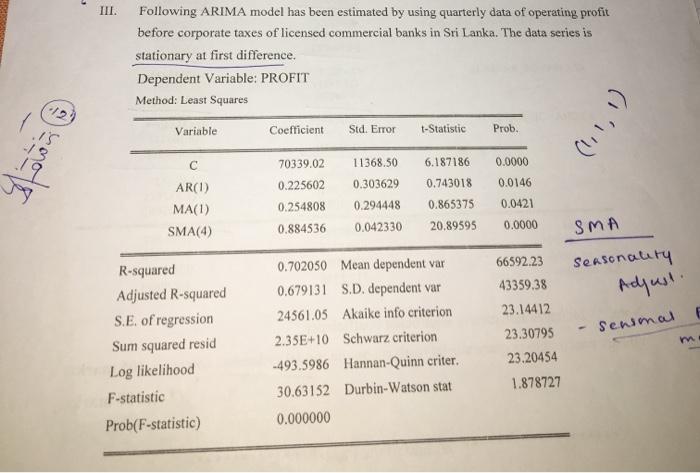

(12) is 13 III. Following ARIMA model has been estimated by using quarterly data of operating...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

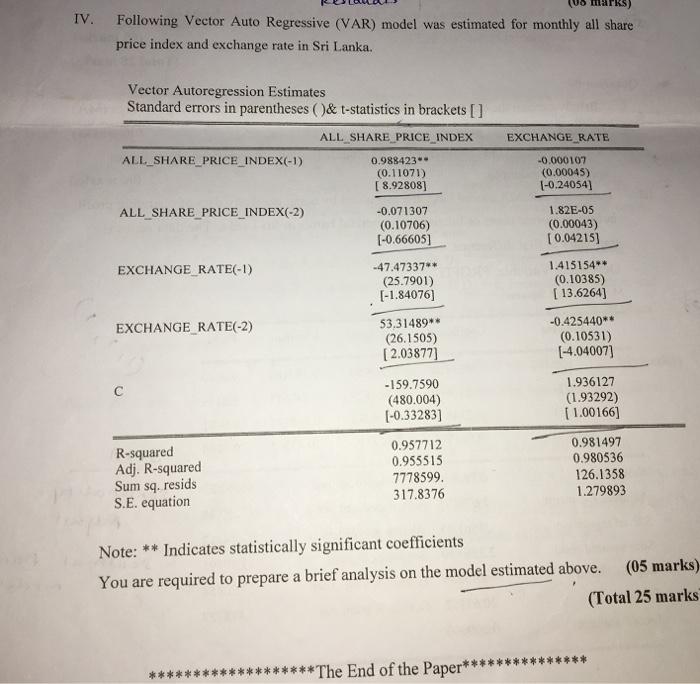

(12) is 13 III. Following ARIMA model has been estimated by using quarterly data of operating profit before corporate taxes of licensed commercial banks in Sri Lanka. The data series is stationary at first difference. Dependent Variable: PROFIT Method: Least Squares Variable C AR(1) MA(1) SMA(4) R-squared Adjusted R-squared S.E. of regression Sum squared resid Log likelihood F-statistic Prob(F-statistic) Coefficient, 70339.02 0.225602 0.254808 0.884536 Std. Error t-Statistic Prob. 11368.50 6.187186 0.0000 0.303629 0.743018 0.0146 0.294448 0.865375 0.0421 0.042330 20.89595 0.0000 0.702050 Mean dependent var 0.679131 S.D. dependent var 24561.05 Akaike info criterion . 2.35E+10 Schwarz criterion -493.5986 Hannan-Quinn criter.. 30.63152 Durbin-Watson stat 0.000000 66592.23 43359.38 23.14412 23.30795 23.20454 1.878727 (1, 1, 1) SMA Seasonality Adjust. - Sensmal m IV. AR res MA roots as 00 -1.6 -10 -0.5 00 0.5 a) Write the name of ARIMA model estimated above. b) Interpret coefficients of the model e) Analyze goodness of fitness and validity of the model. 40- EXCHANGE RATE(-1) Residuals (85 marks) Following Vector Auto Regressive (VAR) model was estimated for monthly all share price index and exchange rate in Sri Lanka. Vector Autoregression Estimates Standard errors in parentheses ()& t-statistics in brackets [] ALL SHARE PRICE INDEX ALL_SHARE_PRICE_INDEX(-1) EXCHANGE RATE(-2) R-squared Adj. R-squared Sum sq. resids S.E. equation ALL SHARE_PRICE_INDEX(-2) Roots of ALAM Poyom 0.988423** (0.11071) [8.92808] -0.071307 (0.10706) [-0.66605] -47.47337** (25.7901) [-1.84076) 53,31489** (26.1505) [2.03877] -159.7590 (480.004) [-0.33283] 0.957712 0.955515 7778599. 317.8376 lags vanable *********The End of the Paper*** EXCHANGE RATE -0.000107 (0.00045) (-0.24054) 1.82E-05 (0.00043) [0.04215] 1.415154** (0.10385) [13.6264] -0.425440 (0.10531) [4.04007] 1.936127 (1.93292) [1.00166] 0.981497 0.980536 126.1358 1.279893 Note: Indicates statistically significant coefficients You are required to prepare a brief analysis on the model estimated above. (05 m (Total 25 r IV. Following Vector Auto Regressive (VAR) model was estimated for monthly all share price index and exchange rate in Sri Lanka. Vector Autoregression Estimates Standard errors in parentheses ()& t-statistics in brackets [] ALL SHARE_PRICE_INDEX(-1) ALL SHARE_PRICE_INDEX(-2) EXCHANGE RATE(-1) EXCHANGE RATE(-2) R-squared Adj. R-squared Sum sq. resids S.E. equation ALL SHARE PRICE INDEX 0.988423** (0.11071) [8.92808] -0.071307 (0.10706) [-0.66605] -47.47337** (25.7901) [-1.84076] 53,31489** (26.1505) [2.03877] -159.7590 (480.004) [-0.33283] 0.957712 0.955515 7778599. 317.8376 EXCHANGE RATE *The End of the Paper** -0.000107 (0.00045) [-0.24054] 1.82E-05 (0.00043) [0.04215] 1.415154** (0.10385) [ 13.6264] -0.425440** (0.10531) [-4.04007] 1.936127 (1.93292) [1.00166] 0.981497 0.980536 126.1358 1.279893 Note: ** Indicates statistically significant coefficients You are required to prepare a brief analysis on the model estimated above. (05 marks) (Total 25 marks (12) is 13 III. Following ARIMA model has been estimated by using quarterly data of operating profit before corporate taxes of licensed commercial banks in Sri Lanka. The data series is stationary at first difference. Dependent Variable: PROFIT Method: Least Squares Variable C AR(1) MA(1) SMA(4) R-squared Adjusted R-squared S.E. of regression Sum squared resid Log likelihood F-statistic Prob(F-statistic) Coefficient, 70339.02 0.225602 0.254808 0.884536 Std. Error t-Statistic Prob. 11368.50 6.187186 0.0000 0.303629 0.743018 0.0146 0.294448 0.865375 0.0421 0.042330 20.89595 0.0000 0.702050 Mean dependent var 0.679131 S.D. dependent var 24561.05 Akaike info criterion . 2.35E+10 Schwarz criterion -493.5986 Hannan-Quinn criter.. 30.63152 Durbin-Watson stat 0.000000 66592.23 43359.38 23.14412 23.30795 23.20454 1.878727 (1, 1, 1) SMA Seasonality Adjust. - Sensmal m IV. AR res MA roots as 00 -1.6 -10 -0.5 00 0.5 a) Write the name of ARIMA model estimated above. b) Interpret coefficients of the model e) Analyze goodness of fitness and validity of the model. 40- EXCHANGE RATE(-1) Residuals (85 marks) Following Vector Auto Regressive (VAR) model was estimated for monthly all share price index and exchange rate in Sri Lanka. Vector Autoregression Estimates Standard errors in parentheses ()& t-statistics in brackets [] ALL SHARE PRICE INDEX ALL_SHARE_PRICE_INDEX(-1) EXCHANGE RATE(-2) R-squared Adj. R-squared Sum sq. resids S.E. equation ALL SHARE_PRICE_INDEX(-2) Roots of ALAM Poyom 0.988423** (0.11071) [8.92808] -0.071307 (0.10706) [-0.66605] -47.47337** (25.7901) [-1.84076) 53,31489** (26.1505) [2.03877] -159.7590 (480.004) [-0.33283] 0.957712 0.955515 7778599. 317.8376 lags vanable *********The End of the Paper*** EXCHANGE RATE -0.000107 (0.00045) (-0.24054) 1.82E-05 (0.00043) [0.04215] 1.415154** (0.10385) [13.6264] -0.425440 (0.10531) [4.04007] 1.936127 (1.93292) [1.00166] 0.981497 0.980536 126.1358 1.279893 Note: Indicates statistically significant coefficients You are required to prepare a brief analysis on the model estimated above. (05 m (Total 25 r IV. Following Vector Auto Regressive (VAR) model was estimated for monthly all share price index and exchange rate in Sri Lanka. Vector Autoregression Estimates Standard errors in parentheses ()& t-statistics in brackets [] ALL SHARE_PRICE_INDEX(-1) ALL SHARE_PRICE_INDEX(-2) EXCHANGE RATE(-1) EXCHANGE RATE(-2) R-squared Adj. R-squared Sum sq. resids S.E. equation ALL SHARE PRICE INDEX 0.988423** (0.11071) [8.92808] -0.071307 (0.10706) [-0.66605] -47.47337** (25.7901) [-1.84076] 53,31489** (26.1505) [2.03877] -159.7590 (480.004) [-0.33283] 0.957712 0.955515 7778599. 317.8376 EXCHANGE RATE *The End of the Paper** -0.000107 (0.00045) [-0.24054] 1.82E-05 (0.00043) [0.04215] 1.415154** (0.10385) [ 13.6264] -0.425440** (0.10531) [-4.04007] 1.936127 (1.93292) [1.00166] 0.981497 0.980536 126.1358 1.279893 Note: ** Indicates statistically significant coefficients You are required to prepare a brief analysis on the model estimated above. (05 marks) (Total 25 marks

