You are following Option 1 on pages 10 and 11 of the Instructions, Flowcharts, and Ledgers...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

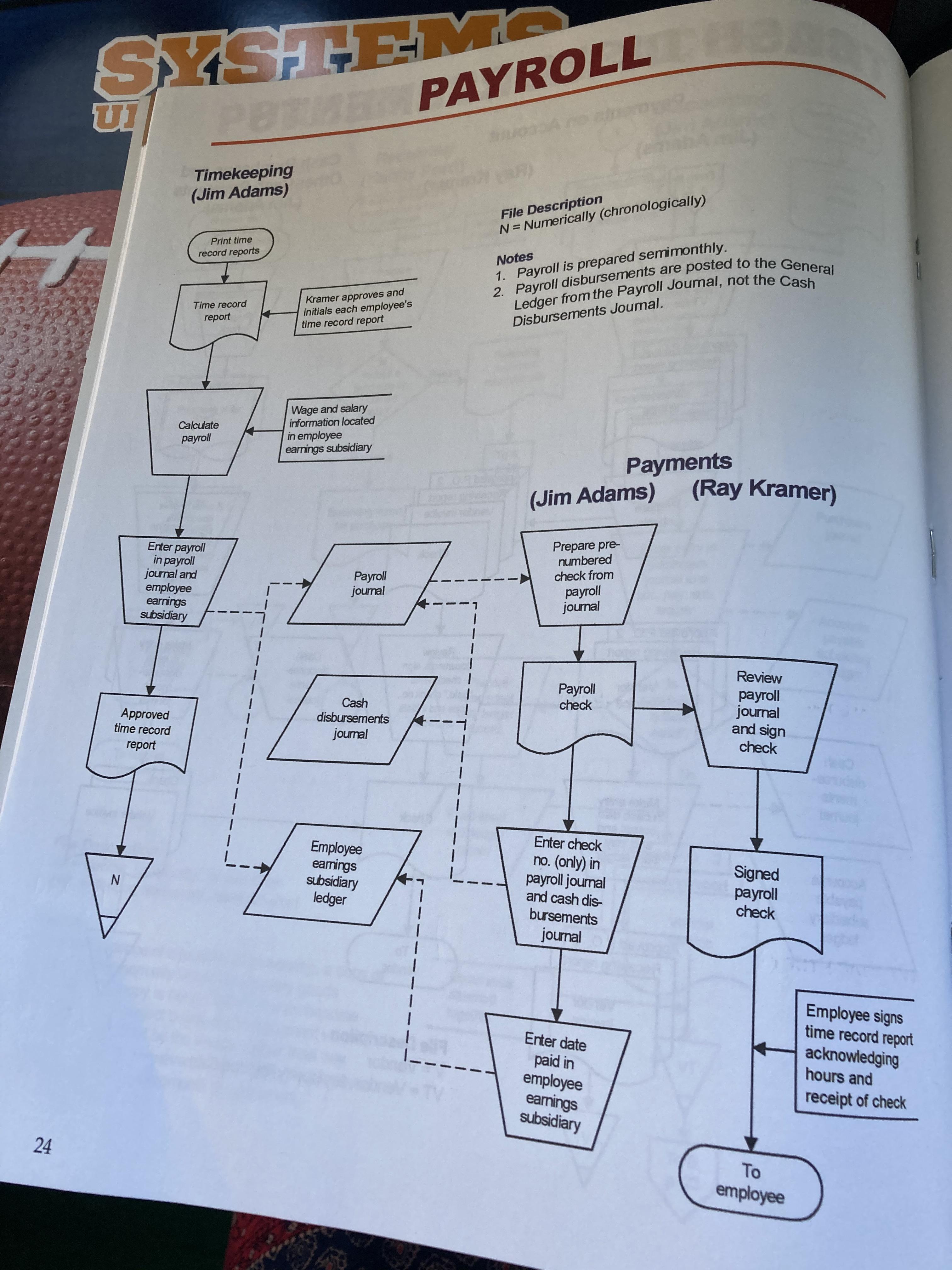

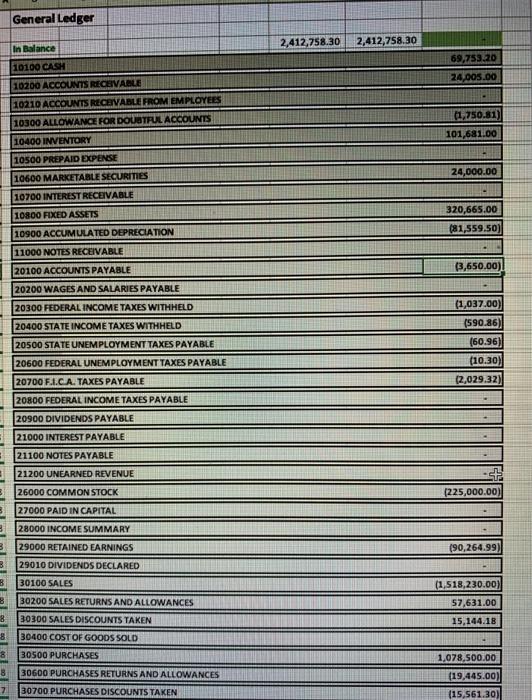

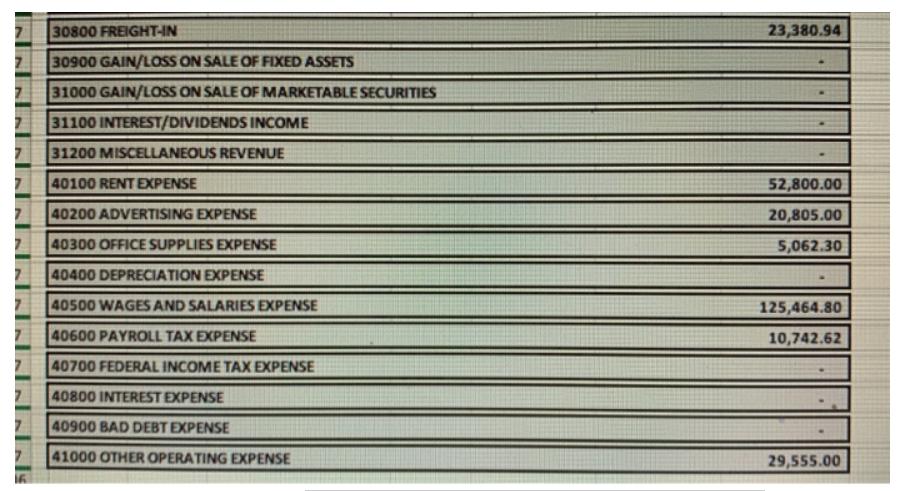

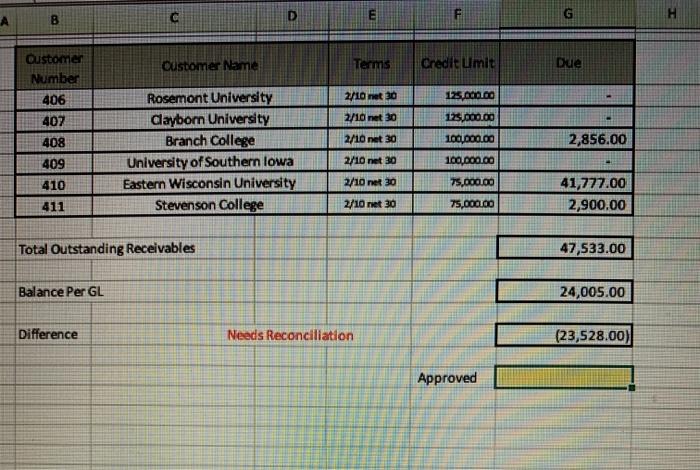

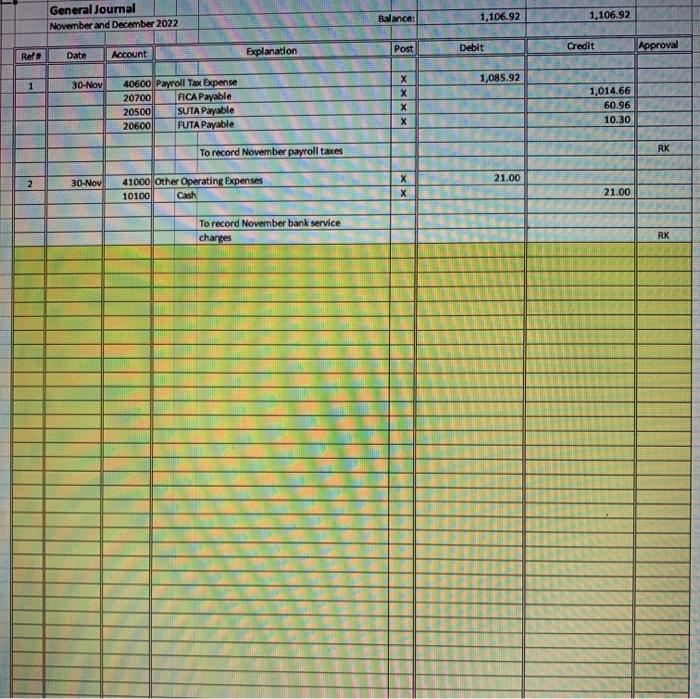

You are following Option 1 on pages 10 and 11 of the Instructions, Flowcharts, and Ledgers book. Read Introductory information, pages 3-12, 16 and scan 25-43. Scan through all documents in the Documents Folder. Please use the blue version of the transaction list. Destroy the other versions (green). Carefully read Option 1, pages 10. Go through all transactions on the transactions list (Document No. 1) and write S & CR, P & CD, or PR beside each transaction as follows: $ Sale, sales return, cash receipt, or charge-off (S & CR) $ Purchase of goods or services or cash disbursement, except for payroll (P & CD) $ Payroll (PR) Every transaction must be identified as one of these three types. Sales and Cash Receipts Study flowcharts on pages 18-21. Complete the seven-step process for recording a transaction on pages 11 and 12 for all sales and cash receipts transactions on the transactions list. USE THE SUA 10TH Edition Hybrid Spreadsheet for recording all transactions in journals, general ledger and subsidiary ledgers. Complete WAREN'S MONTH-END PROCEDURES 2, 3A, 3B, 5, 6, and 7 on pages 12 and 13 for sales and cash receipts only. Complete WAREN'S YEAR-END PROCEDURE 6 on page 15 (accounts receivable aged trial balance only.) S 24 SYSTEME POTHER PAYROLL UI Approved time record report N Timekeeping (Jim Adams) Print time record reports Time record report Calculate payroll Enter payroll in payroll journal and employee earnings subsidiary 1 Kramer approves and initials each employee's time record report Wage and salary information located in employee earnings subsidiary Payroll journal Cash disbursements journal Employee earnings subsidiary ledger 12- File Description N = Numerically (chronologically) Notes 1. Payroll is prepared semimonthly. 2. Payroll disbursements are posted to the General Ledger from the Payroll Journal, not the Cash Disbursements Journal. apr obol (Jim Adams) Prepare pre- numbered check from payroll journal Payroll check Enter check no. (only) in payroll journal and cash dis- bursements journal Payments Enter date paid in employee earnings subsidiary (Ray Kramer) Review payroll journal and sign check Signed payroll check To employee Employee signs time record report acknowledging hours and receipt of check I 12 OBC 2 UNDERST vi. File documents in the appropriate file tab in the envelope in accordance the flowchart description. See pages 5 and 6 of this book for additional filing vii. Proceed to the next transaction. Repeat this process until you have completed and year-end procedures. REQUIREMENTS the roles of Ray Kramer, Nancy Ford, and Jim Adams and perform each of these month- after all transactions