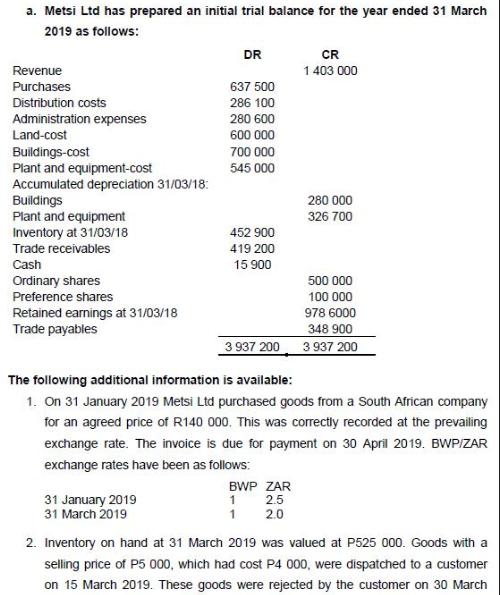

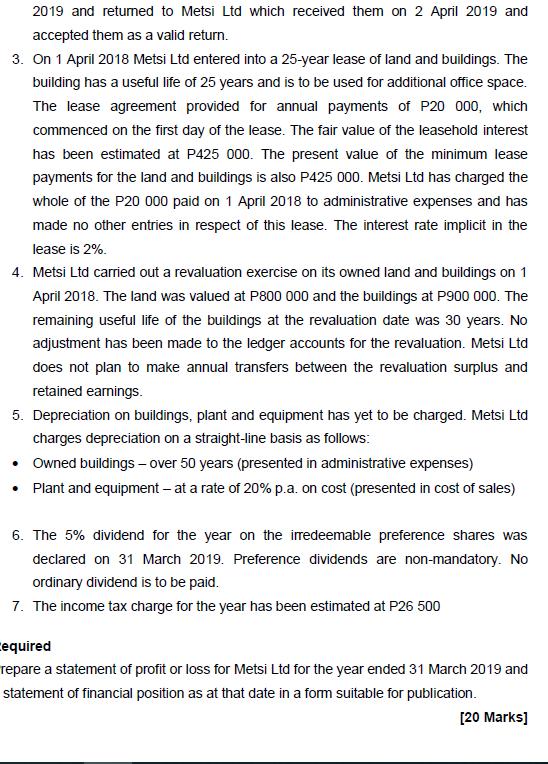

a. Metsi Ltd has prepared an initial trial balance for the year ended 31 March 2019...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

Related Book For

Financial Accounting and Reporting

ISBN: 978-0273744443

14th Edition

Authors: Barry Elliott, Jamie Elliott

Posted Date: