financial stat d. Why is this non-GAAP measure reported? Net assets Net income Non-GAAP measures are a required component of the MD&A section Non-GAAP measures may be explained in the notes to financial statements Non-GAAP measures must be explained in the notes to financial statements The reporting affirms the computation of a measure widely and consistently used across companies The reporting of non-GAAP measures is a required industry practice Total assets Core operating earnings, core operating margin, core earnings per share Disclosure is not based on a GAAP standard Earnings from operations Voluntary decision made by management

Expert Answer:

Answer rating: 100% (QA)

a The nonGAAP measures reported are core operating earnings core operating margin and core earnings ... View the full answer

Related Book For

Corporate Financial Accounting

ISBN: 978-1133952411

12th edition

Authors: Carl S. Warren, James M. Reeve, Jonathan E. Duchac

Posted Date:

Students also viewed these accounting questions

-

Earnings per Share Disclosure Extreme Company reported the following information about its stock on its December 31, 2016, balance sheet: Preferred stock, $2 par value, 5% cumulative, 300,000 shares...

-

The Abercrombie Supply Company reported the following information for 2014. Prepare a common-size income statement for the year ended June 30, 2014. Abercrombie Supply Company Income Statement for...

-

Hometown Supply Company reported the following information in its comparative financial statements for the fiscal year ended January 31, 2018: Requirements 1. Compute the net profit margin ratio for...

-

Solve the equation symbolically. Then solve the related inequality. 1 - X

-

Repeat Exercise 11 using the Jacobi method. In Exercise 11 a. Is the coefficient matrix Strictly diagonally dominant? b. Compute the spectral radius of the Gauss-Seidel matrix T g . c. Use the...

-

Getting more Americans to realize that it pays to make things in the United States is the heart of the competitiveness issue. (This is a quote from an American business magazine.) a. Would Americans...

-

Consider the solar or waste-heat refrigeration cycle in Figure 10.41, which was proposed by Sommerfeld (2001). In addition to the conventional refrigeration loop, a portion of the condensate is...

-

Applin Corporation has a desired rate of return of 8 percent. Troy Anderson is in charge of one of Applins three investment centers. His center controlled operating assets of $5,000,000 that were...

-

Finer, % 100 90 80 70 60 50 40 30 20 10 0 0.01 0.1 1 Size, mm L 10 100 Figure shows a grain size distribution curve of soil. Estimate the coefficient of curvature (Cc) of this soil.

-

Tele Telcom, Inc. is a medium-sized company that produces automotive parts. The company has been in business for over 50 years and has a workforce of approximately 500 employees. Recently, some...

-

Using the Reader-Response model we learned in class, use Martin Ginsberg's essay, "Thirty-Eight Who Saw Murder and Didn't Call the Police," as the basis for your response discussing whether or not...

-

Two years later, the Baconia central bank hires you as an economic consultant and has provided you with these statistics on the current economic conditions: Real GDP = $11.1 trillion Inflation rate =...

-

Mrs. Safar, a devout Muslim, was employed as a teaching assistant in a junior school controlled by the local education board. She refused to comply with her headmaster's instruction that she should...

-

Skylar Ross, March 2021 The recent growth of the e-commerce industry has transformed the global marketplace. According to Digital Commerce 360, consumers spent $861.02 billion on online shopping in...

-

Why did the Cold War end suddenly and with little warning in the late 1980s and early 1990s? What was the consequences of the end of this event for the U.S.?

-

-B1/B3*(1-B4))+B2 -B1/(B3 (1-B4))+B2 -85+84 B6 A 1 Next Dividend (D) 2 Dividend Growth Rate 3 Stock Price -B1/B3+B2 4 Flotation Cost 5 Beta 6 Risk-free Rate 7 Expected Market Return 8 Cost of New...

-

Which of the 3 categories of earnings quality definitions do you find most convincing for clarifying what is meant by "earnings quality"?

-

Write a while loop that uses an explicit iterator to accomplish the same thing as Exercise 7.3. Exercise 7.3. Write a for-each loop that calls the addInterest method on each BankAccount object in a...

-

Assume the same facts as in Exercise 9-25, except that the book value of the press traded in is $108,500. (a) What is the amount of cash given? (b) What is the gain or loss on the exchange? In...

-

The unadjusted trial balance of La Mesa Laundry at August 31, 2014, the end of the current fiscal year, is shown below. The data needed to determine year-end adjustments are as follows: a. Wages...

-

The supplies account had a beginning balance of $1,975 and was debited for $4,125 for supplies purchased during the year. Journalize the adjusting entry required at the end of the year assuming the...

-

The following information relates to the operations of Emile Luxury Ltd. The profit was $2 750 000. The company distributed preference dividends of $50 000, and ordinary dividends of $300 000. Over...

-

Pedros Parts Ltds statement of financial position (extract only) on 30 June 2023 is set out below. Required (a) Calculate the current and quick ratios. (b) A loan agreement entered into by the...

-

You are provided with the following information from the statement of cash flows for Precedent Ltd. Required (a) Calculate the following cash sufficiency ratios for Precedent Ltd for 2025 and 2024:...

Study smarter with the SolutionInn App