are recorded in the journals and subsidiary ledgers. You are to assume Following are the procedures performed at the end of each month by Waren's employees statement (Doc. No. 23), and the list of items clearing with the bank statement (Doc. No. 24). Set all end procedures for December. The only materials needed are this list of seven month-end monthly statement (Doc. No. 15), bank reconciliation for November (Doc. No. 22), December bank procedures, all journals and ledgers, and four items from the loose document set: blank other documents and records temporarily aside. WAREN'S MONTH-END PROCEDURES 1. Jim Adams foots and crossfoots each of the five special journals (sales, cash receipts, the special journals to indicate that his work has been performed: F for Footing and purchases, cash disbursements, and payroll). He uses the following symbols in C for Cross-footing. 2. Jim Adams posts the column totals and individual transactions in "Other" columns to and by each of the individual transactions in the "Other" columns to show that the He places a posting reference check mark [✔] under each column total in the journals the appropriate general ledger account and updates each general ledger account balance. numbers have been posted. 3. After receiving the bank statement (Doc. No. 23) and list of items clearing with the bank statement (Doc. No. 24) from the bank, he performs the following procedures: a. Traces and agrees the monthly totals from the cash account columns of the cash receipts and cash disbursements journals to the posting in the general ledger cash account. He initials the cash account column totals in the journals, as well as the general ledger lines where the totals are posted. b. Compares each entry in the cash receipts prelist (Doc. No. 9) to the cash receipts journal for name, date, and amount, and puts a check mark [✔] by each entry in the prelist. c. Prepares a bank reconciliation using the procedures outlined in the Systems Understanding Aid Reference book on pages 62 through 65. You can also use November's bank reconciliation (Doc. No. 22) as a model. Deposits in transit and outstanding checks at November 30 are listed there. dance with onal filing mpleted th-end yees me th- nd k k 3 O 好 d. Adjusts the cash general ledger account using the general journal, regardless of materiality, for all reconciling items requiring an adjustment. Attaches together and files the bank reconciliation, bank statement, list of items clearing with bank statement, and the cash receipts prelist in the file labeled "Shipping/Banking." e. 4. Jim Adams calculates and records the unemployment taxes paid by employers, and Waren's portion of the FICA payroll tax. These payroll taxes are calculated at the end of the month on gross payroll and recorded in the general journal. The taxes are paid the following month. REQUIREMENTS State and federal unemployment taxes are imposed on the first $7,000 of wages paid to covered employees in 2017. Thus, a review of the employee