Expert Answer:

Related Book For

Statistics Data Analysis and Decision Modeling

ISBN: 978-0132744287

5th edition

Authors: James R. Evans

Posted Date:

Students also viewed these general management questions

-

Consider the following balance sheets and selected data from the income statement of Keith Corporation. Keith Corporation Balance Sheets December 31 Assets 2019 2018 Cash $1,450 $980 Marketable...

-

Bio medical's operating income before taxes was $90,000 ($10,000 of this was R&D expense and $5,000 expense was damages from a spring flood). Capitalized R&D is amortized over 5 years. What...

-

Handicraft Inc. starts selling purely native bags early August of this year for P1,300 each. This product is very suitable for gifts and passed the quality control for exports. The company also gives...

-

The parol evidence rule: a. allows the introduction of conflicting oral testimony relating to contractual obligations if the parties had an oral agreement prior to forming a fully integrated written...

-

What is the meaning of each of the four states in the MESI protocol?

-

Refer to the fungus growth data of Exercise 12.2.7. For these data. SS(resid) = 16.7812. (a) Calculate the standard error of the slope, SEbl. (b) Consider the null hypothesis that laetisaric acid has...

-

Is technological excellence enough for choosing a programming language?

-

A rower wants to row her kayak across a channel that is 1400 ft wide and land at a point 800 ft upstream from her starting point. She can row (in still water) at 7 ft/s and the current in the channel...

-

Prepare the schedule of cost of goods manufactured for Barton Company using the following information for the year ended December 31. Direct materials used Direct labor Factory overhead Work in...

-

Ayayai Hotels Ltd. (AHL) is a small boutique hotel that provides 44 suites that can be rented by the day, week, or month. Food service is available through room service as well. In addition, there...

-

How many true breeding pea plant varieties did Mendel select as pairs, which were similar except in one character with contrasting traits? (1) 4 (2) 2 (3) 14 (4) 8

-

Lease arrangement and other equipment information SLR has agreed to lease the equipment to Agri-Panel with the following terms: Annual payments of $6,000,000 are due at the beginning of the period...

-

Establish the reasons for losses or profits in previous financial reports. Review the requirements for compliance and liabilities in taxation. Analyze existing financial management software and its...

-

Briefly describe the difference between the 3 levels of the fair value hierarchy that a company following IFRS must choose from when noting its ability to reliably measure each investment's fair...

-

The Basel Committee's Guidance follows from principles of corporate governance published by Organisation for Economic Cooperation and Development (OECD). Explain how the Royal Bank of Canada has...

-

Part 1: Calculating Contribution Margin and Breakeven Point 1. Calculate the contribution margin rate, the sales dollar breakeven point, and the unit sales breakeven point. 2. Use the following...

-

StellarCraft, a space equipment manufacturer, produces three types of space components: "Plasma Thrusters," "Navigation Systems," and "Solar Panels." StellarCraft needs to determine the optimal...

-

If someone's Z-score for a variable was 0.67. Their score is a significant extreme score. Their score is not significant. O Their score is slightly above average. O Their score is an outlier.

-

What is a pvalue? How is it used to reach a conclusion about a hypothesis test?

-

Apply stepwise regression using the each selection rule and t value criterion to find the best model for predicting the number of wins in the Major League Baseball data. Compare your results. How do...

-

What are the primary components of time series?

-

For each of the following sets of numbers, calculate a \(95 \%\) confidence interval for the mean ( \(\sigma\) known); before going through the steps in calculating the confidence interval, the...

-

Consider a 3 -year \(10 \%\) coupon bond. The underlying short rate of interest follows a lattice with initial value of \(R=1.15\) and then has an factor of 1.02 , a down factor of .99 , and...

-

Using the density function of the stopping time probability for a fixed \(\lambda\), find the average time to the first event over the entire interval \([0, \infty)\).

Study smarter with the SolutionInn App