earnings subsidiary ledger on pages 40 and 41 of this book indicates that only one of Waren's employees remains subject to this tax (i.e., has not yet exceeded the wage base maximum). The same wage base maximum is used in the project for both state and federal unemployment taxes to simplify the calculations. The state unemployment tax (SUTA) rate is 3.55%. Because employers are allowed credits against the federal unemployment tax (FUTA) rate for participation in state unemployment programs, the net FUTA rate is .6%. 5. Jim Adams posts transactions from the general journal to the general ledger (and subsidiary if applicable), places a posting reference check mark [✔] in the general journal post reference column for each item posted, and updates each general ledger balance. 6. Nancy Ford foots the balances of each subsidiary for the accounts receivable, accounts payable, employee earnings, and fixed assets subsidiaries, and compares the total to the appropriate general ledger control account (G/L accounts 10200, 20100, 40500, 10800, and 10900, respectively). She initials each general ledger control account to indicate that she has made the comparison. 7. Jim Adams prepares a monthly statement (Doc. No. 15) for each customer with a balance. He includes information about each unpaid invoice including its aging status. Aging totals and the total amount due are shown at the bottom. He completes the remittance advice (attached to the monthly statement) in a similar fashion except that no aging is included. Ray Kramer reviews each statement and initials it before it is mailed to the customer. In this project, you are to prepare a December monthly statement for only one customer and file it in the "Mailed to Outsiders" file tab. The name of the selected customer is stated in the transactions list (Doc. No. 1) provided with your loose document set in this package. After completing all seven month-end procedures for December, continue to the next section and perform Waren's year-end procedures. 30 D DO $0 13 B 3 3 B 8 8 8 8 7 General Ledger In Balance 10100 CASH 10200 ACCOUNTS RECEIVABLE 10210 ACCOUNTS RECEIVABLE FROM EMPLOYEES 10300 ALLOWANCE FOR DOUBTFUL ACCOUNTS 10400 INVENTORY 10500 PREPAID EXPENSE 10600 MARKETABLE SECURITIES 10700 INTEREST RECEIVABLE 10800 FIXED ASSETS 10900 ACCUMULATED DEPRECIATION 11000 NOTES RECEIVABLE 20100 ACCOUNTS PAYABLE 20200 WAGES AND SALARIES PAYABLE 20300 FEDERAL INCOME TAXES WITHHELD 20400 STATE INCOME TAXES WITHHELD 20500 STATE UNEMPLOYMENT TAXES PAYABLE 20600 FEDERAL UNEMPLOYMENT TAXES PAYABLE 20700 F.I.C.A. TAXES PAYABLE 20800 FEDERAL INCOME TAXES PAYABLE 20900 DIVIDENDS PAYABLE 21000 INTEREST PAYABLE 21100 NOTES PAYABLE 21200 UNEARNED REVENUE 26000 COMMON STOCK 27000 PAID IN CAPITAL 28000 INCOME SUMMARY 29000 RETAINED EARNINGS 29010 DIVIDENDS DECLARED 30100 SALES 30200 SALES RETURNS AND ALLOWANCES 30300 SALES DISCOUNTS TAKEN 30400 COST OF GOODS SOLD 30500 PURCHASES 30600 PURCHASES RETURNS AND ALLOWANCES 30700 PURCHASES DISCOUNTS TAKEN 2,412,758.30 2,412,758.30 69,753.20 24,005.00 (1,750.81) 101,681.00 24,000.00 320,665.00 (81,559.50) (3,650.00) (1,037.00) (590.86) (60.96) (10.30) (2,029.32) (225,000.00) (90,264.99) (1,518,230.00) 57,631.00 15,144.18 1,078,500.00 (19,445.00) (15,561.30) 7 30800 FREIGHT-IN 7 30900 GAIN/LOSS ON SALE OF FIXED ASSETS 7 31000 GAIN/LOSS ON SALE OF MARKETABLE SECURITIES 7 31100 INTEREST/DIVIDENDS INCOME 7 31200 MISCELLANEOUS REVENUE 7 40100 RENT EXPENSE 7 40200 ADVERTISING EXPENSE 40300 OFFICE SUPPLIES EXPENSE 40400 DEPRECIATION EXPENSE 40500 WAGES AND SALARIES EXPENSE 40600 PAYROLL TAX EXPENSE 40700 FEDERAL INCOME TAX EXPENSE 40800 INTEREST EXPENSE 40900 BAD DEBT EXPENSE 41000 OTHER OPERATING EXPENSE 7 7 7 7 7 7 7 23,380.94 52,800.00 20,805.00 5,062.30 125,464.80 10,742.62 29,555.00 B Customer Number 406 407 408 409 410 411 Balance Per GL C Total Outstanding Receivables Difference D Customer Name Rosemont University Clayborn University Branch College University of Southern lowa Eastern Wisconsin University Stevenson College E Needs Reconciliation Terms 2/10 net 30 2/10 net 30 2/10 net 30 2/10 net 30 2/10 net 30 2/10 net 30 Credit Limit 125.000.00 125,000.00 100,000.00 100,000.00 75,000.00 75,000.00 Approved G Due 2,856.00 41,777.00 2,900.00 47,533.00 24,005.00 (23,528.00) Ref # 1 2 General Journal November and December 2022 Date 30-Nov 30-Nov Account 40600 Payroll Tax Expense 20700 FICA Payable 20500 SUTA Payable 20600 FUTA Payable Explanation To record November payroll taxes 41000 Other Operating Expenses Cash 10100 To record November bank service charges Balance: Post X xxx X X 1,106.92 Debit 1,085.92 21.00 1,106.92 Credit 1,014.66 60.96 10.30 21.00 Approval RK RK You are following Option 1 on pages 10 and 11 of the Instructions, Flowcharts, and Ledgers book. Read Introductory information, pages 3-12, 16 and scan 25-43. Scan through all documents in the Documents Folder. Please use the blue version of the transaction list. Destroy the other versions (green). Carefully read Option 1, pages 10. Go through all transactions on the transactions list (Document No. 1) and write S & CR, P & CD, or PR beside each transaction as follows: $ Sale, sales return, cash receipt, or charge-off (S & CR) $ Purchase of goods or services or cash disbursement, except for payroll (P & CD) $ Payroll (PR) Every transaction must be identified as one of these three types. Sales and Cash Receipts Study flowcharts on pages 18-21. Complete the seven-step process for recording a transaction on pages 11 and 12 for all sales and cash receipts transactions on the transactions list. USE THE SUA 10TH Edition Hybrid Spreadsheet for recording all transactions in journals, general ledger and subsidiary ledgers. Complete WAREN'S MONTH-END PROCEDURES 2, 3A, 3B, 5, 6, and 7 on pages 12 and 13 for sales and cash receipts only. Complete WAREN'S YEAR-END PROCEDURE 6 on page 15 (accounts receivable aged trial balance only.) S 24 SYSTEME POTHER PAYROLL UI Approved time record report N Timekeeping (Jim Adams) Print time record reports Time record report Calculate payroll Enter payroll in payroll journal and employee earnings subsidiary 1 Kramer approves and initials each employee's time record report Wage and salary information located in employee earnings subsidiary Payroll journal Cash disbursements journal Employee earnings subsidiary ledger 12- File Description N = Numerically (chronologically) Notes 1. Payroll is prepared semimonthly. 2. Payroll disbursements are posted to the General Ledger from the Payroll Journal, not the Cash Disbursements Journal. apr obol (Jim Adams) Prepare pre- numbered check from payroll journal Payroll check Enter check no. (only) in payroll journal and cash dis- bursements journal Payments Enter date paid in employee earnings subsidiary (Ray Kramer) Review payroll journal and sign check Signed payroll check To employee Employee signs time record report acknowledging hours and receipt of check I 12 OBC 2 UNDERST vi. File documents in the appropriate file tab in the envelope in accordance the flowchart description. See pages 5 and 6 of this book for additional filing vii. Proceed to the next transaction. Repeat this process until you have completed and year-end procedures. REQUIREMENTS the roles of Ray Kramer, Nancy Ford, and Jim Adams and perform each of these month- after all transactions are recorded in the journals and subsidiary ledgers. You are to assume Following are the procedures performed at the end of each month by Waren's employees statement (Doc. No. 23), and the list of items clearing with the bank statement (Doc. No. 24). Set all end procedures for December. The only materials needed are this list of seven month-end monthly statement (Doc. No. 15), bank reconciliation for November (Doc. No. 22), December bank procedures, all journals and ledgers, and four items from the loose document set: blank other documents and records temporarily aside. WAREN'S MONTH-END PROCEDURES 1. Jim Adams foots and crossfoots each of the five special journals (sales, cash receipts, the special journals to indicate that his work has been performed: F for Footing and purchases, cash disbursements, and payroll). He uses the following symbols in C for Cross-footing. 2. Jim Adams posts the column totals and individual transactions in "Other" columns to and by each of the individual transactions in the "Other" columns to show that the He places a posting reference check mark [✔] under each column total in the journals the appropriate general ledger account and updates each general ledger account balance. numbers have been posted. 3. After receiving the bank statement (Doc. No. 23) and list of items clearing with the bank statement (Doc. No. 24) from the bank, he performs the following procedures: a. Traces and agrees the monthly totals from the cash account columns of the cash receipts and cash disbursements journals to the posting in the general ledger cash account. He initials the cash account column totals in the journals, as well as the general ledger lines where the totals are posted. b. Compares each entry in the cash receipts prelist (Doc. No. 9) to the cash receipts journal for name, date, and amount, and puts a check mark [✔] by each entry in the prelist. c. Prepares a bank reconciliation using the procedures outlined in the Systems Understanding Aid Reference book on pages 62 through 65. You can also use November's bank reconciliation (Doc. No. 22) as a model. Deposits in transit and outstanding checks at November 30 are listed there. dance with onal filing mpleted th-end yees me th- nd k k 3 O 好 d. Adjusts the cash general ledger account using the general journal, regardless of materiality, for all reconciling items requiring an adjustment. Attaches together and files the bank reconciliation, bank statement, list of items clearing with bank statement, and the cash receipts prelist in the file labeled "Shipping/Banking." e. 4. Jim Adams calculates and records the unemployment taxes paid by employers, and Waren's portion of the FICA payroll tax. These payroll taxes are calculated at the end of the month on gross payroll and recorded in the general journal. The taxes are paid the following month. REQUIREMENTS State and federal unemployment taxes are imposed on the first $7,000 of wages paid to covered employees in 2017. Thus, a review of the employee earnings subsidiary ledger on pages 40 and 41 of this book indicates that only one of Waren's employees remains subject to this tax (i.e., has not yet exceeded the wage base maximum). The same wage base maximum is used in the project for both state and federal unemployment taxes to simplify the calculations. The state unemployment tax (SUTA) rate is 3.55%. Because employers are allowed credits against the federal unemployment tax (FUTA) rate for participation in state unemployment programs, the net FUTA rate is .6%. 5. Jim Adams posts transactions from the general journal to the general ledger (and subsidiary if applicable), places a posting reference check mark [✔] in the general journal post reference column for each item posted, and updates each general ledger balance. 6. Nancy Ford foots the balances of each subsidiary for the accounts receivable, accounts payable, employee earnings, and fixed assets subsidiaries, and compares the total to the appropriate general ledger control account (G/L accounts 10200, 20100, 40500, 10800, and 10900, respectively). She initials each general ledger control account to indicate that she has made the comparison. 7. Jim Adams prepares a monthly statement (Doc. No. 15) for each customer with a balance. He includes information about each unpaid invoice including its aging status. Aging totals and the total amount due are shown at the bottom. He completes the remittance advice (attached to the monthly statement) in a similar fashion except that no aging is included. Ray Kramer reviews each statement and initials it before it is mailed to the customer. In this project, you are to prepare a December monthly statement for only one customer and file it in the "Mailed to Outsiders" file tab. The name of the selected customer is stated in the transactions list (Doc. No. 1) provided with your loose document set in this package. After completing all seven month-end procedures for December, continue to the next section and perform Waren's year-end procedures. 30 D DO $0 13 B 3 3 B 8 8 8 8 7 General Ledger In Balance 10100 CASH 10200 ACCOUNTS RECEIVABLE 10210 ACCOUNTS RECEIVABLE FROM EMPLOYEES 10300 ALLOWANCE FOR DOUBTFUL ACCOUNTS 10400 INVENTORY 10500 PREPAID EXPENSE 10600 MARKETABLE SECURITIES 10700 INTEREST RECEIVABLE 10800 FIXED ASSETS 10900 ACCUMULATED DEPRECIATION 11000 NOTES RECEIVABLE 20100 ACCOUNTS PAYABLE 20200 WAGES AND SALARIES PAYABLE 20300 FEDERAL INCOME TAXES WITHHELD 20400 STATE INCOME TAXES WITHHELD 20500 STATE UNEMPLOYMENT TAXES PAYABLE 20600 FEDERAL UNEMPLOYMENT TAXES PAYABLE 20700 F.I.C.A. TAXES PAYABLE 20800 FEDERAL INCOME TAXES PAYABLE 20900 DIVIDENDS PAYABLE 21000 INTEREST PAYABLE 21100 NOTES PAYABLE 21200 UNEARNED REVENUE 26000 COMMON STOCK 27000 PAID IN CAPITAL 28000 INCOME SUMMARY 29000 RETAINED EARNINGS 29010 DIVIDENDS DECLARED 30100 SALES 30200 SALES RETURNS AND ALLOWANCES 30300 SALES DISCOUNTS TAKEN 30400 COST OF GOODS SOLD 30500 PURCHASES 30600 PURCHASES RETURNS AND ALLOWANCES 30700 PURCHASES DISCOUNTS TAKEN 2,412,758.30 2,412,758.30 69,753.20 24,005.00 (1,750.81) 101,681.00 24,000.00 320,665.00 (81,559.50) (3,650.00) (1,037.00) (590.86) (60.96) (10.30) (2,029.32) (225,000.00) (90,264.99) (1,518,230.00) 57,631.00 15,144.18 1,078,500.00 (19,445.00) (15,561.30) 7 30800 FREIGHT-IN 7 30900 GAIN/LOSS ON SALE OF FIXED ASSETS 7 31000 GAIN/LOSS ON SALE OF MARKETABLE SECURITIES 7 31100 INTEREST/DIVIDENDS INCOME 7 31200 MISCELLANEOUS REVENUE 7 40100 RENT EXPENSE 7 40200 ADVERTISING EXPENSE 40300 OFFICE SUPPLIES EXPENSE 40400 DEPRECIATION EXPENSE 40500 WAGES AND SALARIES EXPENSE 40600 PAYROLL TAX EXPENSE 40700 FEDERAL INCOME TAX EXPENSE 40800 INTEREST EXPENSE 40900 BAD DEBT EXPENSE 41000 OTHER OPERATING EXPENSE 7 7 7 7 7 7 7 23,380.94 52,800.00 20,805.00 5,062.30 125,464.80 10,742.62 29,555.00 B Customer Number 406 407 408 409 410 411 Balance Per GL C Total Outstanding Receivables Difference D Customer Name Rosemont University Clayborn University Branch College University of Southern lowa Eastern Wisconsin University Stevenson College E Needs Reconciliation Terms 2/10 net 30 2/10 net 30 2/10 net 30 2/10 net 30 2/10 net 30 2/10 net 30 Credit Limit 125.000.00 125,000.00 100,000.00 100,000.00 75,000.00 75,000.00 Approved G Due 2,856.00 41,777.00 2,900.00 47,533.00 24,005.00 (23,528.00) Ref # 1 2 General Journal November and December 2022 Date 30-Nov 30-Nov Account 40600 Payroll Tax Expense 20700 FICA Payable 20500 SUTA Payable 20600 FUTA Payable Explanation To record November payroll taxes 41000 Other Operating Expenses Cash 10100 To record November bank service charges Balance: Post X xxx X X 1,106.92 Debit 1,085.92 21.00 1,106.92 Credit 1,014.66 60.96 10.30 21.00 Approval RK RK

Expert Answer:

Answer rating: 100% (QA)

S CR 1115 Sold merchandise to Rosemont University for 125000 on account terms 210 net 30 S CR ... View the full answer

Related Book For

Posted Date:

Students also viewed these accounting questions

-

Cost of goods sold for Harlem Tool & Die during 20X1 was $400,000. Beginning inventory was $64,000 and ending inventory was $89,000. Beginning trade accounts payable were $13,000, and ending trade...

-

Cost of goods sold is shown as a distinct line item on the income statement. Where is information related to cost of goods sold shown on the statement of cash flows under both the direct and indirect...

-

In 2013, Macys reported cost of goods sold of $ 16.5 billion, ending inventory for 2013 of $ 5.3 billion, and ending inventory for the previous year (2012) of $ 5.1 billion. Required: If the cost of...

-

A random sample of 100 students was taken from a large university to study the relationship between GPA and the number of hours of study per week. The following linear regression equation was...

-

Mercury(I) chloride, Hg2Cl2, is an unusual salt in that it dissolves to form Hg22+ and 2Cl. Use the solubility product constant (Table 17.1) to calculate the following: (a) The molar solubility of...

-

Explain why, despite its being acceptable on the basis of NPV or of IRR, a real estate investment still might not be acceptable to a given investor.

-

The SI units of stress are: (a) \(\mathrm{kg} / \mathrm{mm}^{2}\) (b) \(\mathrm{N} / \mathrm{mm}\) (c) \(\mathrm{N} / \mathrm{mm}^{2}\) (d) N.mm

-

Seger, Inc., is an unlevered firm with expected annual earnings before taxes of $21 million in perpetuity. The current required return on the firms equity is 16 percent, and the firm distributes all...

-

In the "Stakeholder Analysis in Projects" article this week, the authors Jepsen and Eskerod (2008) found that the "guidelines provided in current literature are far too general to be useful for...

-

Stephen is a UK resident taxpayer with two different sources of income. He works part-time as an IT consultant for a small number of clients, on a project management basis. A separate contract is...

-

What can I comment on these paragraphs? 1. Newton's First Law of Motion is, "an object rest remains at rest, an an object in motion remains in motion at constant speed and in a straight line unless...

-

Find the optimum value for each objective function given in Problems 47-51. Maximize \(P=100 x+100 y\) subject to the constraints of Problem 37. Data from problem 37 \(\left\{\begin{array}{l}x \geq 0...

-

Given the matrices in Problems 36-39, perform elementary row operations to obtain zeros above and below the 1 in the third column without changing the entries in the first or second columns. [D] =...

-

The combined height of the Transamerica Tower and the Bank of America Building is 1,632 ft. The Transamerica Tower is \(74 \mathrm{ft}\) taller. What is the height of each of the San Francisco...

-

A chemist has two solutions of sulfuric acid. One is a \(50 \%\) solution, and the other is a \(75 \%\) solution. How many liters of each does the chemist mix to get 10 liters of a \(60 \%\) solution?

-

A collection of coins has a value of \(\$ 4.76\). There is the same number of nickels and dimes, but there are four fewer pennies than nickels or dimes. How many pennies are in the collection if...

-

What are the key characteristics of a monopoly market structure, and how does it differ from other market structures such as perfect competition? (20 Points) Using real-world examples, discuss the...

-

What is the back work ratio? What are typical back work ratio values for gas-turbine engines?

-

The purchasing department of Xena Co. creates $676,000 of overhead costs each year. The annual cost and quantity of activity involved in each primary task in the department follow Required: (a)...

-

Intercept, Inc. estimated that, for 2009, $761,250 of overhead costs would be incurred at 175,000 machine hours. During 2009, the company incurs 182,000 machine hours and has actual overhead costs of...

-

You and some friends are watching a football game on television and suddenly realize that youre really hungry. Required: Prepare a process map that extends from the point of the hungry determination...

-

The indicative of the stall flutter is the sign of the integral under the curve of (i) lift vs vertical displacement for plunging, (ii) moment vs angle of attack for pitching. Why? In obtaining the...

-

Using the potential theory obtain the damping for a cycle of (i) plunge, (ii) pitch oscillations.

-

Consider a delta wing with sweep angle \(\Lambda\). Show that the expressions 8.11 and 8.12 give the same lift line slope for the delta wing. Eq 8.11 Eq 8.12 = CD CD+CL tan

A History And Description Of Roman Political Institutions 1st Edition - ISBN: B009JU9OZ4 - Free Book

Study smarter with the SolutionInn App